A $7.5M market cap you say? Well they all have to start somewhere. A few requests have come into the Wolf Den discord after TTZ reported their annual financials earlier in the week. It would seem like the requests have some merit, as the stock has gapped up on three consecutive days since their FINS dropped.

For the year Total Telcom is only up 6%, but it has risen by 53% in the last month. Their daily trading volume is also noticeably different in the past few months, although it’s hard to classify them as highly liquid with their largest volume day of 244k shares in the twelve months.

So who is Total Telcom?

The name for starters can be a little confusing as this isn’t your Mom and Dad’s traditional telco. They provide satellite based communication focusing on poorly covered areas across a number of verticals. Click on the image above for their full investor deck which is unfortunately over a year old now.

The five year chart is a little less impressive, down about 50% from their November 2023 high. In fact the company has been publicly traded since 1999 and was founded on February 18th, 1980. That was four days before the “Miracle on Ice” at the Lake Placid Olympics, and well before Mrs. Wolf was born.

So why now? Do their financials indicate this has more room to run? Let’s find out.

Paid Subscriber Benefits:

First access to annual picks, upgrades and mid year “Seal of Approval” picks.

Monthly “What’s Wolf Watching” preview of upcoming earnings and potential market moves.

FinsDontLie Scholastic Series - exclusive educational posts

Access to The Wolf Den Discord community (daily insights, charts, chat & Q&A)

Balance Sheet:

A current ratio of over 14 (15.5 with deferred revenue removed) is one heck of a start. At the end of their fiscal year, the company has $3.2M in cash and term deposits, $305k in A/R, $281k of inventory and $13k in prepaids against just $266k of short term liability commitments. They are debt free with only lease commitments within their long term liabilities.

The company’s A/R aging is adequate and they greatly improved their inventory turnover this year.

Ok, they have my attention.

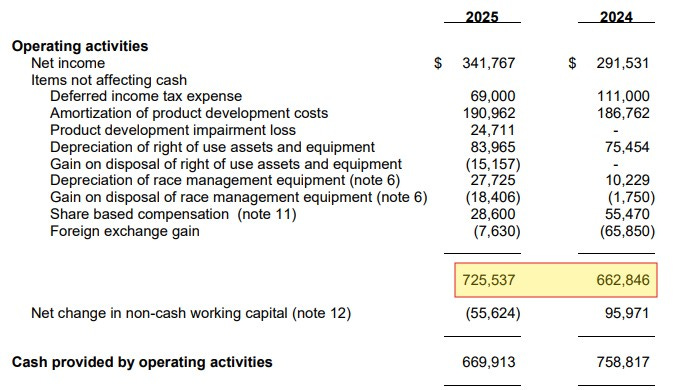

Cash Flow:

Total Telcom delivered $670k of operational cash flow in 2025. That was 12% less than what they did in 2024, but when you back out the minor working capital adjustments in both years, it grew by 10%.

They spent $250k in capitalized development costs during the year and socked away $385k worth of their cash flow in additional term deposits.

Overall they increased their cash and equivalents position by 15% during the fiscal year.

Share Capital:

26.4M shares in a well managed float with zero dilution last year

1.1M options outstanding, 700k of which are ITM under a shareholder friendly SBC plan

33% insider ownership per the company investor deck. That leaves approx 19M shares available everyday on the open market. With the low daily volume it suggest that the majority of those are in very strong hands

$12k of insider buying in the last twelve months - all from sitting director and small cap legend - Paul Andreola

Income Statement:

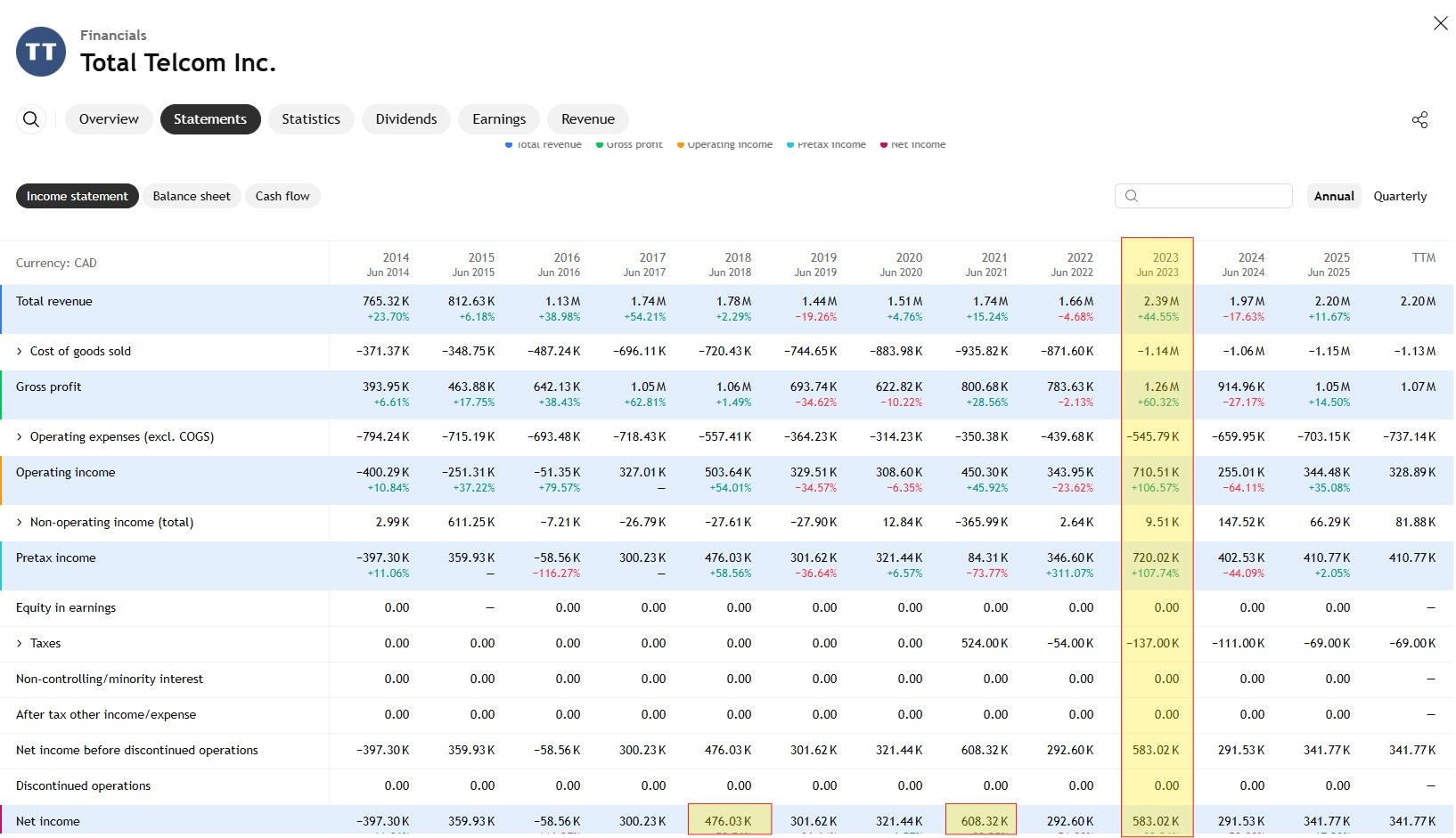

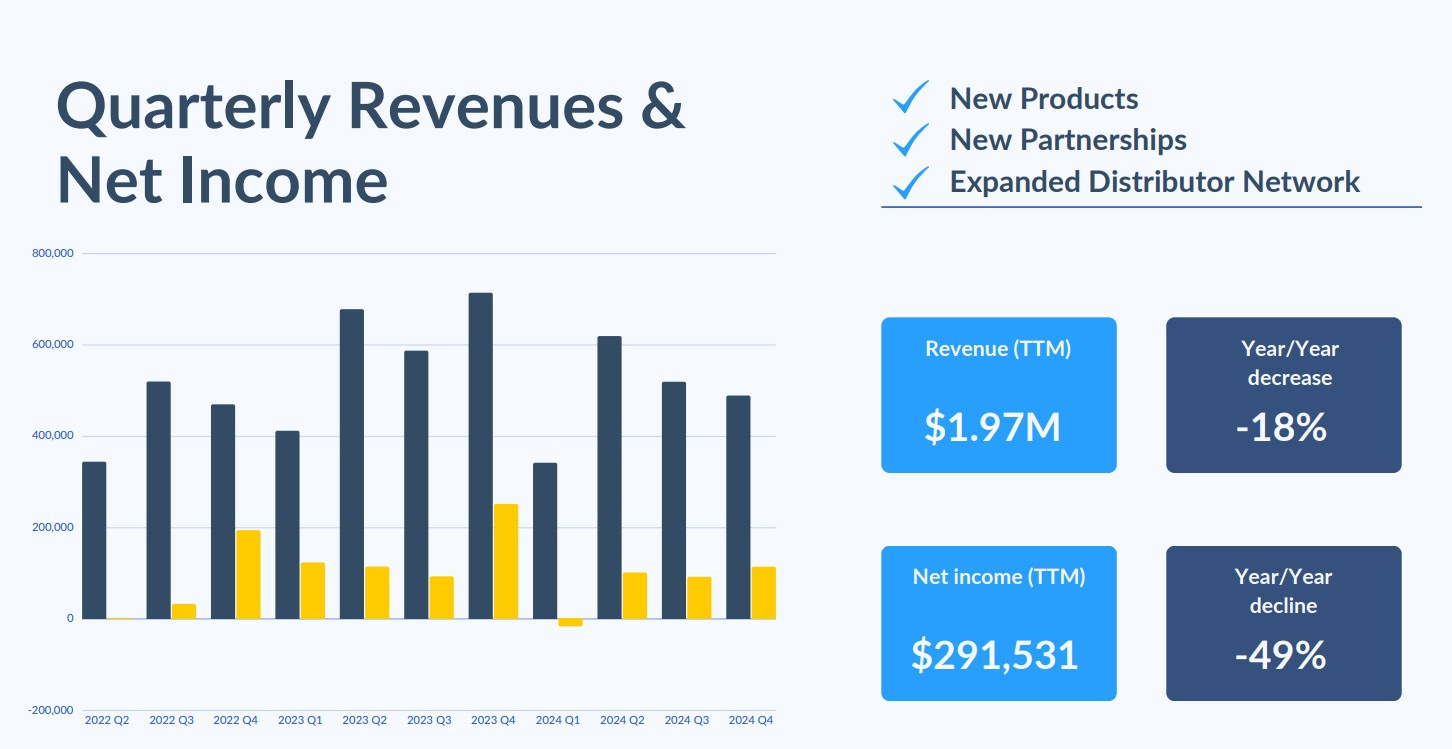

Total revenue for their 2025 fiscal year was $2.2M, a 12% increase over what they did in ‘24. That top line also comes with some sexy gross margin, 60.9% and that number is up by 110 basis points above the 59.8% from a year ago.

They also converted decently on spending. Total expenses rose by 11%, but cash burning expenses (all under the G&A umbrella) rose by 6.7%. It’s not the biggest Wolf Trifecta I’ve witnessed but under my definition, still qualifies.

They did have a $58k bogey in foreign exchange gains year over year which is significant on $2M worth of revenue, but that was almost made up for with a $42k birdie in deferred income tax expenses.

Overall that translates to $341k in net income, a 17% increase over what they achieved last year.

It’s also notable that the company has some significant losses carried forward which will decrease their tax commitments over the next few years.

Overall:

There isn’t much in the way of anything to criticize within these financials and I always try my best to find something.

On the full year, it is trading around a 19 P/E based on yesterday’s close, but if you annualize their last six months, it works out to a 12.5 P/E. That could be a very exciting metric for a company on pace for exponential growth.

That is where the questions start to arise for me.

Total Telcom achieved a 12% increase in 2025 over 2024. But if you look back just one year earlier, it’s 9% less than what they did in 2023. They have also had three years when their profitability was higher than what they did here as well. So while they are growing over time, it is far from a consistent and reliable state of growth.

It also makes me question their aged investor deck even more, as this is the financial highlights they are exposing potential investors to in the midst of having 25% or more in quarterly revenue growth in three of the last four quarters. This is not endearing - why hasn’t anyone thought to update this deck in the last twelve months?

Another factor is that more than two thirds of their business is done in the US and will be impacted by the ongoing and unpredictable tariff situation, but to what degree is difficult to assess.

Outside of telling me the TAM (Total Addressable Market) is going to grow with a CAGR of 32% over the next half decade, I’m not seeing enough on how the company plans to get out there and get their share. And if the 32% CAGR is an accurate number, isn’t 12% revenue growth significantly underperforming the sector and suggest they’re losing market share. That’s what it suggests to me.

I want to like TTZ more, but they haven’t given me a reason to, at least not yet. I get they’re a small organization and likely lacking some IR communication resources, but they’ve also been publicly trading for a quarter century. I’m willing to listen to someone else’s bull case to convince me otherwise but I’m not seeing anything that makes them more than watchlist worthy here.

3.25 stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.