Multiple requests from the Wolf Den discord for another review of Snipp. Sometimes I feel like my subscribers can be masochists, deriving some sort of pleasure from yours truly tearing apart a potential shitco they might be interested in.

I last reviewed Snipp after their third quarter back in early December (attached below for reference). I awarded them a mediocre two and a half stars then. Their overall numbers were not terrible, but there were several intangibles that left me uninterested. Snipp has a bloated executive structure matching their outstanding share count. To satisfy the egotistical nature of their job titles is a retail unfriendly 20% option based share based compensation plan.

Snipp Interactive ($SPN.V) FINS Review

First review of Snipp. Typing that makes me want to cross my legs and protect myself for some reason. The five year chart also makes you want to protect your groin area.

I also noted in that most recent review the company’s penchant for cease trade orders (CTO’s) and late financial filings. Well guess what? The company is currently under a halt situation once again and has been since May 8th. I find a couple of things curious about this. The halt came only one week after their filing deadline. Typically the regulators will allow some extra time to file (a month or more) and usually grant an MTCO to limit insiders from activity in the open market. That didn’t happen, moving straight to a full CTO less than ten days overdue. The company then filed their annual statements only eight days later and recently caught up with their Q1 filings on Monday which was only a few days late. We are now three days later and the regulators have not allowed Snipp to continue trading yet. Were the regulators just being cautious here due to these jabroni’s history of failed filings, or is there more to the story? I suppose we’ll know soon enough.

In terms of the share price prior to the halt, it is down 35% since my last review and over 50% from recent highs back in April of 2024. If you scroll further left, the chart gets much worse.

Let’s get into the numbers themselves.

Paid Subscriber Benefits:

First access to annual picks, upgrades and mid year Seal of Approval picks.

Monthly “What’s Wolf Watching” preview of upcoming earnings and potential market moves.

FinsDontLie Scholastic Series - exclusive educational posts

NEW - Access to The Wolf Den discord community (daily insights, charts, chat & Q&A)

(Snipp Interactive reports in USD)

Balance Sheet:

With deferred revenue removed, Snipp has a strong current ratio of 3.2 consisting of $5.8M in cash, $1.4M in receivables and $1.55M in other short term assets against just $2.8M of liabilities due within the next year. Snipp’s cash position alone doubles their short term commitments so there liquidity is quite strong. The company also carries zero debt and only has $456k in long term liabilities related to long term lease commitments.

Zero issues thus far.

Cash Flow:

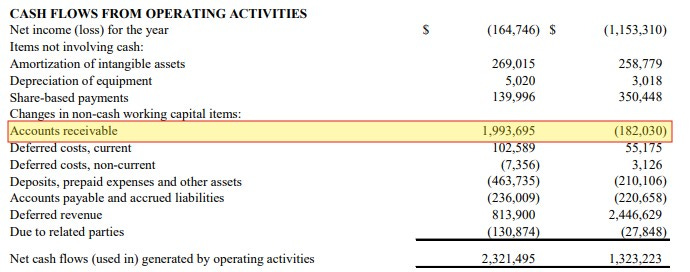

Snipp produced an impressive $2.3M of operational cash flow (OCF) in the first quarter, $1M better than the comparable quarter last year.

This number is heavily influenced by working capital adjustments, in particular from a great A/R collections quarter, as their receivables dropped from $3.4M to $1.4M from their year end. While the OCF is impressive, it’s unthinkable it would continue to trend in this direction for the full year.

Aside from operational activities it was a pretty uneventful quarter within investing and financing activities, so overall Snipp improved their cash position by a healthy 56% in Q1.

Share Capital:

286.1M shares outstanding in a rather large, liquid float but zero dilution over the past twelve months.

A staggering 37.6M options outstanding including 19M options granted in this recent quarter alone under the company’s recently renewed 20% SBC option plan. I discussed my distaste for this plan in my last review and this recent egregious activity only solidifies that. Only 5M of that total figure are currently ITM.

32% insider ownership and 9% ownership from Bally’s (NYSE: BALY) per the company investor deck. Bally’s purchased 25M shares at 25 cents back in April of 2022 for $5M USD. That is now valued at $1.9M CAD. Ouch.

Insiders have been allergic to participating in the public market, but why would they when they hand out options like McDonald’s hot cakes at Fat Con?

Income Statement:

We’re off to a hot start with revenues of $6.4M in the quarter, a 37% improvement over last years $4.66M.

While the company does not report an actual gross margin number within their financials, they do speak to one in their MD&A, and they define it in this fashion:

In using the above figures, margin improved by 550 basis points to 59.9% in Q1, which delivered an impressive increase of 51% additional gross margin dollars on 37% more revenue. Expenses aside from their defined COGS (Campaign infrastructure) rose by just 6%, with actual cash burning expenses jumping by 15% which is still excellent conversion on 51% more margin dollars.

Overall that still left the company just shy of break even with a net loss of $165k, but a very notable improvement over the $1.15M loss suffered in the comparable quarter from 2024.

Overall:

By my own definition the company achieved the Wolf Trifecta of double digit revenue improvements, margin gains and very good conversion within their controllable expenses.

I can’t help but make comparisons to another company I’ve covered frequently of late and that is Neupath Heath (NPTH.V). While the operational model is obviously vastly different than Snipp’s, I see a lot of similarities within the financials and valuations.

Both organizations are growing at a decent clip, on the cusp of having a profitable business, producing positive cash flow and both are valued substantially lower than one on a P/S ratio (.59 in Snipp’s case). In both cases I can opine that if they just did xy and z correctly, there is a profitable and attractive business model to be had. The opportunity may even be better in the case of Snipp Interactive, as I feel Neupath is limited within their margin opportunities and operational cost model.

The flip side is the trust factor. With the company’s history of late filings and regulators halting trading on multiple occassions, that is enough for potential investors to pause. Now I have seen decent companies have complicated audits that cause delays in microcap land before. It happens. But there is a pattern here, and when you list five guys in the C suite, one would have to question their level of competency for this to become a regular occurrence. When you add the fact they also have a very retail unfriendly 20% SBC plan, and felt their historical level of performance warranted a grant of 19M options in a quarter while their stock was halted, speaks volumes. That also occurred while any long term retail investor is holding a very large bag with the share price down 57% since June of 2023.

Awarding them a slight upgrade to 2.75 because of the improved financials, but I trust this management group about as far as I could throw a Fat Con attendee.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Thanks for the review, Wolf. Despite the trifecta, I'm staying out of this because of the SBC plan & late filings.

Thanks Wolf nice comparison to neupath and yet late filings after oayfare, hash concerning. Keep up the great work.