If you’re familiar with my work, then you are likely aware that PesoRama has not exactly been a favourite of mine. They received a one star review in my latest, and most recently identified them as a Danger Zone stock leading into these financials in my June What’s Wolf Watching piece on June 16th, telling investors to “save their Pesos”. The stock is down 18.5% since, and 34% in the past month.

Longer term investors have fared better as the stock is up 231% in the past year. The average daily volume increase has been very noticeable recently also, almost suspiciously since their April 23rd raise. That was done at 35 cents and yet the stock doubled from 40 to 80 cents in the next thirty days. Hard to explain.

Over the past year, PesoRama has expanded by about a dozen locations throughout Mexico. Post financials, the company has tried to clean up some of it’s debt problems which we’ll get into later.

So, should you continue to keep your pesos in your pocket when it comes to this Mexican dollar store chain? Let’s find out.

Balance Sheet:

As of April 30th, an important distinction given the post financials activity, PESO maintained a very unattractive current ratio and liquidity situation. The current ratio stood at .64 and consisted of $10.2M in cash, $10.8M worth of inventory and $2.8M in other short term assets against $37.1M in short term liabilities. Those liabilities included $19.8M of a revolving loan with Third Eye Capital which I wrote about extensively in my last review. Most recently this loan came with a 18.5% minimum interest rate, 15M warrants at 14 cents, closing fees, due diligence fees, and monitoring and standby fees. It was one of the worst loan situations I’ve ever reviewed. Only the only from VSBLTY with high interest rates from insiders tops it.

But as of a couple of weeks ago, the company closed a convertible debentures financing which raised just under $20M (net after $1.05M in commissions). These three year debentures carry an interest rate of 9% and will convert at 91 cents in mid June of 2029. Those funds were used to extinguish the Third Eye Blind debt.

So their balance sheet will certainly look better than it currently does in September when they report their Q2. Even with that $19.8M loan removed, liquidity is still concerning with their cash balance still about $7M shy of their accounts payable and lease costs for the next twelve months. This is of course after a $10M raise back in April.

If they’re operational cash flow positive, it would alleviate some of those concerns.

Cash Flow:

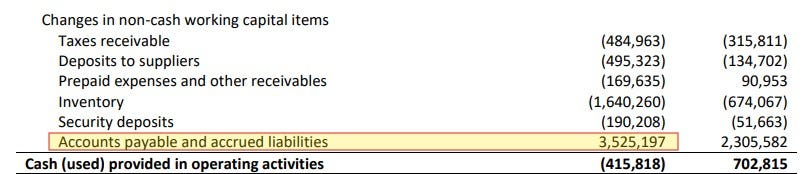

Alas they are not OCF positive, burning $415k in their first quarter. This compares with generating $700k of cash flow in the comparable quarter. Prior to working capital adjustments it’s about $500k worse, only looking as good as it is due to $3.5M in accounts payable growth during the quarter. We’ll touch on this again later.

During Q1 they spent $1.8M in investing activities - the majority of which was utilized on capex for leasehold improvements for new locations.

They received $10.3M into the treasury from the 35 cent raise and warrant exercises in the quarter, and made $950k of interest payments.

Overall, their cash position more than doubled during the quarter to $10.2M from the $4.85M they started with.

Share Capital:

202.4M shares outstanding. 18% dilution in Q1 alone and 111% dilution in the past twelve months

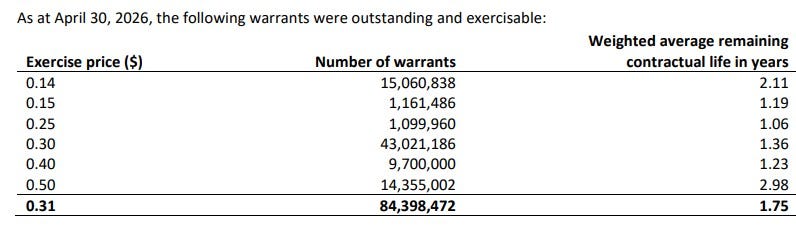

84.4M warrants outstanding - ALL ITM.

20M options - 13.5M ITM with another 2M at 55 cents (stock currently at 53)

$21M new convertible debentures post financials converting at 91 cents in June of 2029. (now publicly trading under PESO.DB)

3.5% insider ownership with a mix of insider buying and selling in the past twelve months

Fully diluted float just including ITM equities is 300.3M shares with an implied market cap of $159M

Income Statement:

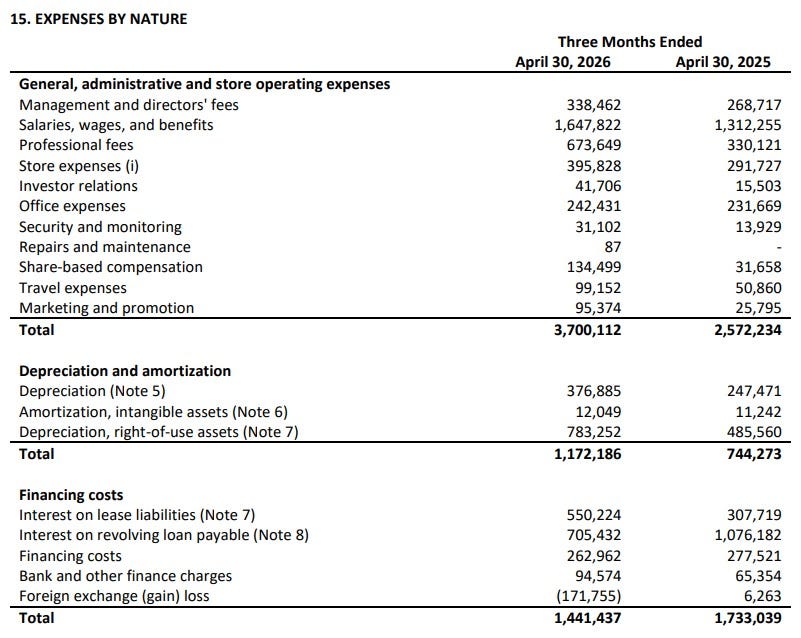

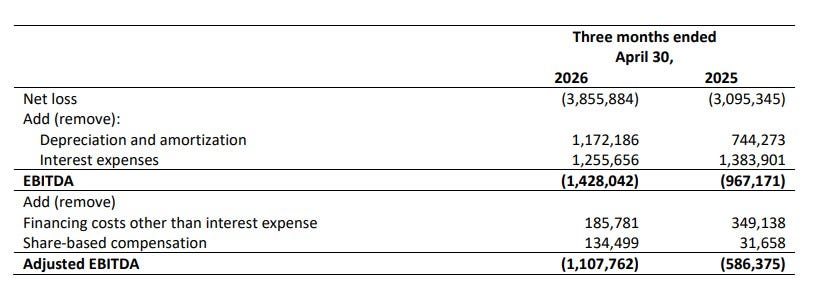

Revenue increased by 36% in Q1 to $7.5M compared with $5.5M last year. Gross margin declined by 240 basis points from 35.1% to 32.7%. Therefore on 36% more revenue, PESO generated just 27% more gross profit dollars.

Cash burning expenses jumped by 44%, more than both their revenue and gross profit increases. Non cash burning operating expenses (Depreciation and Amortization) increased by 58%. This is a bad combination resulting in their operating losses increasing by 76% ($2.41M vs $1.37M). Tack on $1.44M in financing costs and that takes their net losses to $3.86M vs $3.1M. Tack on another $455k in forex losses and their comprehensive losses increased to $4.31M vs $3.03M.

Summary:

Sell more, lose more is far from optimal and that is what we have here. Other than the revenue increase, almost every comparable metric was worse in Q1 of 2027 compared to last year. You cannot have the rate of your operating costs exceed that of your gross profit, and theirs was off significantly, and in most of their major spending buckets.

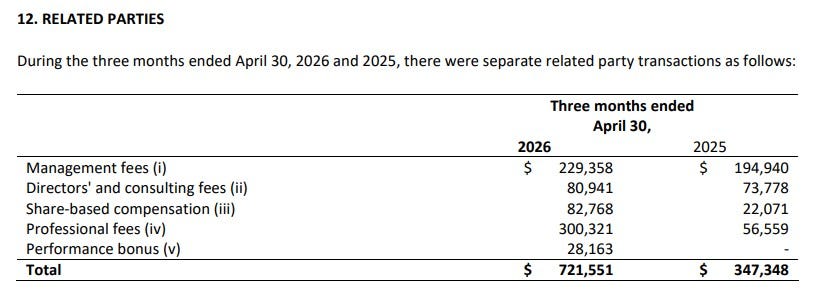

I also never like to see related party expenses rise like this, with the majority of the increase from using legal services with ties to one of their directors.

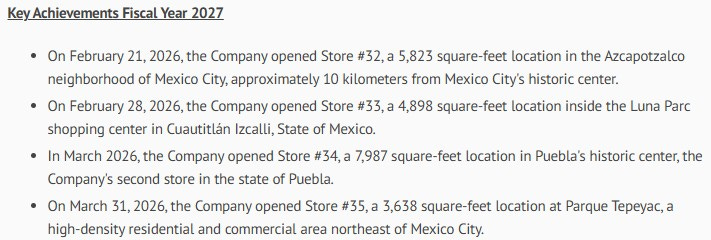

In fairness to PESO, they did not get a substantial revenue benefit from the four new locations in Q1. All four opened in the back half with the most recent opening on the final day in the quarter.

But by the same token, they ended Q1 of 2026 with 25 locations and had 31 open at the beginning of this years Q1. Even without those four new Q1 stores, this revenue figure might appear to be light. Adding to this potential theory is the company did not announce same store sales figures like they usually do. They reported traffic was up 19%, but no mention of SSS. This omission feels concerning.

The biggest positive to occur this calendar year was ridding themselves of that awful debt, but it was replaced with new debt at 9% over the next three years with further dilution tied to the end of the debentures term. Even when considering the post financial revisions to their balance sheet, their liquidity still looks poor. They are burning cash on a quarterly basis and spending capital on leasehold improvement for their new store openings. While we will get a better look in three months, right now it’s hard to imagine them lasting their 2027 fiscal year without the need to raise capital yet again or increase debt.

This is after 111% dilutive measures in the past year and 100M in ITM warrants and options set to explode this float even further.

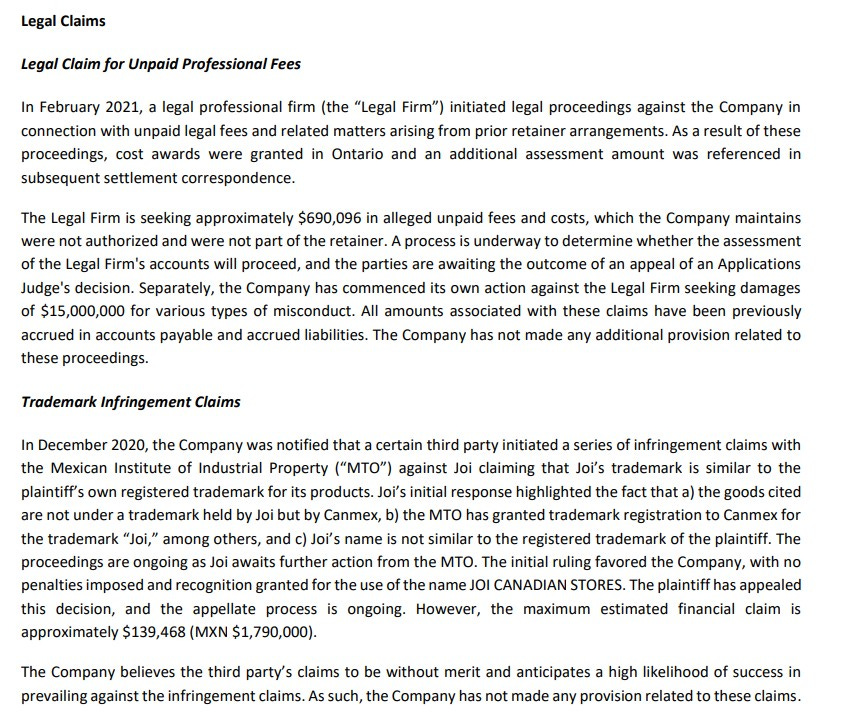

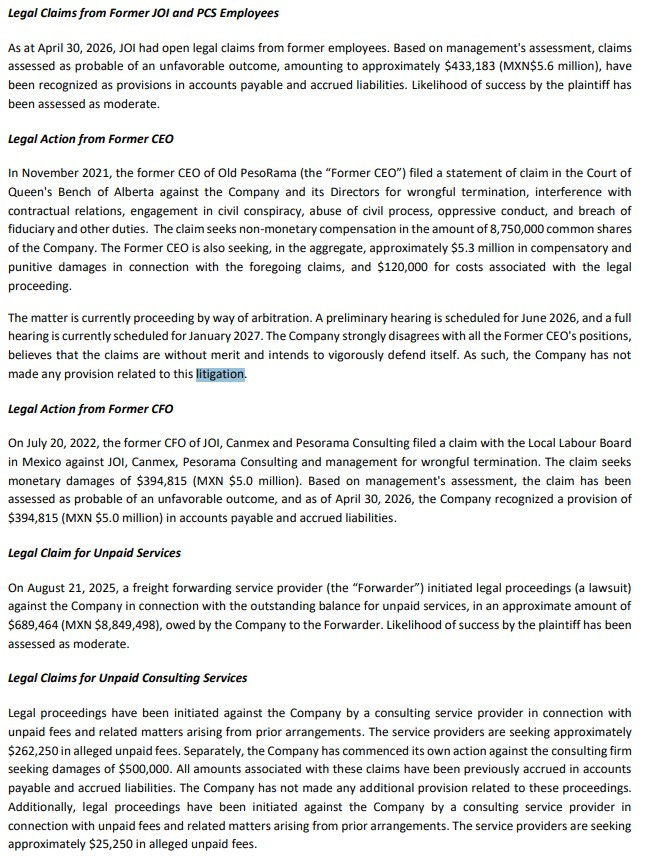

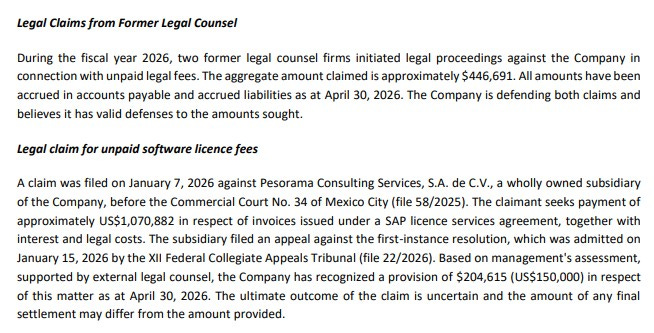

Another concerning portion of PesoRama’s financials is one I haven’t even discussed yet. Legal Claims.

Nine legal claims have been filed against PesoRama which spans nearly three pages within their most recent MD&A. While three of these claims date prior to July of 2022, the other six appear to be from the last twelve months. While legal claims do happen from time to time against public companies, SIX looks to be more than a coincidence.

Former staff, the former CEO and CFO, a freight provider, consultants, software provider, and even their former attorney have issued claims against the company. Many of these claims are for failure to make payments for services allegedly rendered. Remeber when I mentioned the significant growth in accounts payable? Are there any more shoes (or claims) to drop here? You have to wonder.

They have already recognized over $1M in provisions expecting to lose or partially lose some of these cases, but the final amounts could be much higher.

In short, PesoRama is one ugly baby. Speaking of short, it’s getting awfully tempting to play the other side at this valuation. PESO was under a $17M market cap one year ago. The implied market cap is nearly ten times that, with likely further dilutionary measures in the months ahead.

That’s 5.3 P/S while being very unprofitable on even the EBITDA and AEBITDA lines.

Ugly baby. Maintaining the one star while resisting the temptation for a downgrade.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.