I needed a hiatus from cannabis stocks over the past few months. I’m not quite back to the abhorrent disdain that I had on the industry as a whole a few years back, but my current sentiment is lukewarm at best.

Selecting HASH as a Wolf Pick will do that to stock picker, as have subsequent positions (since exited) on more encouraging and better performing businesses such as LOVE and ROMJ. Thankfully, and pardon the pun, many of the poorly run businesses in the cannabis space have been weeded out.

Several microcaps in this space have proven to be better operators. While each has their own warts, the previously mentioned Cannara Biotech and Rubicon Organics fall into that category as do others such as Auxly Cannabis. Glow Lifetech has been trying to join that group, although their model is slightly different than the others.

My first and only review of Glow was last June after their first quarter which received a below average two stars. The stock is down 17% since then. A large reason for that sub par review was their float management and share based compensation. Just two days ago I penned an article on the value destruction of Canada’s microcap drone industry. I could have easily written the same article using microcap cannabis stocks as an example.

During the review I noted not only did Glow experience 3x dilution over a five quarter span, but they had 60M ITM warrants expiring over the next nine months. In multiple subsequent conversations on the stock, I stated that five cents was going to be a continual magnet until they expired. I may have also coined the phrase “nickel humper”. You’ll never guess where the price sits today, a day after posting their 2025 annual financial statements.

I have also felt that Glow could be an interesting swing opportunity once the last of those warrants expired, even referring to them in my annual Wolf Pick article in December. I felt that there were at least three potential catalysts to potentially push the stock in a northern direction between late March and late May. First was the expiration of those final 40M or so warrants and then their two sets of financials ending with their Q1 of 2026 sometime next month. Well, two of those potential catalysts are now in the rear view mirror, and the stock is still hanging on to that five cent figure.

Did Q4 disappoint? Let’s find out.

Balance Sheet:

While the figures are small, the overall state of their balance sheet is solid. They have a current ratio of 2.2 that consists of $1.4M in cash, $444k in A/R, $430k worth of inventory and $250k in other short term assets against just $1.2M in liabilities due over the next twelve months with no debt and just $11k in long term liability commitments.

Unfortunately the company does not provide any details surrounding the state of their receivables but the good news is their current cash position covers their one year liabilities.

Cash Flow:

Let’s call Glow operationally cash flow neutral with just $15k worth of cash burn in 2025, quite the improvement over the $1.35M burned in 2024. They also improved throughout the year with positive OCF over their last two quarters totaling $174k after burning nearly $200k in the front half of 2025.

During the year they also received $560k into the treasury from warrants and options, eliminated all of their $326k of debt and made $100k in asset investments.

Overall, they modestly improved their cash position by 6% during the year.

Share Capital:

181.3M shares outstanding with 7% dilution during 2025

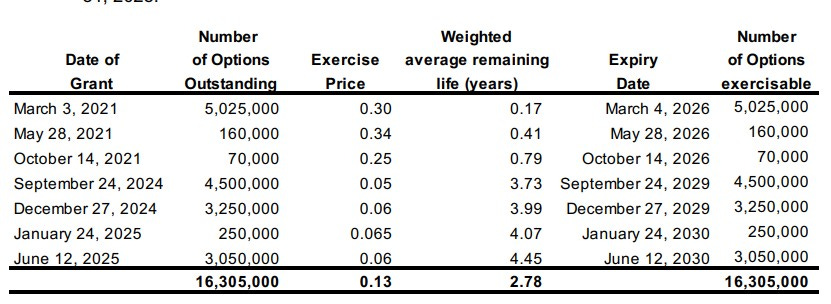

16.3M options, none ITM with 4.5M at today’s price. 5M would have already expired post financials on March 3

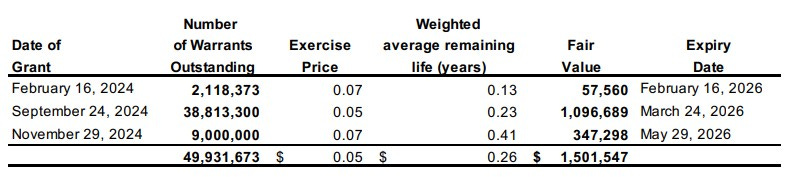

At Dec 31, 49.9M warrants WERE outstanding. As of today, that figure is 9M. 10.9M were exercised post financials with a little over 30M expiring unexercised

31% insider ownership with the majority of that owned by their strategic partner, Swiss PharmaCan

No activity on the open market, and multiple insiders chose to pass on exercising those 5 cent warrants

Income Statement:

Glow hit a milestone in 2025 eclipsing the two million mark in annual revenue finishing with $2.05M, a 146% increase over 2024. A pretty impressive mark considering they were pretty much a pre-revenue company for the front half of 2023.

While margins were strong at 66.3%, it was a 440 basis point decline over the 70.6% they achieved last year. So on 146% more revenue, that delivered 131% more gross profit dollars.

Total operating expenses actually came in lower than 2024 by 1.6% and that may be a bigger highlight than their revenue performance. When non-cash burning expenses are stripped out (amortization, deprecation and SBC), operational costs did rise by 40%. The biggest savings was from a 65% ($300k) reduction in share based compensation. That shouldn’t take away from the excellent operational leverage they did get within G&A (4.6%) and Manufacturing costs (3.3%). Selling and distribution expenses from commissions and advertising did rise significantly (161%) but overall there is reason for encouragement with only 40% more cash based spending on a 146% revenue increase.

Overall, they were able to halve their operational loss from a year ago, $727k vs $1.53M.

Like their cash flow performance, things look much improved in the back half of the year as well, losing $184k in the final six months compared to $559k in the first six with a quarterly best $78k loss in Q4.

Overall:

As a whole, I think anyone would have to concede that Glow Lifetech had a fairly successful year with many achievements. The revenue jumps out clearly, but they also eliminated what remained of their debt, achieved positive cash flow in both quarters down the stretch, significantly shrunk losses as the year progressed and had a much cleaner outlook on their float as they entered 2026.

But.

One can’t ignore their QoQ performance which was down by over 19% from Q3. Perhaps I have not read everything that the company has put out since their financials were released, but if they addressed this, I’ve missed it. Distributing to retail will undoubtedly create some revenue lumpiness (Q2 was lower than Q1 too) but 19% does feel rather significant. That upcoming Q1 which we expect to see next month that initially looked like a slam dunk - perhaps now not so much.

I still sense that overall Glow is headed in a very good direction however as we could see a similar rebound like earlier in the year. They have over 2000 more distribution points (stores x sku’s) heading into ‘26 than they did in ‘25, increased their presence post financials in two provinces and had their first entry into the Canadian medical channel.

So we have a $9M market cap here trading at a 4.5x annual revenue but not yet there to introduce any profitability metrics. How much are they worth? I’m not sure I have a number in mind, but I’ll end with this. One year ago on April 9th, the stock traded as high as 7 cents, and are currently at 5 If you liked them then, you should like them a lot more today as they are a much better looking company at a 29% discount from a year ago.

I’m upgrading them. I want to give them three stars but holding back. Maybe next month’s Q1 with continued progress. Swing play at the very least seems very much in play.

2.75 stars. Let your Soul Glo.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Thanks for the review... I too am up in smoke with HASH... perhaps a sell/buy 1 for 1 investment in GLOW will assist in my portfolio recovery.

Thanks for the review, Wolf. The company's turnaround seems promising, but I've been burned before with these types of stocks (I know they're not the same, but I lump GLOW with HASH and other cannabis stocks). I'm staying out.