I have not reviewed Volatus in almost three years. Since I reviewed one of their competitors (Draganfly) less than two weeks ago, it felt appropriate to take another look at them too. I’ll attach that review below for comparison purposes. I didn’t win many friends with that review and my instinct tells me that will be true here also.

Draganfly Inc ($DPRO/$DPRO.C) FINS Review

I feel like I was almost dared into writing this one. Occasionally I will compose a review solely for the reason that I know it will ruffle a few feathers and piss a few others off. This is of those …

At the end of 2022, I liked Volatus enough to award them with three stars, but changed my tune six months later by downgrading them. That was my last official review of the company. Much has changed since then including the merger with serial underperformer Drone Delivery Canada back in May of 2024. More notably, the sector has been red hot.

Volatus has rewarded shareholders handsomely in the past twelve months with a return of well over 4x, from $0.17 per share to $0.73 today while reaching a high of $0.97 in late July.

The longer term five year chart isn’t so kind however showing a decrease of 50%, although that significantly outperforms the 97% erosion in share price value that Draganfly experienced during the same time span.

Once again, I’ll pose the question - is there anything here other than an exciting theme play? Let’s try to find out.

Balance Sheet:

Volatus has a healthy and liquid looking balance sheet with a current ratio of 3.8 that consists of $41.1M in cash, $3.4M in receivables, $3.3M worth of inventory and $1.8M in prepaids over top of just $13.1M in current liabilities. Their cash position alone is 3x their current one year financial commitments.

The quality of their receivables could look a lot better with more than 45% over 30 days, although there is no indication of what Volatus’ credit terms are.

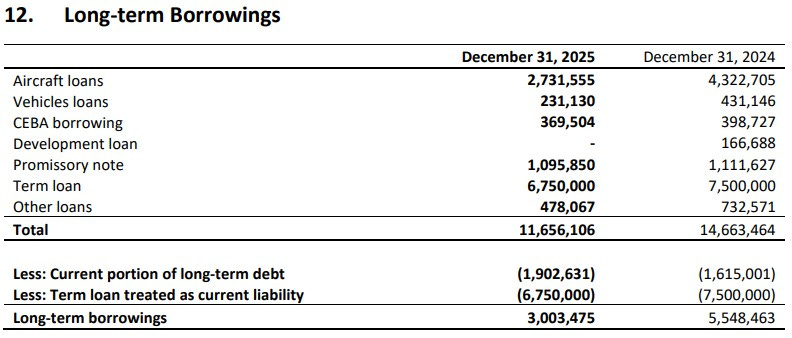

Volatus has over $19.5M worth of debt, $7.9M of those in convertible debentures with the balance in more traditional debt across seven different loans and notes. Nearly 75% or $8.65M is due in within 2026.

A good portion of this debt are under what I’d refer to as non-friendly rates and the company’s disclosure and details are severely lacking as well, only telling us the following:

Aircraft loans bear interest at rates ranging between 8.05 to 12% with expiries between July 2027 and Aug 2030.

Vehicle loans bear interest at rates ranging between 9.3% and 14% with expiries between August 2026 and June 2032

Promissory notes bear interest at rates ranging between 0% and 15.50% with an expiry in 2026 and 2029 (note 14 provides no further detail)

Other loans consist of loans maturing within the next 12 months and have an interest rate between 9% and 12%

The $7.9M of debentures have a rate of 12.5% and expire in October of 2029, and convert the principal at $0.202/share

Cash Flow:

Volatus burned $7.5M in operational cash flow during 2025, nearly a $5M improvement over 2024 when they burned $12.4M.

They also spent $1.67M on asset additions, but were much busier in the financing activities, paying down $6.9M of debt, raising $44.8M through several equity raises, received $9.2M from warrants and stock options, and an additional $2.8M from convertible debentures. I sense the next section will be busy as well.

Share Capital:

668.2M in what has become an increasingly bloated float with 43% dilution alone in the past year

16M options all ITM

9.6M RSU’s - 9.95M awarded and 382k forfeited in 2025

51.1M warrants - 36.3M ITM with the remainder at $0.76

Approx 37M in future dilutionary measures attributable to convertible debentures (principal only)

Fully diluted float including ITM items approx 767M with an implied MC of $560M

20% insider ownership, 6% institutional (per SimplyWallSt)

No insider activity on the open market in the past year

Income Statement:

Volatus achieved $34.2M in revenue in 2025, an increase of 26% over last year. Gross margin suffered on those additional sales with 270 basis points of erosion from 35.2% in 2024 to 32.5% last year. On 26% more revenue, they only delivered 16% of that to the gross profit line.

Total operating expenses grew by 27%. Cash burning expenses (depreciation, amortization and SBC removed) rose by 22%, or $3.4M. This all combined for a worsening of operating losses by 36% or $4M compared to 2024.

Financing costs relating to their debt soared by 77% YoY and after a few other one time items net losses totaled $22M in 2025, $8.7M or 65% worse than losses suffered in 2024.

When solely looking at the quarter alone, it’s worse that the total year in all aspects. Revenue was up by 7% but with gross profit erosion of 500 basis points to 33%, they delivered 7% less in gross profit dollars.

With even greater increases in operational spending and finance costs, losses from operations worsened by 165% and net losses by 107%.

Overall:

Fundamentally, choosing between the previously reviewed Draganfly and Volatus is akin to choosing between Cinderella’s step sisters - ugly or really ugly. But if I were forced to choose, FLT would come out ahead due to better margins and a slightly better history of spending and cash burn. Unfortunately those variations come at twice the market cap valuation, and Volatus is saddled with debt at higher than market rates.

Volatus has increased in market value to just shy of $500M. You get all that for a company who has $73M in net losses and over $40M in cash burn in the past five years. Additionally, while they grew revenues this year, they could not eclipse the $35M in pre-merger revenue from 2023.

In the company’s annual MD&A, they list fifteen accomplishments during the year. Only one of them relates to a signed contract of $9M ($4.5M guaranteed), while TEN of those accomplishments relate to raising capital or dilutive measures.

Post financials, Volatus up-listed from the Venture to the TSX.

What did Volatus do well in 2025? Raise capital is at the top of the list through five separate financings, and that does not include debt for equity transactions or increases to convertible debentures. That gives them a strong enough balance sheet to withstand 2025 performance levels for at least two years without additional funding.

With all of my negativity here, I’m not blind in terms of the overall bullishness of the sector. This has been apparent for several months with NATO and other countries significantly increasing defence spending budgets, and the use of drone activity in both the Iran and Ukraine conflicts. This sector is huge and is only going to grow exponentially in the next few years.

To be honest, no small cap across North America has great fundamentals, and you can throw in PARRO out of France in that mix too. They all trade at very high P/S multiples while burning large amounts of cash and suffering substantial losses.

I think we need to also discuss management’s credibility. At this time last year, Volatus was touting a $600M sales pipeline. They did so within multiple MD&A’s last year and was included in their investor presentations. It’s notable that this reference is no longer contained within their MD&A and has been reduced by $100M in their latest deck. I’ve ranted plenty on this metric usage in other reviews, but to sum it up, they are virtually meaningless without any corresponding historical metric on how sales pipelines convert to revenue. One $9M contract signed last year supports this.

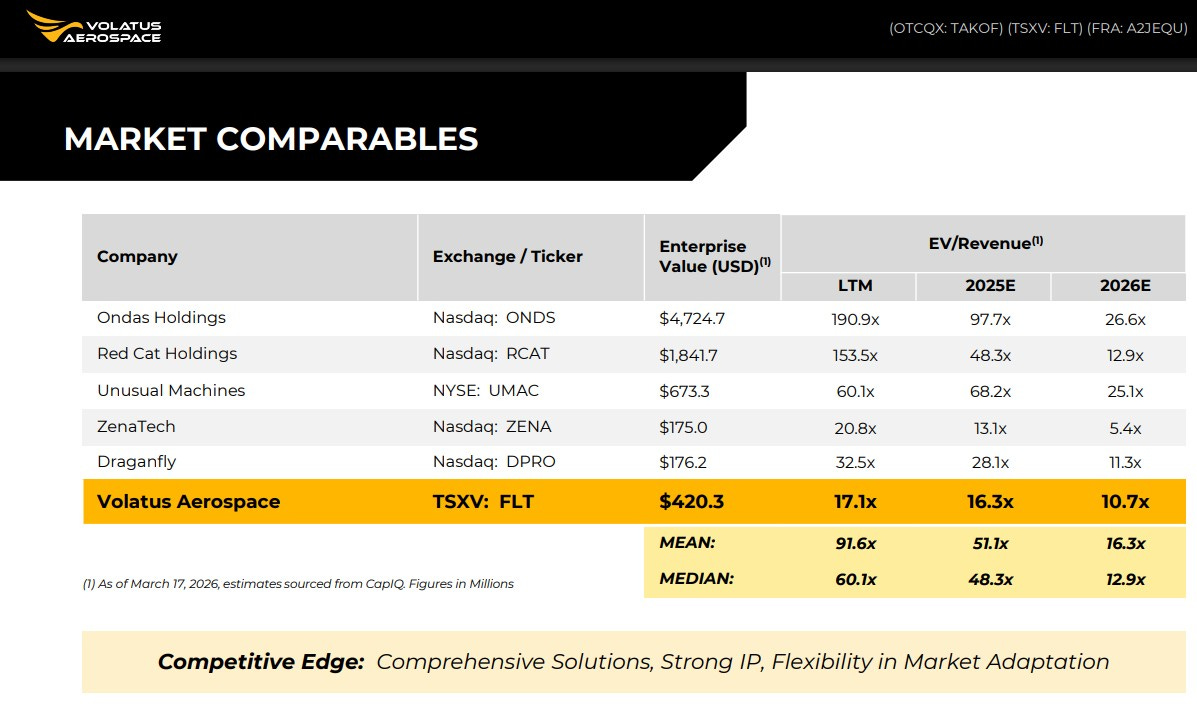

For reference I have attached the company’s latest investor deck from last month:

Ultimately I think the whole sector is tradable, with most of it being un-investable, especially at these astronomical valuations. The biggest winner in this space almost assuredly will come from being an acquisition target. Whomever guesses correctly on the who and how much may be the ultimate winner.

These two reviews have inspired my next article which will be part of my Scholastic Series. Look for that shortly.

I want to give them 1.5 stars. But I just gave that rating to DPRO and I hate them more. 1.75 it is.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

I was holding done delivery Canada before, escaped after merging, now surprised to see it 5x from the bottom price. It 'teaches' me a good theme may save a bad stock. But the odds is very low.