You have to go way back to November of 2022 when Vitalhub became one of the first companies to ever receive a four star review. They traded at around $2.25 per share at that time and I also picked up some shares shortly afterwards. I exited for approximately a 200% gain back in the middle of 2024, only to see the stock to continue on a much higher ascent, peaking at close to $15 at one point last summer.

Fast forward to the spring thaw of 2026 and Vitalhub’s valuation has melted to the tune of 54% in the past eight months, leaving many in this unenviable position:

For a long time, I’ve felt Vitalhub was been trading well ahead of it’s fair valuation. But at some point this downward slide has to start to reverse. Right?

When I first glanced at their final financials of the 2025 fiscal year I thought we could be nearing that time of price recovery. We are now a week later and the stock is down 8%. Has it reached the bottom? Let’s take the first deep dive I’ve performed here in some time.

(The remainder of this article is for paid subscribers. The paywall will be removed March 31)

Balance Sheet:

Vitalhub possesses an elite level looking balance sheet with a current ratio of over 6.6 with deferred revenues removed. They have $57.6M in cash, $61.6M in short term investments, $22.5M in receivables and $3.9M in other short term assets against just $21.9M in liabilities due throughout 2026.

Vitalhub owes $14.6M in deferred taxes, and had $4.65M in consideration contingencies from acquisitions but holds zero debt. The company does have up to $65M in credit available through the Bank of Nova Scotia.

VHI does not provide an A/R aging report for their $22M+ in A/R but they do have a $775k credit loss provision.

Cash Flow:

As is usually the case with Vitalhub, their cash flow statement has plenty of activity.

The company generated $8.3M of operational cash flow in 2025 and that figure is down 45% from 2024 when they generated $15.1M. That continues the downward trend from 2023 when their OCF was $20.5M.

VHI also increased their short term investments by $61.5M, used $14.5M to acquire Induction Healthcare and $35.5 on Novari Health. They also raised capital twice in 2025 for proceeds $103M as well as $2.2M were received on the exercise of options,

In total, they ended the year with over $63M more in cash and investments than they started with.

Share Capital:

63.2M shares out with 20% dilutive measures in 2025 and 45% over two years

3.2M options outstanding with 345k granted and 827k exercised this year.

132k DSU’s

Approximately $175M remaining under their base shelf prospectus announced in July. Nearly $75M has been raised under the base shelf at $12.70 (ouch)

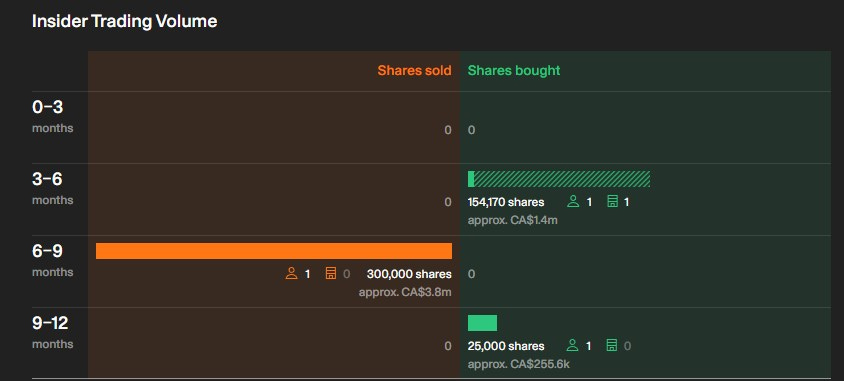

11% insider ownership with 34% institutional.

More insider selling than buying in the past nine months. Selling interestingly occurred a week after their August raise at $12.75 with the buying occurring in December around $9.

Income Statement:

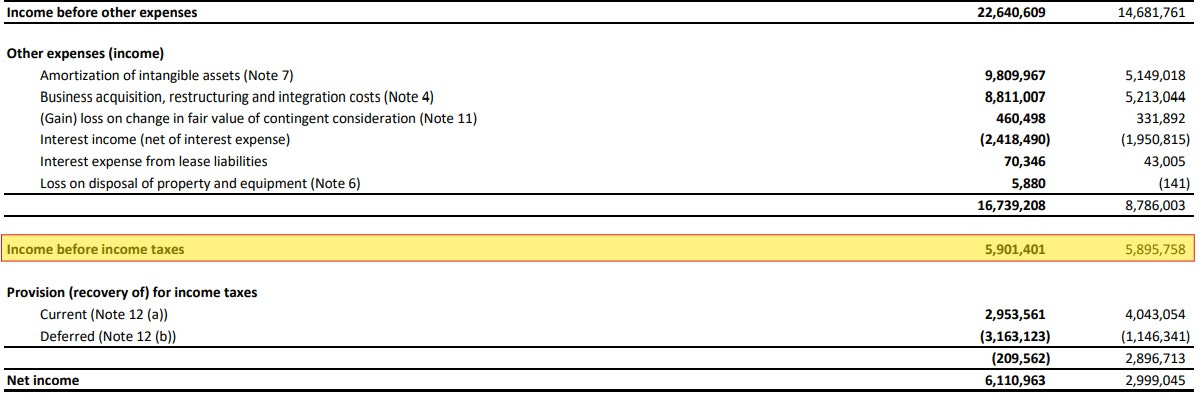

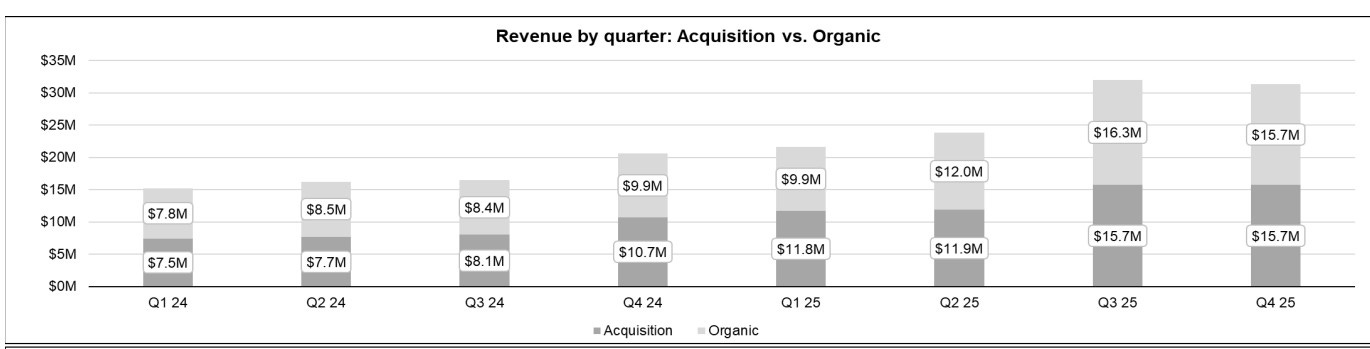

Vitalhub eclipsed the $100M revenue mark for the first time achieving $109M, a 59% increase over 2024. Gross margins continue to be greater than 80% but they were 50 basis points lower YoY coming in at 80.4%. Gross profit dollars increased by 57.8%.

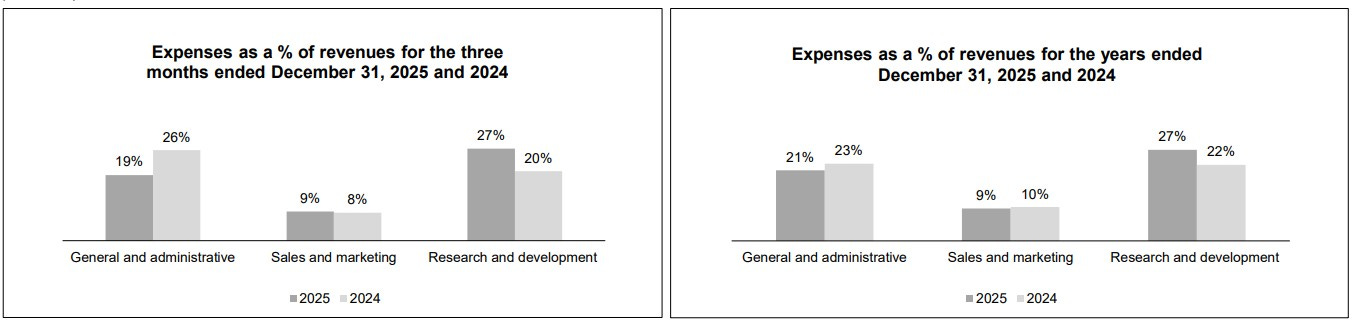

Cash burning expenses grew at a much higher rate than either revenue or gross profit to the tune of 65%. Their three main expenses buckets are G&A which rose by 45%, Sales and Marketing by 52% and R&D spending soared by over 90%. That by far now is their largest P&L expenditure totaling 26.6% of revenues.

While their net income did more than double to $6.1M, that had more to do with additional tax deferrals. Prior to income taxes, their profitability was virtually flat on 59% more revenues.

That has to feel like a lot of work up top to deliver so little on the bottom.

Overall:

Even after this greater than 50% drop in share price over the past eight months, the valuations don’t exactly jump off the page as something extremely cheap. A P/E ratio of 70 and 53x cash flow with a more reasonable looking EV/EBITDA number of 14.

On the flip side, they have looked a lot more expensive at times in the past few years at much higher multiples.

Regardless of what you think of their current valuation, they have and continue to be one of the bigger small cap success stories of the past decade going from zero to $100M in revenue since 2015. I’ve been known to say the following when it comes to “roll-ups” or “serial acquirers” - the easy part is buying revenue and the more difficult part is transforming these acquisitions into profitable businesses.

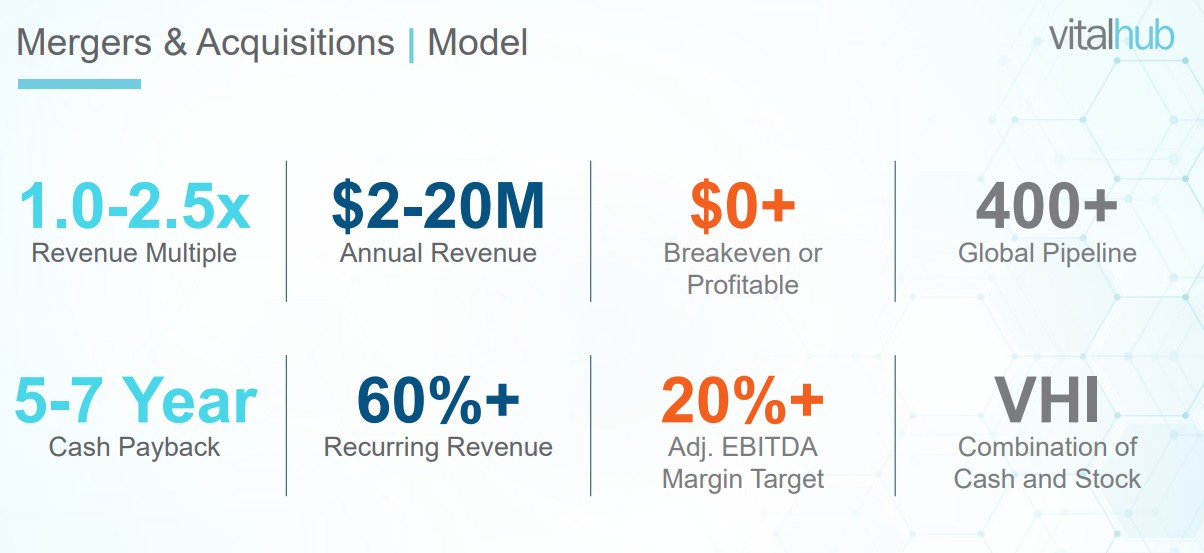

This is what the last decade of M&A activity has looked like for Vitalhub, and they suggest they target companies with 1-2.5x revenue multiples with a 5-7 year cash payback and 60% recurring revenues.

Outside of the recurring revenue, I find little evidence that the company is following their own M&A model, particularly when it comes to their cash payback or adjusted EBITDA margin targets. Their two acquisitions in 2025 were Novari, who were “break even” on the AEBITDA line and Induction who had an AEBITDA loss. The 2024 acquisitions did not list any profitability numbers upon being announced. Given that their last two years of operational cash flow dropped by 44% last year and 26% the year before isn’t helping any of those cash payback numbers. I also don’t like that all of their contingent considerations are solely based on revenue targets.

I’m likely bordering on being overly critical here, but that’s because they just aren’t living up to their own playbook and that slide above has been in their deck for as long as I can remember. One part of keeping management accountable is making sure they live up to what they say, and the metrics suggest they are not. Maybe it is time to update the fucking slide.

Let’s don the more bullish hat now. Outside of this latest quarter, Vitalhub has been doing a pretty good job with organic growth.

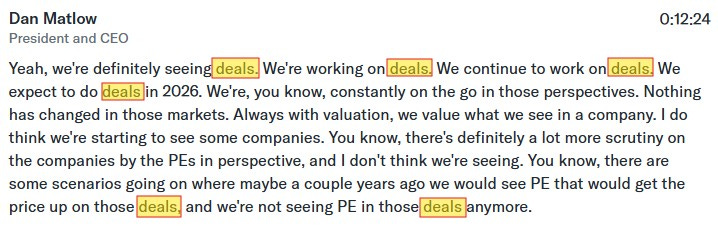

While the company does not provide forward looking guidance, analysts are generally expecting organic growth at 10% which puts them near $130M in 2026. This is of course before any additional M&A activity, and if you’re wondering whether they are thinking about making additional “deals” I’ll just leave you with this quote from their conference call.

If you normalize their organic earnings and cash flow, you could add back just the $8.8M from acquisition and restructuring costs to come up with a little more reasonable metrics of a 30 P/E and 26x cash flow. This is of course before additional synergies. Those potential synergies remain significant when you take into consideration recurring revenues of $93.7M which is 86% of total revenues and very high margins of over 80%. Their R&D spending is also impacted from acquisitions. That additional R&D spend this year as a percentage of revenue is equivalent to another $5.5M in potential cost savings. I just wish Vitalhub would provide better guidance around some of their future spending. As usual the analysts on the conference call doled out more verbal fellatio than hard hitting questions.

Vitalhub also has a tremendous looking balance sheet and $120M in near term liquidity to be able to pull off some significant M&A opportunities when they arise. Their current market cap sits at less than 4x cash on hand,

For some further reading, I’ll attach an excellent article published in the middle of last year by Simeon Capital which really dives into the nuts and bolts of what Vitalhub does. Below that is the company’s latest investor deck.

In summary, I do like Vitalhub in this area as it is teetering on the 200 weekly moving average. The squeamish investor could place a stop loss somewhere below that line for safety.

I feel an $11 price target by the time we review their 2026 annuals isn’t out of the question and that represents a 55% increase from this potentially lucky $7 price tag.

While these financials are not the clean four stars that I looked at three and a half years ago, they are still worthy of 3.5.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.