I’m making the assumption before we dig into these Q1 financials that it will be brief since I recently covered them in my Mother of All Reviews for their Q4.

PCRX is part of the batch of my 2026 Wolf Picks, currently up 20%, peaking at 29% recently after announcing their big acquisition plans at the end of April.

Let’s check in on their Q1 progress.

Balance Sheet:

The balance sheet looks incredible with a current ratio of 9.4 consisting of $23.4M in cash, $1.2M in A/R, $3.1M worth of inventory and $93k in prepaids overtop of just $2.9M in liabilities due over their next twelve months.

But that cash will not be in the treasury for very long with their announced plans to acquire eight pharmacies in Eastern Canada for an announced price tag of $24.2M. In that same announcement they also revealed four other pharmacies under LOI. Just last week one of those letters of intent turned into a definitive agreement to acquire an Ontario location for $8.2M.

Doing the simple math (24.2+8.2) is $32.4M. They ended Q1 $9M shy of that figure in order to close those two deals. Where will that shortfall come from?

Pharmacorp’s A/R looks healthy with 84% current and no other issues arising from their balance sheet that look problematic.

PCRX has $3.2M of debt, all borrowed against a $20.5M credit facility which has a $10M accordion feature at a monthly variable CORRA rate (currently 2.25%). I think that leads one to believe where those additional funds are going to come from - tapping much deeper into this credit facility.

Cash Flow:

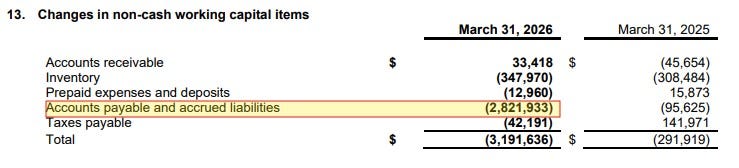

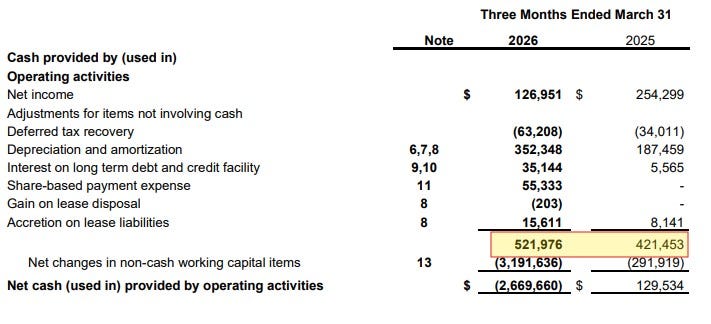

Pharmacorp burned $2.67M of operational cash flow during Q1, but I wouldn’t get concerned with that number as the company had $3.2M of negative impact from working capital adjustments, almost all arising from paying down their A/P by more than half. It sat at $5.2M at year end three months ago, and $2.4M today.

I’m much more encouraged that their operational cash flow was $521k to the positive prior to working capital adjustments, and that figure is up 24% YoY.

Minor activities within the financing and investing side during Q1. Overall their cash position depleted by 10% in their first quarter, but we know both their cash flow and balance sheet will look significantly different when they produce their Q2 in August.

Share Capital:

174M shares outstanding, with 48% dilution during the past five quarters

28.4M warrants outstanding, all just ITM at $0.50 expiring in Nov of 2027 from last November’s raise

9.3M options, all ITM but none expiring for 6 years plus

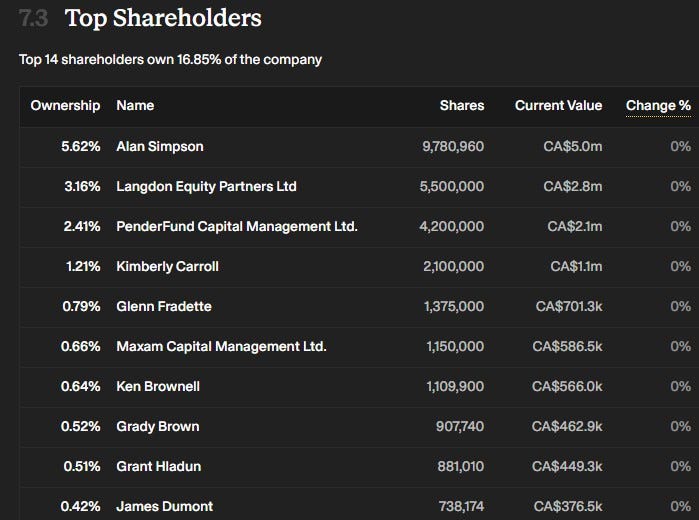

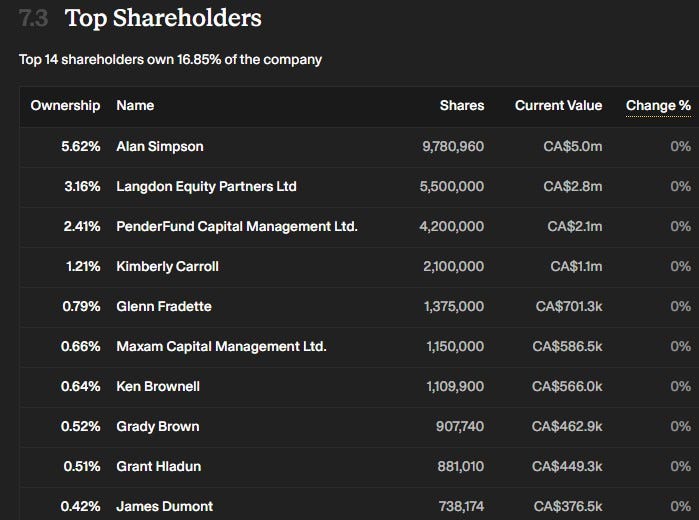

11% insider ownership with institutions making up 6%

No recent insider buying in the open market, but five different insiders did participate in the November raise for a total of over $1.5M

Income Statement:

Revenues came in at $7.2M, up 79% over a non comparable $4M a year ago due to new pharmacies added to the mix. Gross margins slipped by 170 basis points from 40.5% to 38.7%, and that drove an additional 72% gross profit dollars.

Operating expenses doubled to $2.8M, with cash burning expenses rising by a similar figure, both well above the rate of revenue and margin gains. While a portion of these expenses are from additional legal costs and fees stemming from their acquisitions, their G&A and payroll expenses are up about double as well, but they are not getting double the amount of revenue at the top. Something to monitor going forward.

After $205k in other income, mainly from interest received on their large cash position, PCRX delivered $127k of net income in the quarter, 50% less than the comparable period.

Summary:

Nothing earth shattering within these numbers, nor did I expect it. The company is trending towards a $30M run rate with their current six locations, and with seven new ones announced and another three under LOI, it looks quite likely they will triple their current pharmacy count to at least eighteen by the end of 2026.

While the majority of their growth is from new locations, they are growing organically. This is one of the things that attracted me most to Pharmacorp - their ability to quickly turn around well established pharmacies and integrate new merchandising strategies for the front of the store while also driving additional prescription revenue.

The risks with Pharmacorp are the same as when I first talked about the company in my 2026 Wolf Pick article. PCRX will have substantial growth for the foreseeable future, but it will come at the cost of dilutionary measures, or debt. You need to fully understand that, expect that it will occur and be ok with it.

I am, and I’ll be looking to add to my position above the 49 cent range as those opportunities happen. Three stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.