I feel like I was almost dared into writing this one. Occasionally I will compose a review solely for the reason that I know it will ruffle a few feathers and piss a few others off. This is of those times.

I’ve been saying this frequently off the top of my reviews of late, but once again it has been sometime since I last did a full review of Draganfly, a dual listed stock on the Nasdaq and the typically more bottom feeding CSE.

When looking at the one year chart, DPRO has had a relatively successful last twelve months, with the stock up 52%, and at one point growing by over 4x. On the flip side, the stock has lost 66% of their value since their 52 week high six months ago, creating lots of investors holding the bag, and perhaps their own.

While I have not performed a full review in two years, I have discussed them in my monthly “What’s Wolf Watching” articles for paid subscribers. I must admit when I do put pen to paper or keystroke to monitor on this company, it often results in some NSFW language. Therefore if you’re a wee squeamish, it might be best to click the back button right now.

In mid October of last year when the stock was trading near recent highs, I put them in the Danger Zone leading into their Q3 earnings.

By the day after reporting earnings a few weeks later, the stock had decreased in value by 45%. Then, just a week and a half ago, I covered them again and finished with this:

Draganfly released their latest earnings after hours on Tuesday, and yesterday the market rewarded them with a 21% decline.

Before we get into the review itself, I think it’s important to zoom out by looking left given a lot has occurred since my last review, including a 25:1 reverse split in September of 2024. While the stock trades at just under $7 (CAD) today, it traded at the equivalent of nearly $330 five years ago. That’s nearly 98% less for you mouth breathers where math may not be your strong suit.

In my December 2022 review I said, “Heck of a lot of news releases, very little meat”.

Has anything changed? Let’s find out.

Balance Sheet:

You won’t hear me criticizing the state of their balance sheet because it has never looked better. I’ll cover the why once we dive into their cash flow statement.

Draganfly sports ridiculous current and quick ratios of over twenty consisting of $90.2M in cash, $1M in A/R, $3.9M worth of inventory and $4.8M in prepaids overtop of only $4.6M in liabilities due through their 2026 fiscal year.

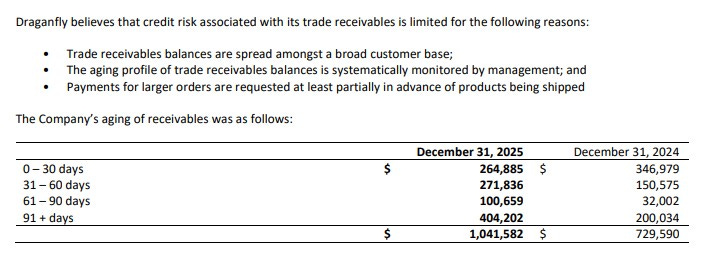

Their credit manager on the other hand may need to resort to some drone surveillance for their customers as nearly half of receivables are over 60 days.

They have no debt and very little long term liabilities.

The lowlight on the balance sheet is their $140M+ accumulated deficit.

Cash Flow:

Here is where the problems begin to surface with $23.9M worth of operational cash burn in 2025 and that figure is more than double the $11.8M burned in 2024. This likely isn’t a surprise to anyone following the company closely as they burned over $90M in the last five years.

Draganfly purchased $920k worth of equipment in 2025, but the biggest news within their cash flow statement is they raising of over $109M in net capital through financing and warrant exercises. That put the company in the position of having their current assets grow by over 11x during 2025.

Share Capital:

29.3M shares outstanding. 440% dilution in the past twelve months and a two year dilution rate of nearly 15x.

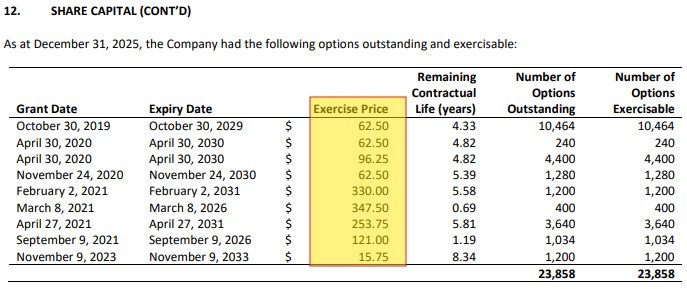

Only 24k options outstanding and by the table below it’s safe to say these are well out of the money

When a company runs a ship as poorly as this management team has, it’s no surprise to see them move away from options to a DSU model. 413k DSU’s remain outstanding. 216k vested in 2025 with 451k newly awarded.

4.5M warrants outstanding. 3.5M are just out of the money at $7.36 (CAD)

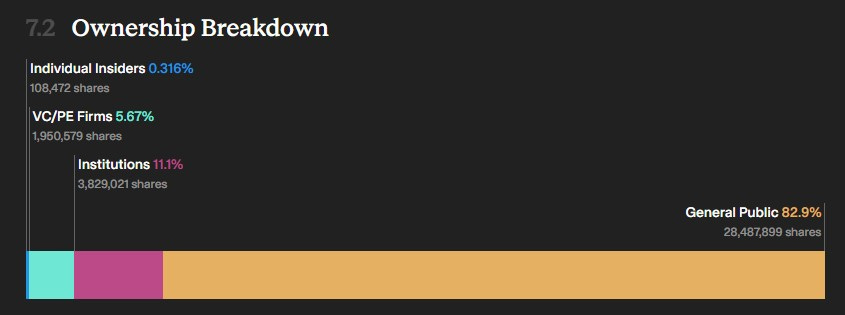

Approx 17% ownership by private equity and institutions with some of the smallest insider ownership I’ve witnessed.

The majority of insiders have been flipping their RSU awards on the open market upon being awarded.

Draganfly maintains a rolling 15% SBC plan.

The rolling part is important here. As of their Dec 31 year end, the number of outstanding shares was only 5.4M shares, giving the number of available of 814k less existing options and RSU’s for 595k available. 413k were awarded.

With the current share count of 29.3M and using the same formula, 3.96M RSU’s will be available to award in 2025.

Income Statement:

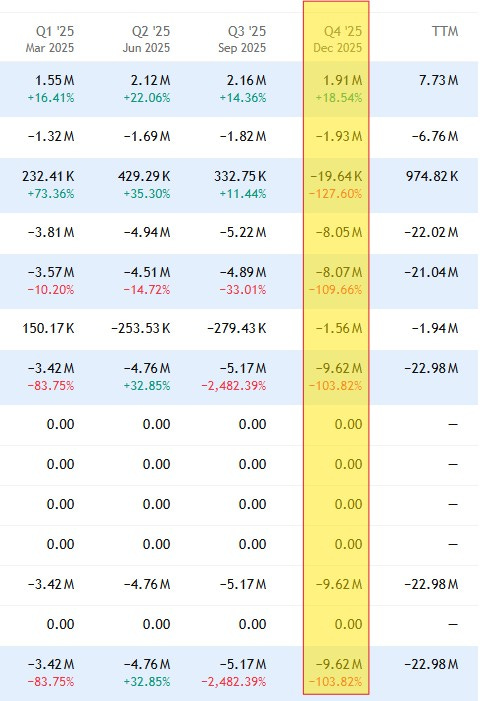

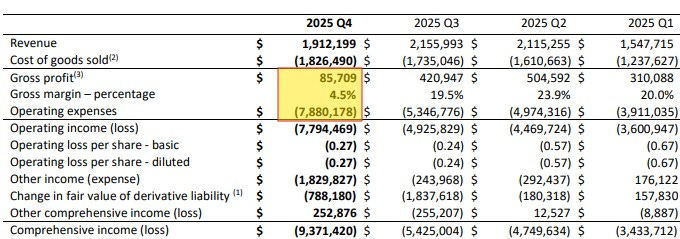

We’ve reached the part of the review where things begin to go south in a hurry. DPRO’s top line for 2025 came in at $7.7M, and that is an increase of 18% over 2024. Unfortunately, gross margin decreased by over 400 basis points down to 17.1% and that actually resulted in the company taking 5.5% LESS dollars down to the gross profit line on 18% more business.

Total operating expenses soared by 34%, nearly double the rate of their revenue increase to over $23.5M and the vast majority of that was cash burning. That resulted in an operational loss of $22.1M and a net loss of $23M, the latter amount 66% worse than the net loss of $13.9M experienced in 2024.

As for their Q4, it grew over the comparable quarter by 18.5% but was down sequentially by 11.6%, and their quarterly net loss of $9.6M was the worst the company experienced since Q4 of 2022.

A more detailed look highlights only 4.5% of gross margin. Nearly $7.9M of operating expenses, 93% more than last year to generate $86k in gross profit dollars. Their operational cash burn in the quarter was $9.7M. That’s $39M annualized and trending very poorly.

Overall:

If you read this far, and I forgive anyone who bailed at my intro, I was expecting their financials to be bad. Somehow they exceeded those expectations, and not in a good way. I was three quarters of the way through the review before I realized their Q4 was as bad as it was.

Let’s just start with a simple break even analysis. To be kind let’s go with their annual numbers. At 17.1% gross margin, to offset Draganfly’s level of spending would have required just shy of $134.5M in revenue. They achieved $7.7M or 5.7% of the revenue required to offset expenses. To make matters worse, revenues were down QoQ on low single digit margins while their spending in Q4 was double what it was in Q1. For fun their B/E point in Q4 would have been over $209M in revenues, or $836M annualized, more than 100x what they actually achieved.

Does Draganfly have anything going for them? Yes. It goes without saying that they operate in a very hotly themed sector - Drone technology. They were able to parlay that, along with the stupidity of investors to raise over $100M in capital. Amazingly, post financials, they raised capital again, this time for gross proceeds of over $68M through 5M shares and 2.1M prefunded warrants. Effectively the company is now sitting on approximately $150M in cash. That makes their cash runway enormous, even with their Q4 burn rate approaching $10M.

With the vast majority of those prefunded warrants also exercised, that puts their new share count around 36.5M, increasing that level of dilution to about 570% since the start of last year and takes their market cap to around a quarter billion CAD. When I referred to stupid investors - those that participated in that raise just over a month ago are currently down by 28%.

That $250M market cap is only about 1.5x their current cash on hand, but it is also over 32x their 2025 revenues. They are way too unprofitable to talk about P/E or EV/EBITDA ratios but their ROIC is at a staggering -45%, showing how ineffective they have been utilizing capital.

One of the most confusing things to me is their lack of capex spending given the hundreds of millions of dollars raised. Draganfly has not built or acquired a significant owned manufacturing infrastructure. Instead, it relies heavily on contract manufacturing partners. Strategically, this seems problematic and short sighted.

Earlier I shared a quote from an old review citing “A heck of a lot of news releases, very little meat”.

Since their annual filings last year, the company has put out more than fifty news releases. I’ve attached some of the more interesting ones (click the image for the full news release), but I still contend very little meat as no drone quantities or dollar figures are ever disclosed. I’ve also attached Draganfly’s latest investor deck.

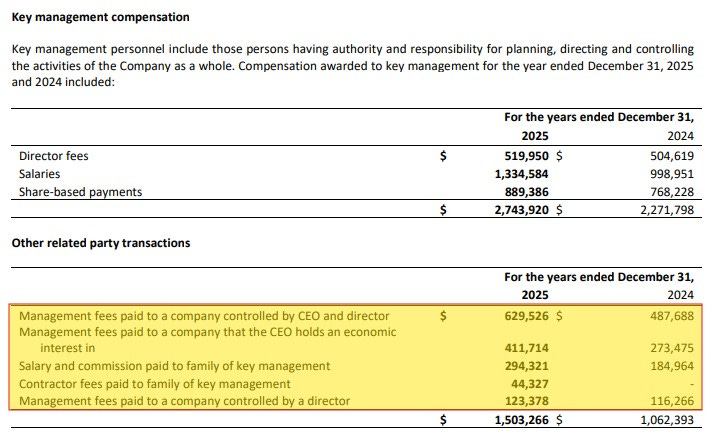

The group of people who should be the most bullish are management themselves. With the cash war chest they have on hand, they can continue reaping the rewards shown below including related parties and even family members for a few more years. Let’s also remember none of them have any significant skin in the game with insider ownership at .32% (per multiple sources).

Let’s put a bow on this. Normally, this type of epic bedshitting performance would easy garner a one star review or less. But the $150M or so cash on hand with virtually no liabilities does give them a long window to eventually find themselves. Couple that with a sector that is only going to get hotter with increased defense spending across the globe, and the current Iran and Ukraine conflicts showing just how much of a future drone technology has in surveillance and warfare, and it’s hard to write them off completely.

1.5 stars with a hope and a prayer for the massive amount of bagholders in Draganfly. I gotta say I thought I would have used more foul language. Next time.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

That's A LOT of dilution.

Btw, the paragraph starting "Let’s just start with a simple break even analysis" is just mindboggling.

I would never have thought of it in those terms, so thanks for breaking it down for us!

Thanks wolf these reports saves me allot of time and you can't replace time. Time is the most valuable thing. Keep up the good work.,