There is the odd occasion when I sit down to write a review and think to myself, “Is anyone going to give a shit about this one?” This is one of those times.

Not a great lede for a 2026 Wolf Pick, but after some initial fan fare after making it a selection in mid December sending the stock up by 130% over the next two weeks, there hasn’t been very much to get excited about since. That includes a mediocre 2.75 star review back at the end of January for their Q3. The stock has now come back to reality sitting up just 3.5% from the pick, well off the average of 42%.

Now that I’ve adequately lubed up your sensory glands with anticipation, let’s get into the review.

Balance Sheet:

Pudo finds themself in a similar position as they did at the end of their third quarter. A current ratio of 1.9, but light on cash with receivables making up 70% of their current assets. Since these are annual financials for a stock on the junior exchange we must also account for the fact these numbers are 3.5 months old - the end of February in this case and the first quarter of 2027 ended in May.

So as of Feb 28th, Pudo had $242k in cash, $905k in receivables and $142k in other short term assets against just $675k in short term liabilities. The company also maintains no debt OR long term liabilities.

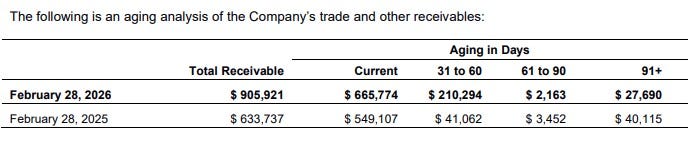

Their aging report was a little worrisome last quarter but has improved slightly with only very minor amount over 60 days and the total amount is down by $180k over their last three months.

Cash Flow:

The bad news is Pudo burned through $505k in operational cash flow during their fiscal year. The slightly less bad news is they only burned $7k in Q4 after their worst quarter of the year in Q3 when the burn rate was $300k. 80% of that burn was due to working capital adjustments, mainly from the increase in accounts receivables. Therefore it isn’t as bad as it looks, but it’s still far from good.

They invested $35k and had a raise of $101k during the year. Sadly, overall they burned through two thirds of the cash on hand they had to begin the year.

With less than a quarter million in cash to end the year, this burn rate is unsustainable, and will need a big turnaround in the first half of the year to avoid a raise of capital.

Share Capital:

33.3M shares outstanding, 22% dilution over the past year due to a raise and debt settlements

3.6M options outstanding, with 350k expiring unexercised in Q4. 1.7M are ITM but do not expire until Jan 2030. With the treasury being light, will insiders early exercise some of these options with the stock price currently double the $0.14 option price?

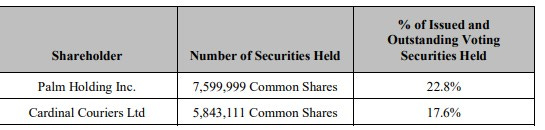

Approximately 50% insider ownership with the top two shareholders being private companies - Palm Holding and Cardinal Couriers

Insiders were major participants in their March 2025 raise and debt settlements

No Sedi filings since March of 2025

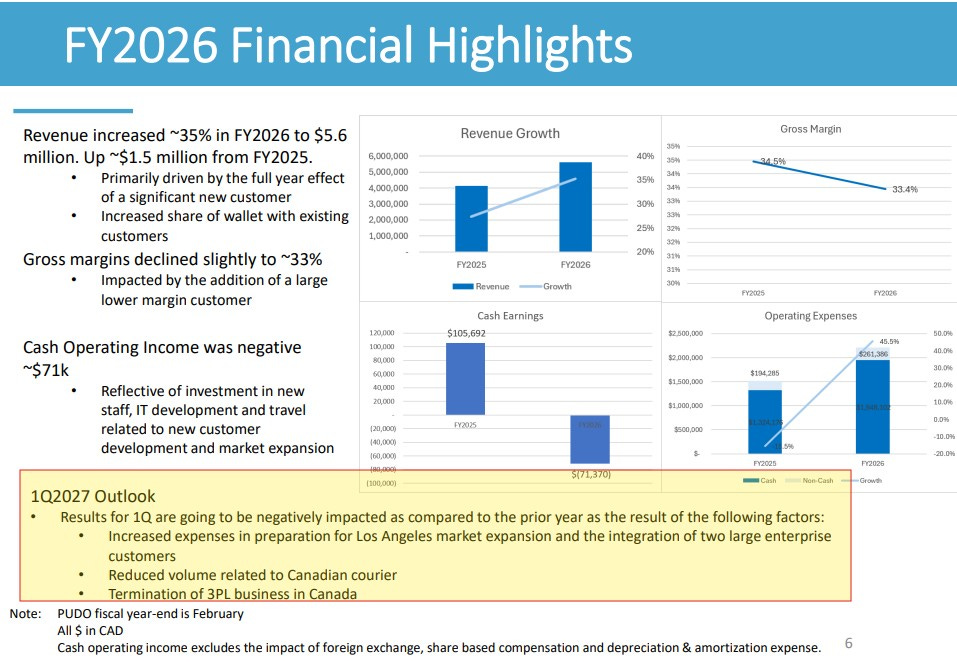

Income Statement:

A relatively successful top line performance on the year with a 35% increase in revenue to $5.6M and that came with a slight drop in margin of 100 basis points to 33.4%. Gross profit dollars as a result grew by 31%.

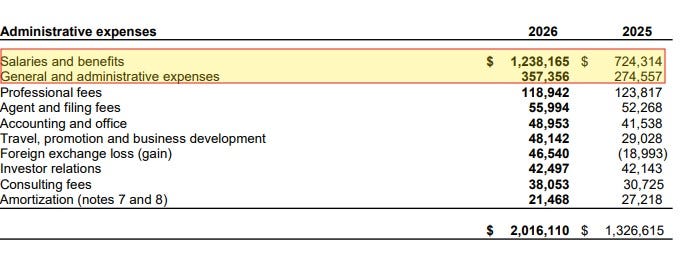

Unfortunately the company did not gain any operational leverage last year as Admin expenses rose by 52%, a significantly higher rate than their revenue or GP dollar gains. Their top two expense buckets, payroll and G&A rose by 71% and 30% respectively. Salaries and benefits to related parties grew by 3.5x. Really?

This all results in a quadrupling of their losses from a year ago, $332k vs $82k.

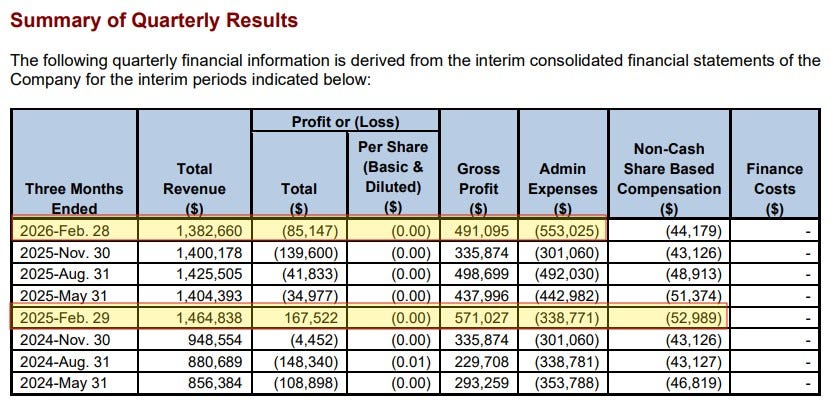

Q4 results were not more encouraging. Revenues came in at $1.38M, down by 5.6% and the worst performing top line quarter of their last five. While margin was above their annual total at 35.5%, it was off last year by 450 basis points, leaving gross profit dollars off by 14%. To add insult to injury, admin expenses grew by 63% leading to a reversal of profitability of $167k last year to a loss of $85k this year.

This is a clear definition of a reverse Wolf Trifecta. This makes Wolf unhappy.

Summary:

There is no putting lipstick on this pig of a quarter and a terrible back half of the year after what was a rather encouraging first half.

The thesis of the Wolf Pick was a growth story that could turn them into an acquisition target, as has happened with their competitors. Management is aligned with this thinking as well - they have a goal of moving on and cashing out.

Unfortunately that thesis starts to fall apart when you stop growing, have margin slippage and spend a shit ton more on in expenses. The comments in their deck for Q1 are not exactly encouraging either, particularly given their cash position and risk of burn, setting up a potential need for a raise.

They go back into the watchlist pile here as we see where their Los Angeles expansion takes them. Q2 may be the tell if this growth story can still remain intact.

Downgrading from 2.75 to 2.0. But hey, at least I’m not deleting the channel like some other discords have with their annual picks.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

"at least I’m not deleting the channel like some other discords have with their annual picks."- best zinger in Wolf review -Priceless :)