After years of doing this, you think I would know better by now than to comment immediately on socials and bulletin boards when financials drop. The argument can be made that I should probably refrain from doing so all together. Will I ever change? Not a chance.

If you read my “Mother of Reviews” article released on Mother’s Day, than you’re aware that I had some concerns regarding the QoQ Q4 revenue numbers for Happy Belly. My initial glance Tuesday night at the Q1 financials had a similar feel and that seemed to have set off a bit of permabulls - one of my favourite pastimes.

I’m almost 100% certain that I have written more reviews on Happy Belly than any other stock, reviewing every quarter since early 2022. In November of that year, they received my first upgrade when the stock traded at 8 cents and was under a $9M market cap. A month later they were included in my first ever batch of Wolf Picks when the stock traded at a dime.

So much time has passed that showing a five year weekly chart is now a relevant endeavour. Today they sit 20x higher from that upgrade and more than a 15 bagger from the Wolf Pick with a market cap approaching a quarter billion dollars.

A large part of the bull case back then remains the same - the bet on the jockey, and the team striving to do something they had done with some degree of success before. That stir the other night resulted in some chatting with that lead jockey, Sean Black yesterday morning.

Many likely don’t realize that I’ve been in a similar chair as Sean is today in taking a brand from zero dealer/franchise businesses to over 250 within a decade. I know what it’s like to have accountability for revenue and profitability numbers and having someone with only macro visibility into the business slice and dice my numbers. Let’s just say Sean handles this better now than I did back then.

At the same time that isn’t going to change the critical lens that I review all financials with. Wolf Picks, and those I hold larger positions in will always get an extra dose of scrutiny. If my neighbours kid received a “C” in Social Studies, I’d say “Way to go little buddy”. If it’s my kid, they’d get grounded for a week.

If you’re a reader of mine, I would hope you would want it that way. If not, I have bad news for you.

Let’s get more granular into Happy Belly’s Q1.

Balance Sheet:

A big improvement in the company’s balance sheet Q1 over Q4, now sporting a current ratio of 2.2 consisting of $6.2M in cash, $2.4M of receivables and $700k in other short term assets overtop of just $4.3M in liability commitments (deferred revenue removed) over the next twelve months.

The biggest difference QoQ is their strengthened cash position and I’ll touch on the why in the next section. The end result is much improved liquidity with just the company’s cash position at 1.4x current liabilities compared to only .65x a quarter ago.

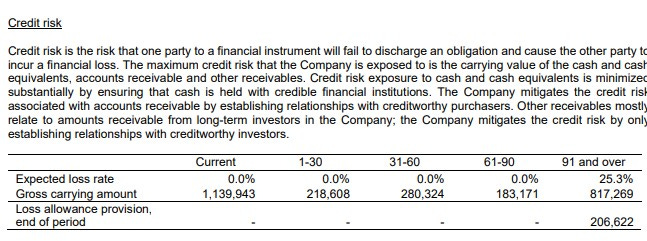

I have been keeping an eye on their A/R over time and I don’t feel I’ve addressed it in a review yet, but it does appear to have the beginnings of something to be mildly concerned about. Less than half of their receivables are current with a third over 90 days past due. A quarter of the 90 days plus is booked as potential losses. In this model I would expect the bulk of their A/R to be from franchise fees and royalties. So, this certainly is something to monitor as it is very important to cash flow and franchisee health. The company also mentions “other receivables” from investors but those amounts do not appear to be broken down in the financials or MD&A. If those are material amounts, disclosure needs to be better.

HBFG has $1.4M of debt in the form of convertible debentures. The remaining debentures all stem from Feb 2024. The holder of the debentures has the option of cash or shares and since the conversion price is $0.50 look for them to be converted to shares in Feb of 2027 or earlier. Since that is less than 12 months from the end date of this quarter, I believe these amounts are incorrectly stated under long term liabilities.

Cash Flow:

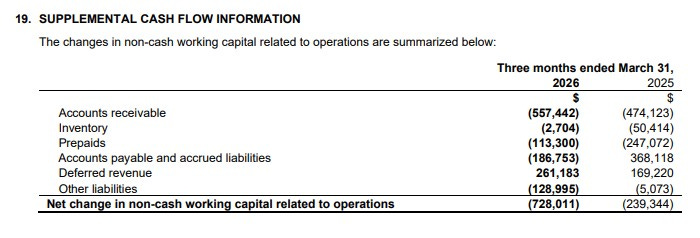

For the second straight quarter we have operational cash flow comparisons going the wrong way with $940k of cash burn vs $156k last year. Much of that variance is due to working capital adjustments. Most of those adjustments are from the previously mentioned accounts receivable, making that aging report more important to review in future quarters.

The influx in cash in Q1 came both through investing and financing activities. In February, Happy Belly sold their Holy Crap cereal CPG brand. It was an excellent brand but I think exiting their CPG segment to focus on QSR was the appropriate step in their growth journey. Getting $1M for it feels like a good return as well.

The company also received over $3.7M into the treasury through warrant and option exercises. That is a nice segue into the next section.

Share Capital:

148.2M shares outstanding representing 10% dilution this quarter and 15% dilution over the past five quarters.

All of Q1 dilution stemmed from exercising warrants and options

31.9M warrants outstanding with 14M well ITM at 20 cents and expiring in just over a month. All remaining warrants are at $2 and will be vested on future share price targets. See their news release from November or one of my previous reviews for more details

16.9M options. The most recent 12.1M have similar vesting triggers as the recently mentioned warrants

3.2M options also expire next month ranging from 40 cents to $1.14.

With all of the options and warrants exercised I have insider ownership around 27% but with all of the recent activity that may not be 100% accurate. Let’s call it ballpark

Insiders have also been regular buyers in the open market for years, more so than any other stock I have ever covered. Insiders have however been performing some cross trades to sell shares in order to exercise their numerous performance warrants and options. I anticipate we will see a lot more of this in the next month with a staggering 14M warrants and 3.2M options expiring in less than five weeks. This would bring approximately $5.4M into the treasury increasing their cash position by 87% from where it is today - it’s significant. The value of these shares is worth well over $25M so there is a lot of profitability on the table for the holders of those warrants and options. Therefore expect some insider selling on the horizon.

That will take the float to approximately 165.5M shares by the time we see the company’s second quarter. That’s an additional 12% dilution from today giving an implied market cap of about $260M.

Let me say if you have issues with the dilution you haven’t been paying attention to this story. Insiders were rewarded for share price performance, and the influx’s of capital will largely come from them to support future growth. I’d much rather have it this way than your typical private placement. Given that big push to get the stock to $2 is why I sold some and above that number and re-purchased them at $1.50.

Income Statement:

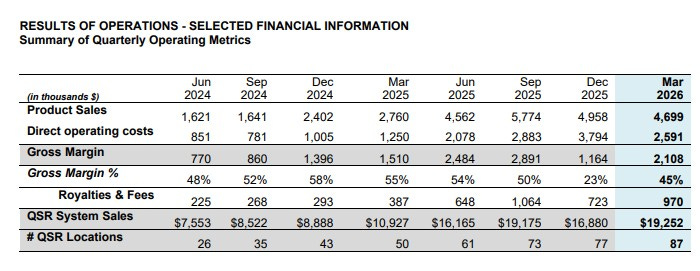

There are a lot of YoY and QoQ numbers to get through. There is no question the YoY numbers are tremendous. Firstly is purely the number of units up by 74% from where they ended Q1 a year ago, going from 50 QSR locations to 87 at the end of March. I’m sorry to say the company did get a couple of figures (percentages) wrong in their MD&A and news release.

Product Sales rose by 70%, not the 101% as stated in the MD&A, and Royalties and Fees rose by 151%, not the 118% as stated in their earnings news release. QSR system sales rose by 76% to $19.25M. That is a 14% increase on a QoQ basis but just better than flat when compared to Q3 of 2025 on 19% more restaurants. Total revenues rose by 82% over the comparable quarter.

Gross margins, while not a specific P&L line, took a rather substantial hit for the second straight quarter coming in at 45%. There are some seasonality impacts with additional costs (Uber Eats), but I think it’s a large miss by not addressing the margin line whatsoever within the MD&A. Gross margin dollars rose by less than 40% on 70% more product sales and 74% more stores and that was the biggest contributor for the quarter’s weak cash flow.

I’m overall aligned with the company’s SBC strategy that rewards insiders based on share price as it sets up a win/win situation with shareholders, therefore I’m not concerned with the high costs seen this quarter. Firstly, it was expected. Secondly, they are non cash burning.

With SBC costs and depreciation stripped out of operating expenses, cash burning expenses rose by 97%, and that is a bad combination when only 40% more gross profit dollars were generated. Again with SBC removed, net losses amounted to $681k in the quarter, and that is about 3.8x worse than a year ago.

Summary:

Did the quarter live up to my expectations? No. Is it a disaster? Also, no.

Seasonality variances within Heal given their products they sell and the fact make up the largest portions of total restaurants are a huge factor here. I was surprised to learn from Sean about the seasonality impacts of brands like Rosie’s and Yolks. The fact the company announced and delivered Q1 well before the deadline also factored into not meeting what I had expected.

So, if you are willing to accept the above rationale for only matching off 2025 Q3 in this most recent quarter, that just amplifies investor expectations for seasonably better quarters of Q2 and Q3.

What the company is doing exceptionally well is expansion, and by the time we review their Q2 financials, their store count will almost certainly exceed 100 locations. That justifies some of the additional costs we have seen in the last two quarters. By the end of next quarter with the warrants and options earlier, they should be well capitalized to support continued growth.

The concerns and things to watch out for are just as numerous as their strengths however.

If we accept the new seasonality situation, that is going to present cash flow challenges. That requires discipline and execution, and those concerns increase with mentions in the MD&A about understaffing in the accounting department. The unfortunate passing of their CFO last year had to have been a major contributing factor. They have done some recent hiring to help fill the gap with their new CFO still coming up to speed. That understaffing may be showing given the rather simple errors mentioned earlier, and could be contributing to their growing A/R and poor aging report.

Those seasonality challenges also extend to the franchise network - probably more so. To be a successful franchisor, you need healthy franchisees. I can tell you from experience that many franchisee’s weaknesses come on the operations side, and managing their own cash flow is a big part of that. I could do an entire article on this topic.

Given the above, operational support to that growing network is key. Given they are currently operating more than ten brands, that makes that challenges larger. Maintaining brand standards, marketing and operating support and infrastructure across ten brands with a massive geographical footprint is much more daunting than I think the average retail investor realizes. The number of brands and those geography challenges will grow this quarter with the acquisition of Ghost Taco scheduled to close shortly, as well as the first Heal location in Texas.

Then there are the brands that have been slow out of the gate. Lettuce Love, Pirho and Joey Turks really haven’t been part of any news flow in a very long time. I discussed this in more length in my Q3 review.

Lastly is the $260M valuation (including upcoming dilution at today’s share price). They still need to grow into that figure as one would be hard pressed to justify that number today. Can they do it? I believe they can, but it will not be without a number of challenges and obstacles.

Sticking with my three star rating from last week. Cue up David Bowie and Freddie Mercury. Pressure is on for Q2.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.