Big financials release last night with big expectations. It feels like forever since they released their annuals which turned out to be an unexpected botch job releasing them at 2 pm. Despite the strong numbers, the market has been punishing the stock due to recession fears and customer concentration concerns. The ticker has not received the deserved respect in this writers opinion and as a result has been trading under a 5 forward P/E for much of the year, a year in which they were selected as a 2025 Wolf Pick.

The company did preview these earnings a while back, and those numbers exceeded what my expectations were. Now the actual results are here, what do they look like?

I gave their last review four stars but gave their IR and communications team two for their poorly worded press release and botched FINS drop.

This press release is much better focusing on the key metrics with a solid headline. Kudos.

Let’s get on with the review:

Paid Subscriber Benefits:

First access to annual picks, upgrades and mid year picks.

Monthly “What’s Wolf Watching” preview of upcoming earnings and potential market moves.

FinsDontLie Scholastic Series - exclusive educational posts

NEW - Access to The Wolf Den discord community (daily insights, charts, chat & Q&A)

I have the advantage of having written the above pre market, and continuing the review post market. ZoomD had a hell of a day yesterday with a 27% jump, breaking through top resistance and closing at $1.03.

It was also nice to see so many subscribers get some wins today on this one as well. As I’ve mentioned before, I’m not a fan of how the company formats their financials but as long as they continue to produce these numbers, all is forgiven.

ZoomD Technologies reports in USD

Balance Sheet:

Zoomd Technologies has a solid balance sheet with a current ratio of 2.6 that consists of $12.5M in cash, $11.7M in A/R and $150k in prepaids and other receivables against just $9.35M of liabilities due over the course of the next twelve months. Their cash position alone covers their current twelve months worth of commitments so liquidity is strong. All of their $2M debt is current, but the rate of this LOC facility is a mediocre SOFR + 4.75%. The company has no long term liability commitments outside of long term leases.

Very solid start, but if we had an A/R aging report, Wolf would be happier.

Cash Flow:

A juicy $3.5M worth of operational cash flow generated during Q1 compared to only $39k a year ago. In all of 2024, ZOMD generated $7.7M worth of OCF. It’s also notable that they did $3.5M with a $1.2M negative impact from receivables increasing which impacted working capital adjustments, so in essence it could have even been a little better.

Not much to speak about throughout the rest of the cash flow statement but overall the company improved their cash position by $3.3M or 36% from their year end three months ago.

Share Capital:

Other than 420k options exercised in the quarter, nothing much else changed. To see what I had to say after their annuals, click below:

Income Statement:

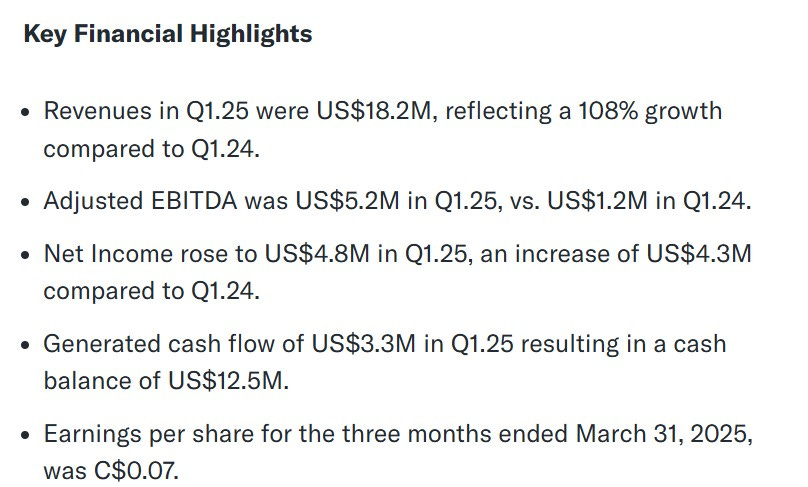

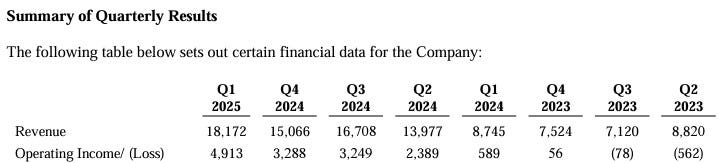

Here we go with something that I have been looking forward to for months. Revenues came in at $18.2M which is a 107% increase of the comparable period a year ago. Margins were strong at 44.3%, over 500 basis points better than they achieved in Q1 of last year which results in 134% more gross profit dollars. Better still, the company achieved those metrics while only spending 10% more in operational costs. SG&A rose by 25% which is still excelllent conversion while spending $200k less in R&D.

If you are unfamiliar with the term Wolf Trifecta, it’s achieving solid revenue growth while showing improvements in margin, and in doing so convert well on your operational spending. There is no greater example of that with ZoomD’s first quarter.

All that equates to $4.9M of net income to kick off their year which is 882% better than the profitability produced in Q1 of last year. Now I think you see why I had this as one of my top 2025 picks. That is a ridiculous 26% of net income to sales in the quarter.

Overall:

With their operational efficiencies kicking off in Q2 of last year, they are no longer up against any “softish” quarters but the outlook for another beat in Q2 of this year is optimistic.

Back to CAD, ZoomD now has $89M of revenue on a TTM basis generating $18.4M worth of net income. Even after the 26% share price jump it still only trades at an undervalued looking 5 P/E after delivering 18 cents of EPS. Ten times earnings (current, not future) is an 80% upside. Is it risk free? Of course not, nothing is but if you read my paid piece from Vegas, then you know they have mitigants in place to minimize those risks.

I’m upgrading to 4.25 stars. The numbers are just that damn good.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Just subscribed after the profits I made on Zoom - twice. I also did a review of previous email blast commentaries and compared price then vs. now. Granted, things are looking up since March but some of these have done extremely well. Thorough and entertaining commentaries. Doing my best to follow it all - tough for a retired english teacher, though I've been in the markets a long while now. Never too late to learn.

Thanks for the review, Wolf! Loving this company.