I wouldn’t call it a love-hate relationship with Neupath over the past eighteen months, more of a like-meh one.

I first wrote about them in late 2024 with a decent three star take. I followed that up covering them briefly in my 2025 Wolf Picks as a potential bonus pick, stating that if they did “xy and z” correctly, the stock would be due for a re-rate. Most of that centered around obtaining some operating leverage, which required getting leaner on about a 19-20% margin rate which is not an easy ask.

They in fact achieved at least some of that, and the stock in fact did re-rate, currently up 130% from mid December 2024.

The story would have been that much better had I bought some shares myself at those lows.

Let’s find out where they stand after releasing their 2025 annuals yesterday as the market didn’t appear to be overly impressed with the stock finishing down 2 cents or 4%, dipping by another penny this morning.

(Free release to all subscribers scheduled for Friday Apr 3)

Balance Sheet:

We start with a mediocre but acceptable current ratio just shy of 1.1 consisting of $4.5M in cash, $8.7M in receivables and $750k in other short term assets over top of $12.8M in liabilities due through 2026. While a sub 1.1 ratio isn’t anything to write home about it, it is a significant improvement from where they stood twelve months ago when it was 0.72.

While receivables make up 62% of their current assets, they remain relatively low risk mainly stemming from government agencies.

Neupath has $6.2M of debt with the National Bank of Canada of a total of $13.5M available through a term loan, acquisition line and revolving facility. All amounts outstnading are under the term loan at prime + 1%. This agreement with NBoC was entered into in March to replace existing loans with RBC, and to settle a related party loan and early redemption of debentures.

Cash Flow:

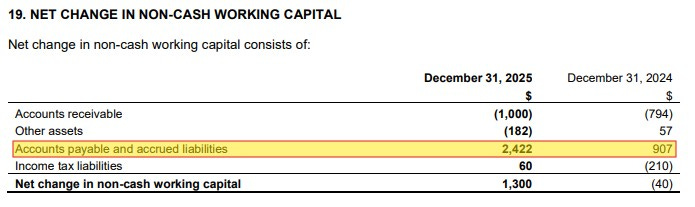

Neupath delivered $4M of operational cash flow in 2025, up 53% from last year. Much of that variance is from working capital changes, particularly growth within their accounts payables. The OCF increase is therefore somewhat of a mirage as the increase YoY is not as good as it looks.

Within the rest of the statement, NPTH invested $863k in investments and intangibles, shuffled around their debt as mentioned in the previous section, taking on a net of $300k more and also repurchased $231k in stock.

Overall, they improved their cash position by 53% during their fiscal 2025.

Share Capital:

56.3M shares outstanding, 80k shares less than a year ago

Repurchased 1.04M shares under their NCIB with 50k additional shares bought back post financials

5.1M options - all but 124k are ITM but none of those expire for 2.5+ years

769k RSU’s with 435k granted in 2025

31% owned between insiders and institutions (per investor deck)

300k shares were purchased by insiders in November at around 35 cents

Income Statement:

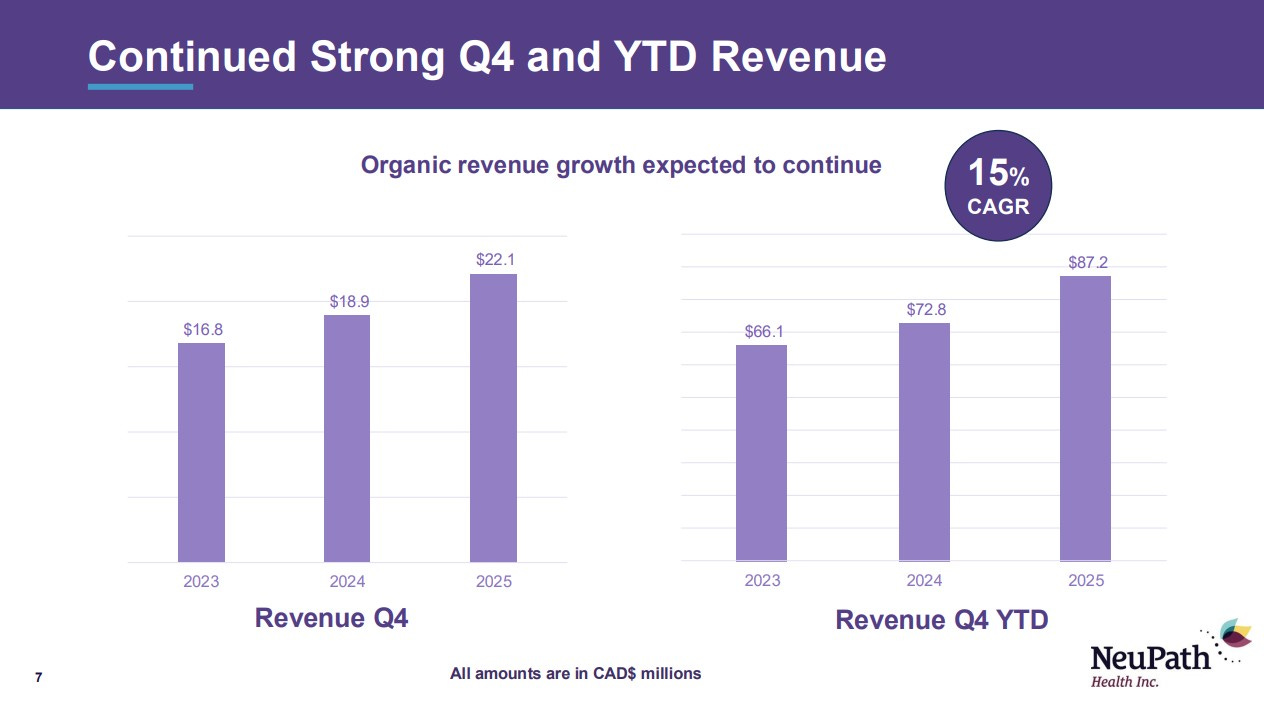

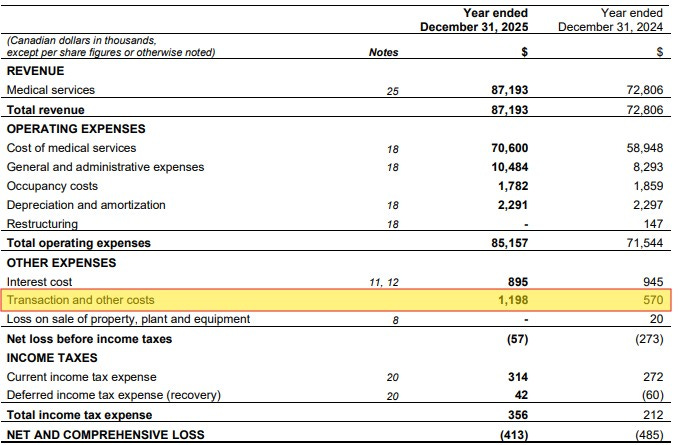

Revenue in 2025 remained strong in 2025 with $87.2M, a 20% increase over what they achieved in 2024, continuing on their 15% CAGR path.

While the company does not calculate a traditional margin line their COMS (Cost of Medical Services) is comparable enough for analytic purposes. This gross margin improved by 40 basis points to 19.4% YoY.

While occupancy costs decreased as expected (5%), unfortunately their largest controllable expenses (G&A) rose by 26% and at a significantly higher rate than their total revenues.

Operating income (another line not shown on their P&L) did grow by 61% to $2.04M, despite that extra spending.

The refinancing of their debt did reduce their interest costs slightly but “Transactions and other costs” rose by over $600k or 110%. Much of that was in relation to costs of that refinancing and should be viewed as a one time expense although the company does not state how much.

Total net losses were $413k, slightly improving over last years loss of $485k.

If we parse out just the quarter, it’s not quite as good and that perhaps partially explains the markets rather muted reaction yesterday. While revenues continued to be strong at 17.3% above the comparable quarter, net losses increased from $180k to $324k. A big part of this was their G&A costs rose by 31.9% on those 17% additional revenues.

Overall:

On the surface it appears to be a bit of a mixed bag with revenues performing extremely well, but they did not get much in terms of operational leverage therefore not translating to much improvement on the bottom line.

But did they perform better than it would initially appear?

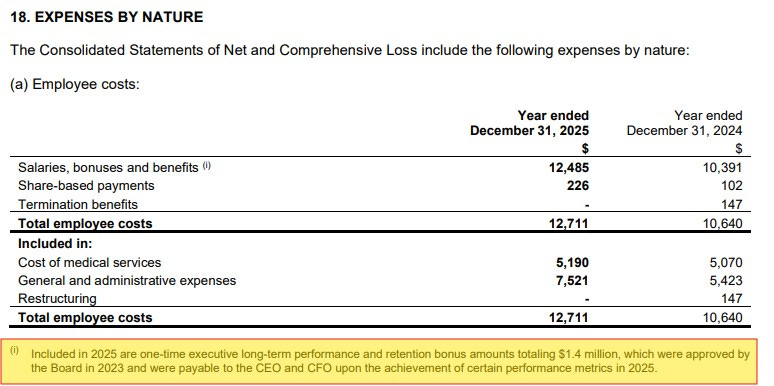

Neupath had $1.4M in one-time bonuses paid out which were approved in 2023 for retention and performance. With those amounts excluded, their annual G&A costs rose by 9.5% on that 20% revenue increase and that looks like much better operational leverage than the total P&L would indicate.

In the company’s investor webinar yesterday, they stated revenue guidance of between 8-12% for 2026. What is important to note however is that growth is excluding a one time revenue item that occurred in Q2 of 2025. No dollar figure was ever provided for that but based on what the company has said I estimate that as somewhere around $2M.

Given that, let’s assume their 2025 revenue baseline as $85M rather than the $87.2M as reported, and that would put their 2026 revenue guidance between $92-$95M.

Neupath’s current valuation is at a $25M market cap, which drives a .27x P/S (2026) and under 8 EV/EBITDA with decent looking EBITDA to cash flow conversion.

With $1.4M in 2025 bonuses and perhaps as much as $600k in transaction and legal costs added back to normalize their Net Income, that could have driven as much as $1.6M of net income on a normalized basis.

I feel investors are focusing less on that and more on what they may consider to be conservative guidance, although the mid-point would still put them into the double digits in 2026. They are also continually looking at M&A opportunities and the additional flexibility they have with their new banking relationship allows them to do so. I’m also quite impressed with the new incoming CEO who seems really focused on efficiencies and getting more operational leverage out of the business. He was also one of the two insiders buying on the open market in November

To assist in improving your due diligence, I’ve attached the following.

Updated Investor Deck

Latest interview with Radius Research

Transcript of yesterday’s investor update (video not yet available)

In my 2025 Wolf Bonus picks, I said if they can prove they can get to $100M in revenue and $5M in Net Income, they would get a significant re-rate. The $100M revenue is well in sight and could happen in 2026 with slightly overperforming their guidance. That net income figure looks a little further away, but I do like the initiatives they have in place to get them closer.

Upgrading to 3.25 stars. I also opened a starter position.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.