What a journey for this stock, myself, the following over on the TSA discord among many other bulls following this roller coaster over the past few years. My first review of SBBC was back in June of 2022. While the fundamentals of the business were never fantastic, I was among many who were bullish about their future, particularly TruBar, and I gave them the Wolf seal of approval in Dec of 2022 as a 2023 annual pick. After that I must say it was a year or more of frustration watching them waste marketing dollars on PureKana like a teenager sitting in perverts row at For Your Eyes Only (IYKYK).

My last review was more than a year ago and it received a downgrade to two stars as they had a lot more issues than just marketing spend. Due to the move to Substack and their failed migration promises, links are not working for pre migration reviews. Each new company I review on Substack, I’m bringing over the most recent or other relevant review from the archive (click below).

After getting out and then calling a nice bounce from the low, I sold my position in late February for a small profit. Of course several weeks later they announced what I wanted them to do for a long time - toss that marketing pig PK and focus their efforts on TruBar. Since then I’ve basically treated them like my ex wife - didn’t even want to look at it.

But the market gets what the market wants. So let’s take a look at their Q3. Headlines look as tasty as a “Day Dreaming About Donuts” bar. Even though they were a 2023 Wolf Pick, SBBC has never received more than a 2.5 star review. Is it time?

Note: SBBC reports in USD.

Balance Sheet:

I have a little tear in my eye, it, it, it, it’s so clean.

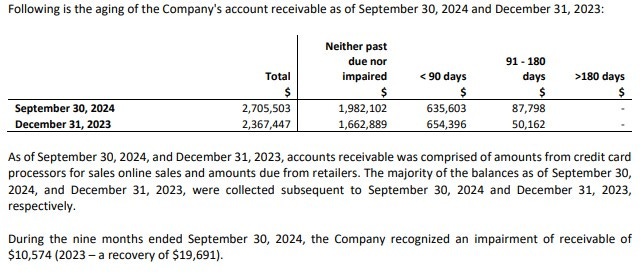

The current ratio nine months ago was a grotesque looking .53. Today it sits at 1.28 and if you remove the non cash burning warrant liabilities, that much better. As of their quarter end, they have $3.7M in cash, $2.7M of receivables, $4.6M worth of inventory and $1.3M of other short term assets against $7.1M in liabilities (cash burning) due over the next twelve months.

Due to the corporate restructure, the company has significantly improved the look of their debt, with $1.8M in their revolving credit facility and $3.7M of promissory notes. The notes, held by insiders carry a high interest rate of 15% (a little greasy) so it will be nice to have those off the books.

Receivables look a little shaky with 27% over 90 days past due. So far this year they have written off only $10k, but it looks like that figure could grow rather substantially and perhaps hit Q4.

Inventory looks very clean and turnover ratio has dramatically improved given their revenue performance.

Cash Flow:

Simply achieved positive cash flow from operations of $1.2M, and this is more than a $2M turnaround from a year ago when they experienced operational cash burn of $953k through three quarters. There is some back and forth with working capital changes so I think it is too soon to call them a cash flow generating juggernaut, but investors should overall be very pleased with the progress.

A lot going on within the financing section of their CF statement. The company raised nearly $4.5M through a PP, warrant and option exercises. They paid down net debt of $6.1M, and incurred nearly $2M in net debt via promissory notes.

Overall, they have improved their cash position by nearly 60% from the beginning of the year.

Very solid turnaround.

Share Capital:

Still reasonable looking float of 93.8M shares with 30% dilution occurring during the last nine months

1M ITM warrants outstanding at 46 cents

SBBC has a 10% incentive plan with 4.2M outstanding. All but 100k are ITM and 3.8M were granted this year

2.8M RSU’s outstanding under the same plan

20% insider ownership (per Yahoo Finance)

Insider participation has been positive. There were multiple insiders who participated in the May raise, many open market buys (most notably Erica Groussman’s $260k September slap), in addition to exercising options

Commercial Break:

Income Statement:

The rest of the stuff has been great but this is where the sausage is made.

The revenue line is a two handed monster jam. It came in at $12.1M, 126% better than a year ago. Through nine months they are up nearly 30% to $31.6M but the third quarter represents over 90% of their YTD increase.

If you like nice margin stories and I’m sure you do, gross profit rate was up to 45.3%, nearly 500 basis points better than the same quarter a year ago. YTD shows a bigger improvement over 2023 but the important part is that 45%+ trends so it appears this could be the new baseline.

Expenses are a little all over the place and if there is any criticism it’s in here. Cash burning expenses (removing SBC & amortization) were $4.39M compared to last years $1.94M, an increase of 126%, much more than discussed in the MD&A due to a reduction in non cash burning items. Important distinction. Basically no conversion as revenue was up by the same rate. G&A costs were up 4.5x, Marketing was up 266% (flashbacks) and consulting and professional fees 272%. That marketing spend doesn’t include $3M in vendor discounts which comes off the top of net sales.

So if we remove the noise of the one time items (warrant liabilities and impacts of discontinued operations), SBBC would have shown a Net Loss of $6k for the quarter compared to a loss of $1.2M. The main news here is after a 126% revenue increase and 500 basis point improvement performance, they were basically break even. So if you’re wondering why the company only spoke to Adj EBITDA rather than real profit, there you have it.

Overall:

I can’t talk about Simply Better without talking about the incredible news flow since the summer. They launched or expanded the TruBar brand into the following retailers:

GNC including online

Whole Foods

Lowes

Kroger

CVS

Walmart (Canada and USA)

Love’s gas stations and rest stops

GMP chain stores

Albertson’s under multiple banners

DTC sales driven mostly by Amazon was up over 250% to approximately $1.7M in Q3. Notably this segment is responsible for 14% of business but drives 20% of the company marketing spend.

The revenue train will not be slowing down any time soon, and a $100M 2025 certainly seems to be in play for this $44M (USD) market cap company. Based on these bouncing balls on the expense line, it does make it tougher to peg a potential valuation - a task I bet larger competitors will be considering at some point as this has all the hallmarks of a potential future take-out target. The marketing spend after their history with the PK brand makes your ass pucker, and the company does a rather piss poor job explaining the individual expenses lines within their MD&A. I would expect these launches to carry extra marketing expense and the costs of getting in the door in some of these behemoth brands could explain the consulting and professional fees. G&A costs rose 450% due to ecommerce fees and $100k in travel. No where do I see that any of these are one time expenses. If revenues rise to $16 - $19M next quarter, will these expenses grow at the same rate? If so, that lowers a potential valuation. Even at break even, a 1.5 revenue multiple isn’t offside, so a $150 USD market cap if they deliver triple digits in revenue next year feels in the cards.

With all that said, SBBC is back on the menu. I fully expect this to gap up at open so I won’t be slapping at the bell, but I will be watching to see where this settles in. Big upgrade from where they have been to 3.25 stars - with potential for more upgrades in the future. Q4 and 2025 could blow this one out of the water.

Have a request to review a stock you are interested in?

Paid subscribers have priority status to request financial reviews of stocks they have interest in. Request via DM or email me at thewolf@wolfofoakville.com

Chat with me and 3000+ other members daily in the TSA Discord.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

I would expect marketing expense to go in tandem with revenue for at least next few Qs and company operating at breakeven because it's 100% focused on growth (and FWIW I think it's the right strategy right now). The goal is to scale up as fast as is possible without dilution/overleveraging. Being asset-light is huge + in this case.

BTw They hinted on a call that 20% EBITDA margin could be a normalized number if they stop investing hard for growth.

Thanks! Great read and intriguing company.

" and $1.3M of other short term assets"

What is included under this?

I couldn't find these numbers in the balance sheet. Would be happy to learn.