Happy Belly Food Group ($HBFG.C) Special

Upon Further Review - Analyzing HBFG's QSR System Sales

I don’t like not having all of the answers. I never have, and I never will.

Additionally, I feel I have a unique way of analyzing companies, using fundamentals and financial analysis in addition to the average retail investor due diligence. Much of that stems from having some form of P&L accountability during my working life.

Due diligence isn’t easy, but it doesn’t really require a superior skill set. It’s hard. It’s grunt work. I don’t like doing it. I’d much rather read someone else’s and verify it. But when it comes to analyzing fundamentals and earnings reports, and finding those important intangibles that make a difference is where I personally feel I have an investor edge. Perhaps that is why I have the privilege of so many who read my ramblings on a fairly frequent basis.

I’ve sat in my share of board rooms over the years. I’ve seen and written on many a whiteboard. Annual plans. Five year plans. SWOT analysis. Objectives. Initiatives. Competitors. I’ve been the one handling the erasable marker and I’ve been across the table while someone holding that marker is verbally ripping me a new asshole.

So when I review a company, I imagine what may be written on their board room whiteboard. Does it match what I would write on it? If it does than the chances of investing in them rises.

Much of this has been true for Happy Belly Food Group going back to 2022. Fundamentals were rather terrible back then. That was a due diligence and intangible investment decision - the biggest intangible was betting on the jockey.

If you know anything about horse racing, you don’t bet on a horse who has a high winning percentage on a fast track going 5 1/4 furlongs when the race is a mile and a half on soggy turf. You bet on a mudder who has the stamina to run long distances. Sean Black and his team are mudders. They are also familiar with the track and distance.

But that doesn’t mean they will avoid criticism. My most recent two reviews, the Mother of All Reviews for their annuals in April and the more recent for Q1 financials, received their first ever downgrade of the company since I began covering them. To be honest, they probably received the most number of reviews WITHOUT being downgraded prior to that.

There were those who thought I was too harsh. Others focused on items that had little relevance. A select few questioned my motives. The latter ones can quite frankly eat my ass. My existence is not to verbally fellate companies either of us are invested in.

To summarize, I had the following concerns regarding the last two sets of Happy Belly’s financials:

Increased operating expenditures and margin reduction

Positive operating cash flow turning to cash burn

Challenges of supporting their growing network

Lack of earning calls given their valuation and desire for more data

Questions on their QSR system sales. QoQ, YoY

There’s no getting around the first two, the numbers are the numbers. The third is just factual, particularly from someone who has grown a network of franchisees across the country. I’ve lived those challenges.

With the first three, I’m confident enough in management that they are equally aware of those issues. I’m also confident enough in the team to know that they exist somewhere in a PowerPoint deck, a short and or long term plan, or in my imaginary board room whiteboard.

In terms of the fourth, earnings calls and more data, like SSS (Same Store Sales) I did have some DM’s with the CEO, Sean Black that made me more comfortable as they will be working towards those.

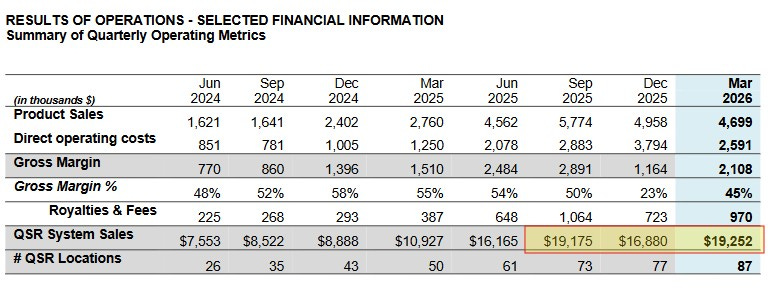

Then we come to number five - their QSR system sales. As I wrote off the top, I don’t like not having all of the data. The system sales looked light to me, particularly in Q4, and to some extent in Q1.

Obviously there are many things to consider. 10 different brands whose AUV (average unit volume) may differ. Seasonality, particularly with their number one brand, Heal Wellness. Smoothies are much more desirable in July, than mid February after all. Their incredible growth of locations is another factor as some may be open a week while others may be open for the majority of a particular quarter.

Sean and I chatted about this also, and I learned some things.

But I still didn’t have any hard data to make me feel better. While some fart sniffers were concerned about whether cross trades would be necessary for insiders to exercise their warrants and options, I’ve been thinking about this. Was there any data for a better apples to apples comparison, even if that might mean we’re comparing a Red Delicious to a Granny Smith. I think I found a method. Here is the data that was readily available:

Quarterly system sales

Number of locations at the start of each quarter

Openings per quarter and their grand opening dates

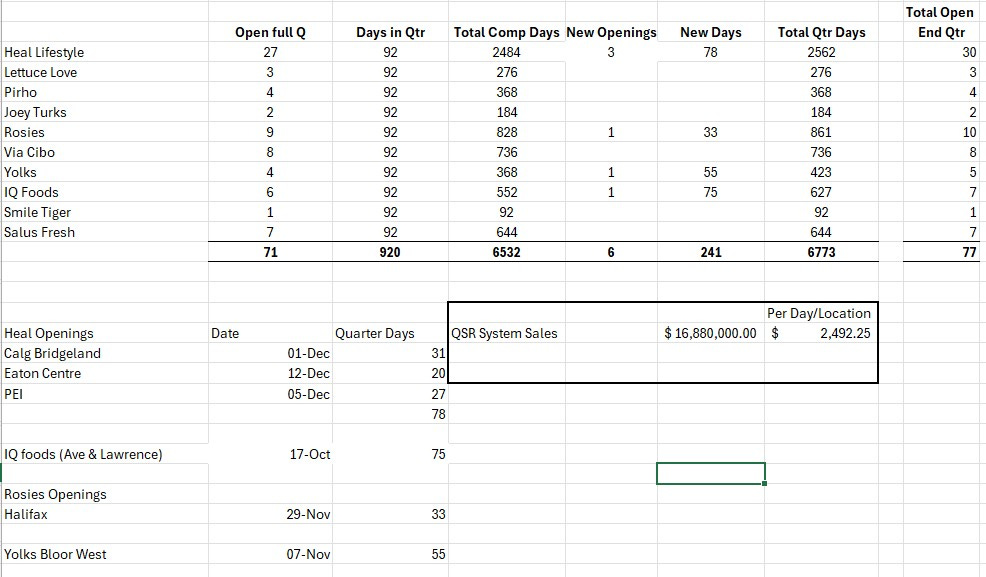

I deemed the best way to analyze their QSR System Sales data was to calculate their revenue, per location, per day. Due to the ten different brands and varying brand AUV’s, this will be imperfect but it would address the seasonality, and smooth out the variances in opening dates regardless of where they occurred in the quarter.

Then, I nerded out. For each of the past eight quarters, I developed a spreadsheet as you see below. It calculates the number of days HBFG had a franchise with their doors open (number of locations x number of days). That number was then calculated against the company’s provided quarterly QSR System Sales data. Stores open for the full quarter were relatively easy (although errors were discovered within previous MD&A’s). Then it was a matter of digging out the number of locations that opened and for how many days for each.

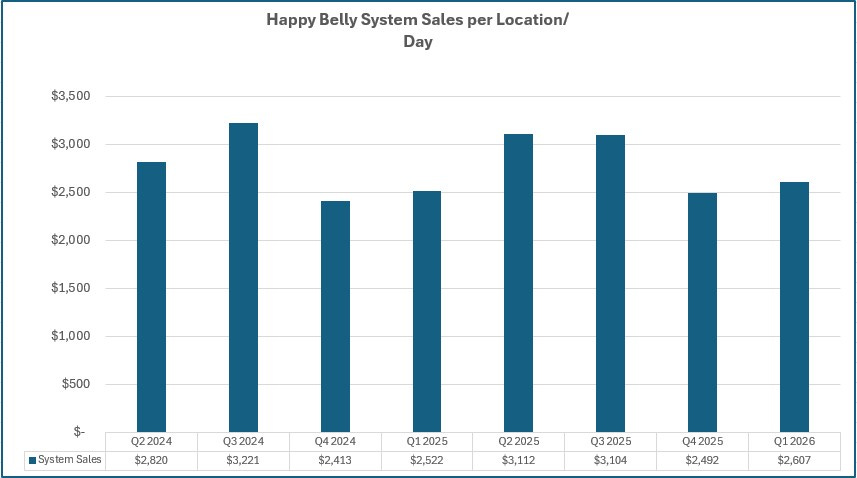

Now here is what all of the data shows for the last eight quarters. To nobody’s surprise there is a rather significant seasonality impact with QSR sales/day being nearly 20% lower in Q4 than Q3, roughly $3,100/day vs $2,600.

What I was pleasantly surprised by is that on a YoY basis, the last two quarters grew by 3.3% and 3.4% respectively in sales per location per day. Most recently Q1 of 2026 $2,607 vs $2,522 a year ago.

In the most recent quarters comparison, Heal Wellness made up about 40% of all locations both this year and last year. With Heal’s having a smaller AUV than some of the other brands, the fact their percentage to the total was similar in each quarter helps validate those growth numbers. In quarter where more Rosie’s Burgers or Yolks Breakfast have a higher percentage of more days open than last year, we should see a higher sales per day number, and the reverse would be true for Heal locations.

Again, these numbers are not totally perfect. They account for many variables, but not all. But I think we can infer or better rationalize variances to expectations by going through this exercise. At least until we have SSS data by brand, by province/state. Right Sean?

In conclusion, while this doesn’t alleviate all the concerns from the past couple of reviews, I think the data strongly suggests we can put any growth comparison questions behind us for now. The other thing this enables me to do is to have some QSR system sales projections for future quarters. I’ve now done that for Q2 which will finish with over 100 locations and ends in ten days. If you’re nice to me, I might let you know what I’m projecting for Happy Belly’s August results.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Bring it on Wolf more info is great people can decide themselves what they do with it.

Excellent review as always. Looking forward to your projections