It’s always an exciting time when one of my annual Wolf Picks reports earnings.

After selecting them as one of my 2026 picks, the stock gained 50% within 30 days but has since pulled back to a more reasonable 20% return.

Usually I’m expecting great things, but that isn’t the case this time around. This is some of what I had to say last month in my earnings preview What’s Wolf Watching article.

We are now an hour into trading after the company reported earnings after the bell yesterday, and as expected the stock has retreated 6%. Keep reading to find out why I’m on the bid to increase my position, despite a negative surprise.

Balance Sheet:

Progressive Planet has a healthy current ratio of 2.2 consisting of $2.15M in cash, $1.3M in receivables, $2.5M worth of inventory and $300k in prepaids against $2.9M in current liabilities that will be due over the next year.

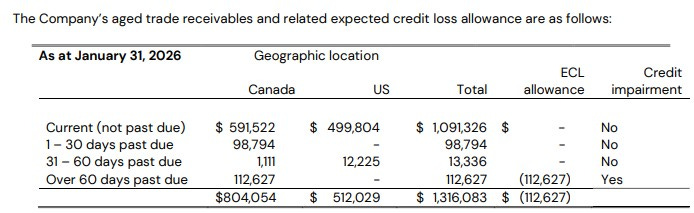

The company’s aging report looks quite similar as last quarter with 83% listed as current (87%), and $113k allowance for a write off due to customer bankruptcy.

Progressive Planet has $5.6M of debt, the vast majority under a 23 year mortgage with BDC at 5.05% interest. This replaced a BMO revolving demand loan therefore this change offers them more flexibility.

Overall they are slightly less liquid then they stood three months ago, but overall in good shape, with a bonus influx of cash post financials through the receipt of two grants.

Cash Flow:

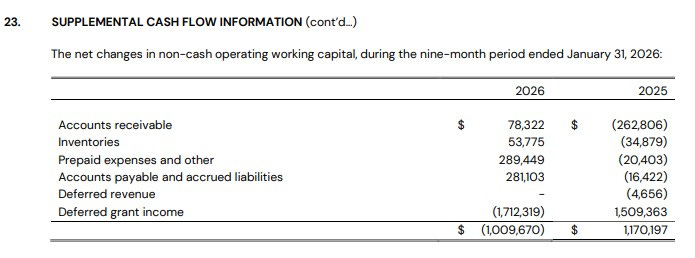

PLAN has generated $2.12M of operational cash flow, and that is down by about a million and a half from the $3.66M generated at this stage last year. This is quite the trend reversal - as of their Q2 financials, they were ahead of last year’s pace by 49%.

While this may appear to be a yellow flag, this can easily be explained due to timing of grant income this year over last. Without grant income, they are still outperforming last year and we know from their subsequent events, $1.4M were received earlier this month. I expect their Q4 will be much improved.

Big investments this year, nearly $5M in total with the majority of that for automation equipment for legacy businesses and building improvements for their PozGlass pilot plant. $1.07M was offset through grants. They also spent $605k in investments in another public company, adding a few shares within the last quarter it would appear. They have a $162k unrealized gain as of the end of January. PLAN has also reduced their debt by $643k YTD and received an influx of $75k to the treasury via exercised options.

Overall their cash position has depleted by 60% since the beginning of the year.

Share Capital:

110.2M shares outstanding. 2.35M less shares than two years ago through share buy backs - all of which occurred in their previous fiscal year with the stock in the ten cent range

8.5M options outstanding. All but 600k currently ITM but those are only 1.5 cents out of the money as of this writing. Approx 1.9M ITM options at 27.5 cents are set to expire in June.

8.3M warrants expired unexercised last year at 36 cents - none remain outstanding

30% insider ownership (per Yahoo Finance)

Small sale of stock in January by the CEO, but those funds appear to have been utilized to exercise stock options in the same group of filings

Income Statement:

The company achieved $5.8M in revenue in their third quarter, a 22% increase over the prior quarter and their second highest revenue quarter in their history. Part of these gains offset the 9% decline the company had in Q2 due to shutting down three of their four production lines for factory upgrades and the launch of new sku’s. This pushed some sales from late Q2 into Q3 as expected.

Gross margins soared by nearly 600 basis points to 34.2% (28.4% LY), and that helped to drive nearly 47% more gross profit dollars on 22% more business, as more operational efficiencies have taken effect.

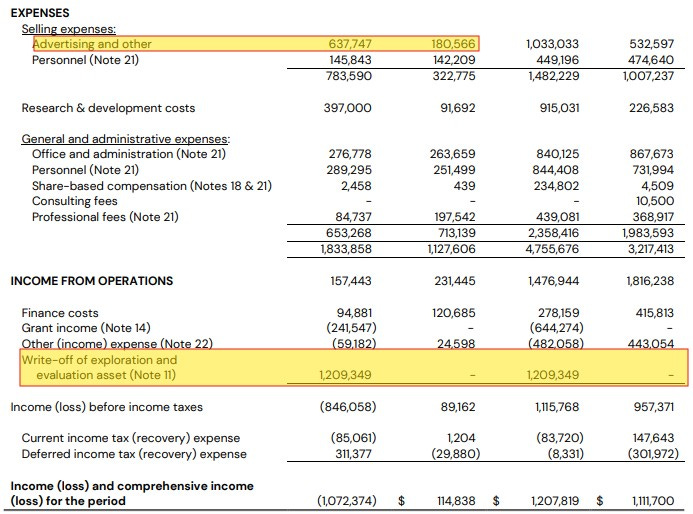

It does get a little messy underneath the gross profit line however. Two line items are the cause - one was expected this quarter but the other wasn’t.

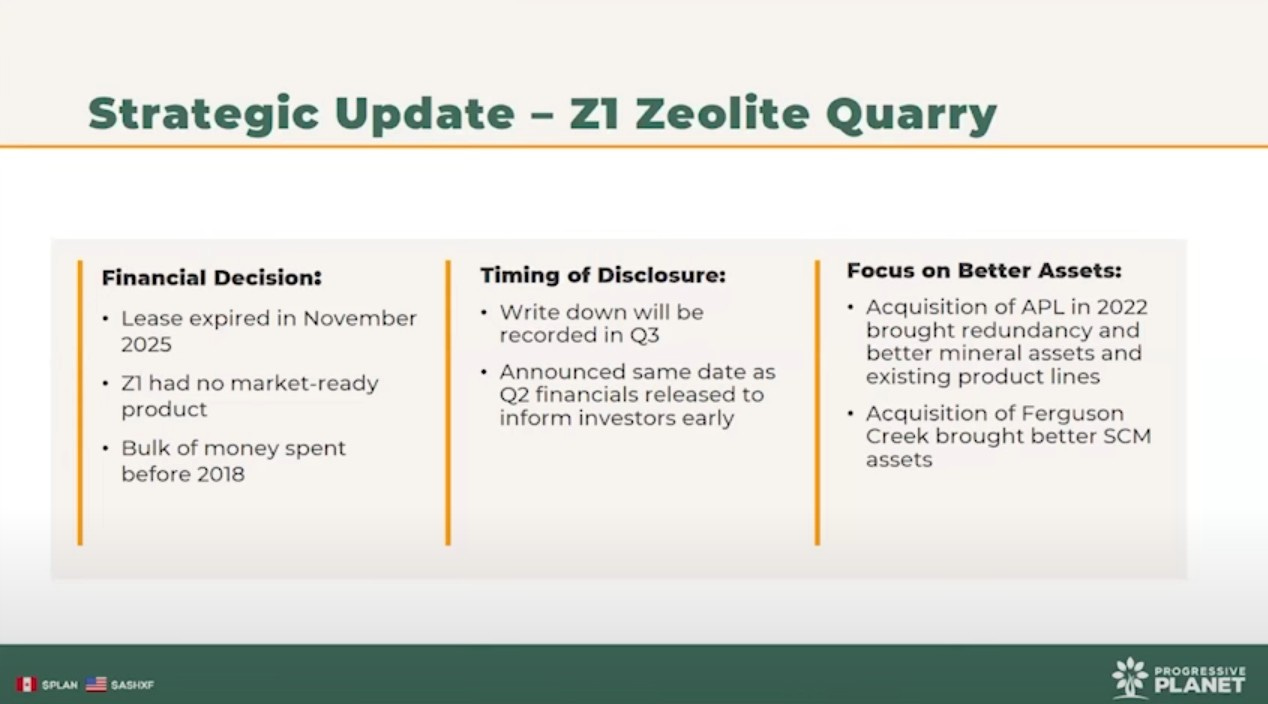

The $1.2M write down of their Zeolite Quarry was announced in late December when the company released their Q2. This was the main rationale for putting the company into the Danger Zone category in my latest WWW article.

The $450k in additional advertising spend was a surprise however. That line item alone was the main driver in rising their total operational costs in Q3 by 63%. Obviously that is terrible conversion on 22% more sales and 47% more gross profit dollars.

R&D costs were also up by $300k during the quarter, but this has been the trend all year and related to their PozGlass pilot.

When you get to the net income line it results in a loss of $1.07M vs net income of $114k last year.

On a YTD basis:

Revenue up 12% to $16.7M

Gross margin up by 360 basis points to 37.3%

Gross profit dollars up 24%

Operational expenses up by 48%. Main drivers are similar line items in the quarter - Selling expenses up 47% and R&D up by 4x to $915k

Net income up 9% to $1.2M

Overall:

Slightly disappointing quarter due to the surprise one time slotting costs, which also impacted cash flow in the quarter.

Despite that and the $1.2M non cash write off of the Zeolite quarry, their net income is still up 9% YTD. Remove that asset write down and their profitability would have more than doubled at the three quarter pole of their fiscal year.

The slotting fee, while negatively impacting the quarter, should have long term positive impacts in doubling their sku presence. The estimated $400k fee does sound unusually high, but unfortunately the reality is a $37M market cap company isn’t going to have much leverage going up against someone like Home Depot.

The fact is once you start to normalize some of these figures including ad costs, R&D and one time items, I believe my long term thesis still holds up well. Even with these hiccups the company still put 7% of revenues on the net income line, grew it over last year and are showing solid cash conversion.

PLAN is well underway with their PozGlass pilot plant with all equipment stalled last month with another update expected at the end of this month with some production happening by the end of their fiscal year - April 30th.

You can always refer to my annual Wolf Pick article for additional information on why they made the cut as a 2026 pick.

I am on the bid for more shares this morning and maintaining my 3.5 star rating.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.