Mother's Day Earnings Recap - The Mother of all FINS Reviews

ZOMD.V NCI.V AEP.V HBFG.C GSI.V PCRX.V BRM.V

I’m back from nearly two weeks of vacation and a lot transpired with earnings for microcaps that I regularly cover. I’m going to provide a summary of each and combine them into one article - something I’ve never done before. Due to the release on Mother’s Day, I’m dubbing it “The Mother Of All Reviews”

Rather than do seven separate deep dives, it feels appropriate as six of the seven of these companies reported their Q4 and annual filings in the past two weeks. They will therefore be reporting their first quarter within just a few weeks. Watch for my more typically formatted reviews when those are released.

As a group, with two exceptions, I would contest their results similar to words you wouldn’t want to hear on your wedding night - soft and disappointing. I will go in order from what I perceive to be the worst to best.

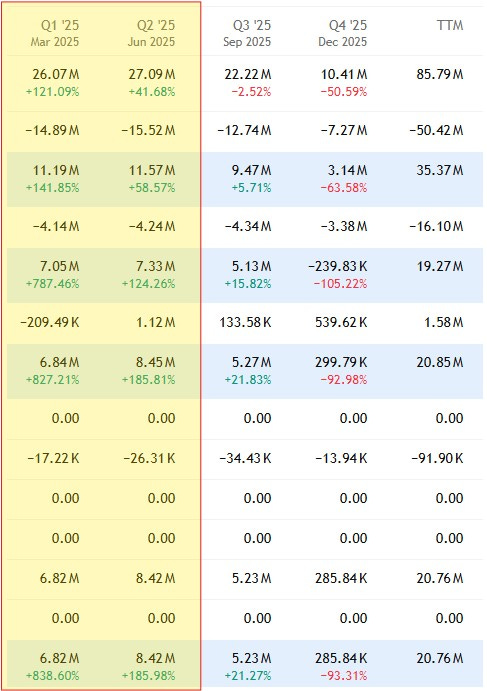

After going over 6x in share price between last May to October of last year, the stock is now up a measly 15% over the past year and down 81% over the past seven months.

This all occurred with annual revenues up by 15% and net income up by 70%. Those annual revenues of nearly $86M with $20.7M in net income has the stock trading at valuation multiples of under 3 P/E, 2.25x cash flow and 1.2 EV/EBITDA. They are currently at a market cap of $53M while having over $30M of cash on hand.

While the back half of the year was considerably softer than last year including a disastrous 50% decline in top line revenue, it feels like a good portion of the decline in valuation has been self inflicted through very mixed messages to the market. For months those that followed the company knew there were concerns with the companies top two customers. The sequencing of events was very well explained in this Valuation Desk piece published shortly after their earnings.

I think if the company was more forthright in their comments after Q3 and even in their subsequent interview with Small Cap Discoveries, the stock would be in a better position than it is in today. Investors went to “fixed” and “back to business” with these two clients, to “limited visibility” with one and “signs of realignment” with the other. Those aren’t exactly comforting statements, particularly when you look at the monster comps the company is up against, starting with their Q1 scheduled to report by the end of May, followed by the best top and bottom line quarter in the companies history in Q2.

Until we know where those two customers stand, it’s really impossible to assign a realistic valuation here. If they return to their former glory, than ZOMD is vastly undervalued. The market currently has them priced as lost causes. I feel that is likely unfair, but with the varying comments that some could (and have) perceive as dishonest or misleading, the market is currently pricing in all of the risk. It’s not the first time I have questioned the amount of ZoomD’s disclosures - their interim financial statements typically total only eight pages and that includes the title and table of contents.

Is it all doom and gloom? No, and far from it. When you parse out the impact of their two largest customers, they have been able to grow the rest of their business by around 30%. They also stand to gain some substantial wins from this years World Cup. They have also shown themselves to be excellent operators with their operational costs, spending the same amount in operational expenses as they did two years ago while virtually doubling revenue.

They also possess an immaculate balance sheet with a current ratio of over 5.4 while sitting on over $30M in cash which is 4.4x their entire 2026 liability commitments. There has been lots of speculation on what the company should do with that cash windfall, with the overwhelming consensus that it should contain a healthy level of share buybacks.

The fact they haven’t pulled the trigger on an NCIB is very telling. If they felt these two customers were going to come back in full force within a short time frame it would have happened already. It’s also notable that insiders don’t feel these valuations have hit bottom either, as their wallets have been firmly entrenched in their pants throughout that 80% share price free fall.

My gut instinct is if there is good news on the horizon with these two customers, buy backs will commence AFTER their Q1 is released. Why do it now knowing Q1 is shaping up to be a massive dud as well? That quarter was completed over five weeks ago, and the commentary in their MD&A is more recent. That sets up for an absolute disaster for their first quarter earnings, likely worse than the ones we just witnessed.

The bottom line is just as important as winning back those two customers, is winning back investors trust. I’m not sure they can fully win back mine. One of my biggest downgrades on record - 4.25 stars down to 3.

Believe it or not, I had a difficult time determining who should go first in my worst to best ranking - ZoomD Technologies or NTG Clarity.

NTG Clarity is still up over 6x from my 2024 Wolf Pick, but let’s not forget they were only three cents shy of becoming a 20 bagger from 15 cents to their all time high of $2.97. They are currently off 69% since that ATH eleven months ago.

NTG’s stock price is down 13% from their earnings released on April 27th. While the company had a solid year on the revenue line, up 49% on the year and 39% in Q4, profitability suffered heavily with net income down 46% in 2025 and 68% in Q4. Unlike some of the communication issues with ZoomD, NTG did telegraph much of this abnormal balance between their top and bottom lines over a year ago with their 2024 annual filings.

At that time they gave guidance of $75M in revenue with AEBITDA margins (eww) of between 16-20%. In fairness to NTG they did cite lower profitability targets due to increased taxation and investments in staff to go after new business. They beat revenue coming in at over $83M but missed the low end of their profitability target, achieving only 14%. That was a pretty significant announcement at the time. In 2024 the company achieved over 17% net income, and they changed their guidance from an N.I figure to a dreaded AEBITDA one. Then they missed it, and rather significantly at that.

NTG now trades around a $48M market cap, giving them valuations of less that .6x of revenue, 8.5 P.E and just 3.6 EV/EBITDA. By all normal standards these would appear very cheap, but due to their historical cash flow woes which I’ve discussed on several occassions, investors have no choice I believe to discount it. My problem with reading their Q4 financials is that cash flow situation has the potential to get even worse.

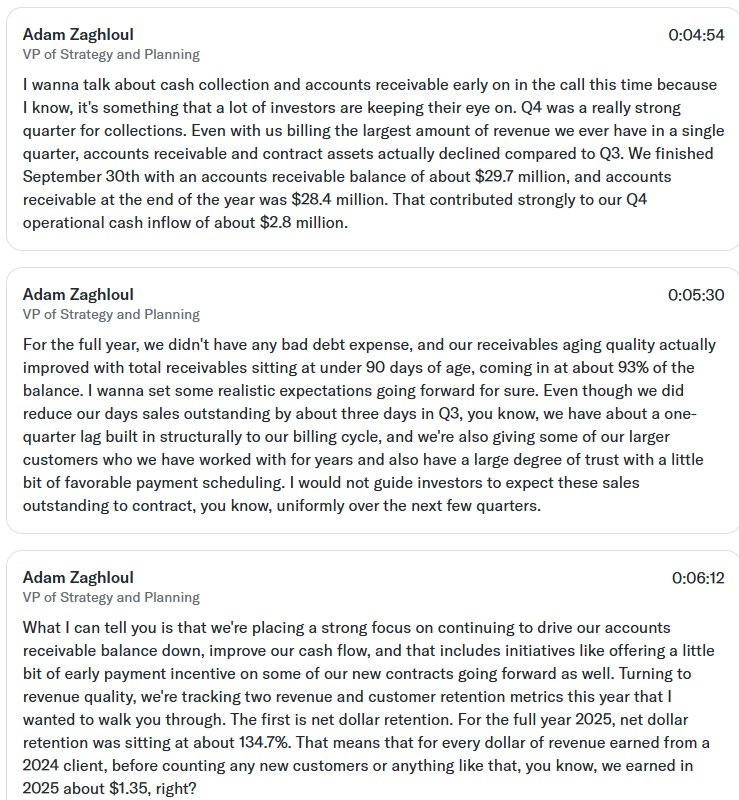

If you listened to their conference call you may have a different impression. Here is the portion of the transcript which speaks to this.

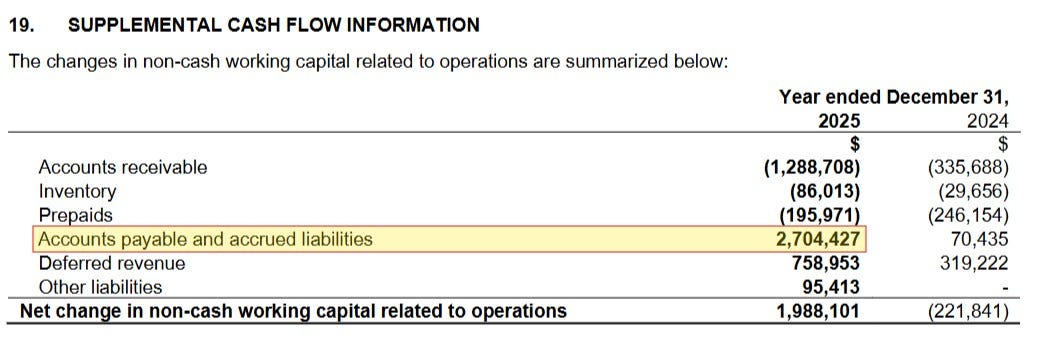

While Adam is correct that receivables went down this quarter, the problem is that is the first time that can be said in their last ten quarters. Their A/R aging reported also improved as noted. Here’s the problem with that - your aging will of course look better if you don’t bill your customers to begin with. That is not only what happened but it appears to be part of a bigger strategy when Adam mentions they are giving preferred payment schedules to certain clients. While that isn’t completely abnormal business practice, it is poor for cash flow and they already have more than generous payment terms to begin with. To top it off, Adam discusses early payment incentives which will impact profit margins.

In summary, they already have a lag built into their billing cycle and have seemingly added to this by the increase in contract assets YoY and QoQ. They have very generous payment terms compared to business norms and giving preferential treatment and discounts on top of the above to some. A company with $15M of net income over two years should not have negative cash flow over that same time frame and I just don’t feel management gets it based on their comments.

Last thing I will touch on is their seemingly weak guidance for 2026 of $90M in revenue with 13%-16% of AEBITDA. That is mid single digits on the top line with soft guidance on the bottom, particularly given the tax situation which they supposedly worked around with a Saudi Arabian LLC. Maybe it’s an under promise, over deliver type situation given missing 2025 profit guidance but I’ve decided to move on from the stock, selling bits and pieces over the last couple of weeks and totally closing my position on Friday.

Maintaining my 3 star review from November.

We’re moving from the very poor financials from the past couple of weeks into the more moderately disappointing ones, and that’s what we have here with Happy Belly Food Group. I probably could have ranked them anywhere from 3rd to 5th, but since I have more skin in the game with HBFG, I’m ranking them here.

The stock is off 3.5% since releasing their financials on May 1st, despite getting some positive acquisition news. Assuming it closes they will add a new brand in the Mexican fast casual arena in Ghost Taco with six existing locations in Ontario.

The year over year results for both the full year and Q4 were impressive as we have come to expect. QSR system sales were up by 108% on the year and 90% on the final quarter. I say as expected as they ended with 77 locations open by the end of 2025 vs 43 at the end of 2024.

QoQ figures were much less impressive coming in 12% lower in Q4 vs Q3 from $19.2M down to $16.9M. Costs on the other hand went completely the other way, with direct operating costs up by 47%, Payroll up by 5% and flat G&A costs.

Happy Belly also received a substantial hit to SBC expenses, but even if we remove that non-cash item, their operational loss in Q4 was $2.4M, compared to being profitable on that line through their first nine months.

Operational cash flow also suffered in Q4, although an overall glance at the cash flow statement doesn’t look problematic. Prior to working capital adjustments, HBFG burned $1.7M, but working capital adjustments thanks mainly to a growth in Accounts Payables makes their overall OCF look better than I suggest it should.

I’m sure seasonality plays a factor in here, particularly when Heal Wellness is the company’s largest brand. But at the end of Q3, Heal had 27 restaurant locations open representing just 37% of their 73 total locations. All of those 73 (plus 4 new locations in Q4) were open for the full quarter, yet total system sales lagged by 12%. I think completely writing that off to seasonality of smoothie bowls doesn’t cut it.

There are not a lot of pure comparisons in the Canadian market place, but for what we do have is MTY, down 2.8% sequentially (likely worse due to an added week in Q4), Tim Hortons was down 6% on a QoQ basis, but A&W was up a staggering 24% in Q4 vs Q3.

I’m not suggesting by any means that investors hit the panic button, but I think there is enough here to put extra focus and a larger magnifying glass on future quarters. That means investors demanding greater detail within their quarterly MD&A’s - a better breakdown of how each brand is performing, and SSS figures as is customary within the sector. I also feel it is time for management to step up and start setting up quarterly earnings calls. The first two stocks I mentioned (NCI and ZOMD) have a combined market cap of under $100M and they produce regular earnings calls. At a $240M market cap and with some analyst coverage, it’s time to expand beyond discussions within a discord full of cheerleaders (don’t be insulted, I include myself in that statement). Sean has the personality and outgoing demeanor that would perform extremely well in that type of format, so I hope he does.

A typical review here likely would have received a 1/4 star downgrade to 3 stars - the company’s first downgrade in the four or so years I’ve been covering them.

As has been the trend thus far, Atlas Engineered Products is down from their earnings release, but modestly to the tune of 4.5%. It still remains up however by 10.3% from their selection as a 2026 Wolf Pick. That happens to be the worst performing Wolf Pick of this year’s batch with the average up 50.3% (cheap self-promotional plug).

My expectations for the first set of financials after my annual pick were mild as the company continues to integrate their two recent acquisitions and get their Ontario robotics plant up and operational. The fact the company received $4M in federal grant funds as the plant upgrade is near completion was a big welcome bonus and strengthens what was already a pretty decent balance sheet.

Aside from seeing how Atlas will be taking advantage of the seemingly improving macro conditions surrounding construction and home building (not to be confused with the poor macro real estate situation), gross margin seems to be the most central thing to watch in terms of how the company will perform in 2026.

Margins dipped to under 20 points in 2025, a decrease of nearly 500 basis points compared to 2024. So despite a 12% revenue increase during the year they brought 10% less dollars to the gross profit line. The encouraging offset is their two largest cash burning operating expense lines (Admin and Payroll) only grew by 1% in 2025, despite the fact that they added two acquisitions in the middle of the year. That continues to prove to me what I have believed for a long time - they are very good operators.

Although Atlas suffered a small $375k net income loss, they did deliver $6.25M of EBITDA, and $7.35M of operational cash flow in 2025. That leaves them trading at around a 10 EV/EBITDA, and just over 6x cash flow. They also reduced their long term debt by 17% during the year.

As we get into the first couple of quarters of 2026, my mild expectations begin to grow. They are up against two soft quarters in the first half of the year with their two non-comp acquisitions in play. The company has battled very soft macro conditions in the past couple of years. While some may not be as optimistic as I am as to that turning - when it does, I want to have a piece of one of the best operators in the sector. I believe I have that with Atlas.

Holding my 3 star rating from their November third quarter review.

We now move to a 2024 Wolf Pick and very likely the one I played the worst in the past four years - selling my stake for a modest gain just prior to their very newsworthy fall of 2025 that sent the stock from $1.30 to $3.15 in about a six week window. Unfortunately the stock has come almost all the way back closing at $1.37 on Friday. That is down about 1.5% from their most recent earnings release after an initial gap up.

I did get a little revenge recently trading the stock from $1.27 to $1.60, but as I mentioned in my April WWW, my preference would have been to be on the outside looking in when earnings came around, and that worked out to be a successful trade.

Unlike the other six in this article, Gatekeeper was the only one not delivering their 2025 annuals, ahead of the group with their Q2 of their 2026 fiscal year.

Gatekeeper killed it on the top line in Q2 with 75% more revenue, but none of that translated to the bottom line with a net loss of $315k. This compares to a net loss of $1.06M in the comparable quarter - sadly this is misstated in Gatekeepers financials as someone forgot to add parenthesis so it appears incorrectly as a net income gain.

Gatekeeper got crushed on foreign exchange with a $406k loss compared to a gain of $403k last year. An $810k bogey in this account is hard to make up for elsewhere. When you take that impact out it was a very successful quarter. Gross margin grew from 38.8% to 42.5% which delivered 92% more gross profit dollars, and the company only spent 15% more in cash burning operation expenses while driving revenue by 75%. It was a Wolf Trifecta quarter ruined by forex.

Their YTD numbers are not quite as good despite achieving 23% more revenue and improving margins by 230 basis points. Operating expenses grew by slightly more than their revenue growth (25%), but that foreign exchange bogey remains growing to more than $900k YTD. That combined to grow their net loss by 177% YTD to $1.44M.

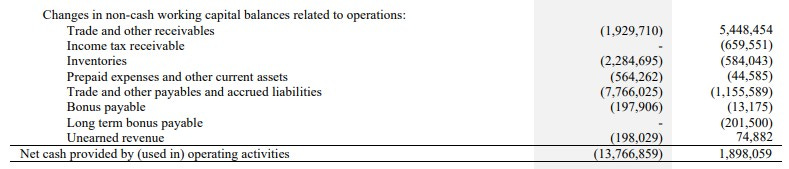

Gatekeeper’s cash flow statement looks like it is out of a horror movie with nearly $13.8M of cash burn through six months. Now this is due to significantly reducing payables while receivables grew, so I don’t anticipate this trend to continue. It is still concerning that they are still burning cash before taking into consideration working capital adjustments. Thankfully, they have an immaculate balance sheet with a current ratio of nearly 10 and possess excellent liquidity.

Pricing Gatekeeper currently is a challenge as they have negative net income, negative $3.3M TTM EBITDA and are no longer generating operational cash flow. From a pure fundamental metrics standpoint they are way behind when I selected them as a 2024 Wolf Pick when they had a P/E of 11, an EV/EBITDA ratio of under 9 and traded at under 5x cash flow.

The outlook is potentially better than is was at the end of 2023 as the company is well positioned in a sector with a lot of growth potential. Their MDC count could get near 100,000 by year end and while that is a nice source of recurring revenue I feel this is something most retail investors do overstate the importance of.

That profitability trend line which has taken a significant hit in the past six quarters needs to turn around through better execution. I think Q2 is a decent start when the forex impact is removed. Can they continue? We’ll see.

I feel a full review would have gotten them 2.75-3 stars, which is an upgrade from the 2.5 for their 2025 annuals.

The trend of the article now begins to change, as Pharmacorp RX (PCRX.V) is up by 17% after their Q4 and 2025 annual earnings release, finally breaking out of that long buy zone I identified in my annual Wolf Pick article.

That positive share price performance was not really related to their earnings, but the news release the day after when they announced an agreement to acquire eight additional pharmacies and a pipeline of four more under LOI. The initial eight are expected to close by end the end of Q2, with the remaining four potentially by the end of Q3.

Pharmacorp only had six pharmacies to end 2025, and by the end of Q3 that number could triple to 18.

The financials they released didn’t exactly jump off the page, losing $1.42M on $20.9M in revenues, but they were operationally cash flow positive while integrating all of these new acquisitions.

They ended 2025 with a run rate of about $31M in annual revenue, so by the end of Q3 we could see this number increase dramatically to potentially $75M or more. Unfortunately the company does not include a lot of metrics for the acquired businesses, so take my Wolf math with a grain of salt.

One of the factors that attracted me initially to Pharmacorp was their ability to improve the overall operational effectiveness of the businesses they acquire and do it in a rather short time frame. Same store sales were up by 6% in Q4, and they are able to do so in both the front (retail) and back (prescriptions) of the house. The fact they can also do this while not burning cash operationally is also very attractive.

PCRX is after all a rollup story, and if we go back to one of my 2023 Wolf Picks, NowVertical, they don’t all turn out well. I’ve always maintained the easy part of a roll-up focused businesses is the acquisitions themselves - essential buying the revenue. Where most rollups fail is in the operational and synergistic integration - this is what separates the good stories from the bad ones. This among other things is why NowVertical has suffered, or arguably failed. Pharmacorp is already showing signs of doing this much better, and pretty much immediately. While PCRX is producing some operational cash flow, they aren’t producing enough to continue on this acquisition pace without dilutive measures occurring or taking on debt. That is certainly one thing retail investors interested in this company need to fully understand, and expect. Management is aggressive and I don’t anticipate they are about to slow down.

By the time NowVertical released their Q1 in 2024, a mere five months after making it an annual pick, warning signs were very evident and I exited with a profit before the bottom fell out of the stock price. I do not see any indication of those warnings signs with Pharmacorp, so I will look to add to my position when the chart dictates.

3.25 stars.

The largest logo also had the largest success story, up 36% after earnings and 41% since selecting them as my first 2026 mid year Seal of Approval pick back in February. How is that buy zone looking now?

Back in February, Biorem was one of my higher conviction plays, citing a 54% upside ($3.73) by the end of May, and we are more than three quarters of the way there.

Unlike the others, this one occurred before I left on vacation, so I’ll leave my full review below.

Biorem Inc. ($BRM.V) FINS Review

I feel like I set this one up on a tee for everyone. Back in February I gave Biorem the Wolf Seal of Approval citing big opportunities for some upward share price moves early in 2026. Many within the…

Thanks for taking the time to read all of that. I need to plan my European holidays a little better.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Great analysis w focus where it matters, thanks Wolf !