This review comes via request through the Wolf Den discord. These financials are about six weeks old so this isn’t typically a request I would agree to. Then I looked at the chart.

A year ago the stock traded at $0.115. Just two weeks ago at the end of March, it was trading at the exact same figure. But since the beginning of the month, the stock has more than tripled, up 217%. For a stock that went many days throughout 2026 with no shares exchanging hands, suddenly had significant volume.

Nepra released their financials mid-day on Feb 27th. For the entire next month, 282k shares were traded. In the past two weeks during this 3x rip, 3.6M shares. The company had zero press releases between their Q3 financials press release and preliminary Q4 numbers on April 10th. So why did the volume and price action begin ten days earlier. Feels a little suspicious right?

Let’s see what we can find. I have yet to open these financials, so you’ll be getting my “live” reaction as you read along.

Balance Sheet:

Insert cringe emoji here. At a minimum, you would like to see a current ratio above one where current assets at least offset their current liabilities. Nepra Foods ended Q3 with a ratio of .33. That consisted of just $25k in cash, $527k of accounts receivable, $1.07M worth of inventory and about $100k in other current assets overtop of $5.3M of liability commitments due over the next twelve months.

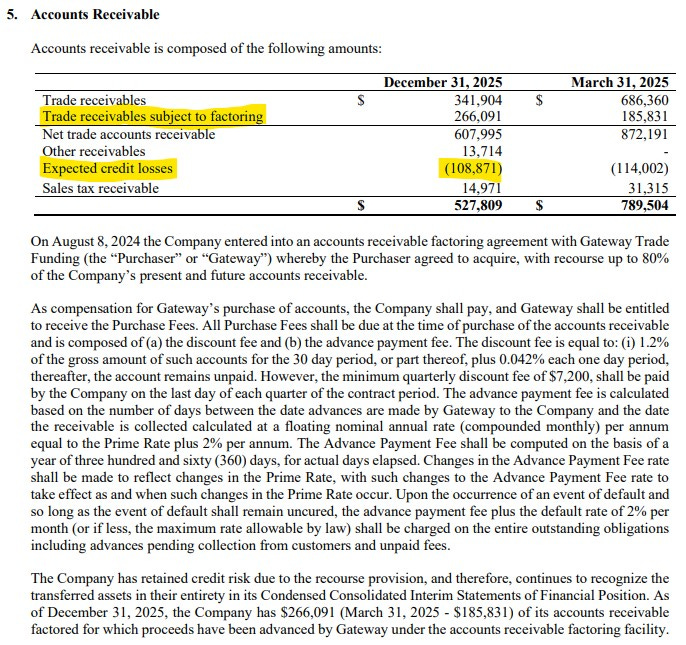

It didn’t take very long to get to our first red flag. Receivables.

First issue is anticipated credit losses. $108k doesn’t sound like a big figure but it makes up 18% of their total. We are less than two years removed from the company taking $211k in recorded losses ($76k was recovered last year).

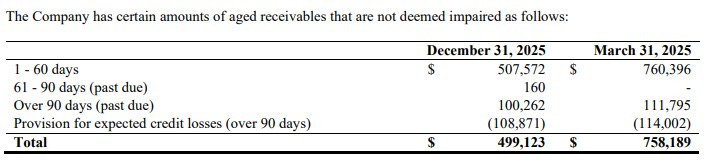

Given the details in their aging report, one would assume their credit terms are 60 days, and are not expecting to receive payment for amounts past due.

Then we come upon something that I’ve only seen once in the last six years of performing financial reviews - a company entering into a factoring arrangement for their receivables. Companies enter into these agreements when facing liquidity challenges, and with under $25k in cash on the books and a .33 current ratio that highly qualifies. In a nutshell, Gateway Funding advances cash for their receivables in exchange for interest and fees, but Nepra Foods still maintains the risk if those receivables are not eventually paid. This poses a myriad of problems:

It’s expensive. For example lets use a $100k invoice that takes 60 days to receive payment. Gateway would give (lend) Nepra $77,600 (80% of the $100k less the 2.4% fee). When the customer pays in 60 days, they would get the additional $20k less interest and additional fees. The total cost of that borrowing is approximately 3.6% for 60 days, annualized between 21-23%. For customers taking longer than 60 days would get significantly more expensive as the discount fee escalates as well as an additional .04% added per day.

They maintain all the credit risk while paying this significant premium. Should the customer default on payments, they still have to pay Gateway back.

This effectively inflates that already poor current ratio. That $266k in receivables under “factoring” needs to be shown in current assets even though funds are already received due to IFRS accounting rules. Therefore that .33 ratio is more like .29.

Nepra Foods has just shy of $2.5M worth of debt. It doesn’t sound like a high dollar amount but their note 12 which covers this in their financial statements covers nearly seven pages and ten different debt instruments. Post financials there was additional activity. Most of the outstanding debt is owed to related parties.

(We have reached the stage where I regret starting this review)

$1.14M of debt owned by the COO and CFO was amended post financials to be paid in a lump sum prior to the end of 2027 at 6%.

$669k in a loan owned by the CEO by way of a promissory note was settled post financials on Feb 11th via stock at 10 cents per share. A little more than a month later those shares are worth over $2.5M.

What a mess. Let’s move on.

Cash Flow:

On a more positive note, Nepra is a little better than cash flow neutral YTD generating $57k of operational cash flow, and that compares to burning nearly $1M at this stage last year.

Nepra had zero investing activities so far this fiscal year, but has reduced their net debt by $700k and received $929k via various financing activities, the majority of which through a private placement that took 4 months to close over three tranches at 8.2 cents CAD. Investors in that PP have nearly 4.5x’d their money since.

Their $25k cash on hand is 44% less than what they began the year with ($44,700).

Share Capital:

As of Dec 31, 113.6M shares outstanding representing 9% dilution YTD but 46% over two years

1.4M options outstanding none expiring before 2031. Only the 500k granted this year are ITM at 13 cents

22M warrants outstanding, all ITM ranging from $0.10 to $0.17. Post financials 5.2M at ten cents were exercised with 8.5M expiring unexercised. Ouch, those 8.5M warrants could have resulted in $2.25M worth of profit at today’s share price

Insider ownership is a moving target. Yahoo Finance has it at 43%. It’s likely higher with the CEO Billy Hogan owning 33% after the shares for debt transaction mentioned earlier after financials

No insider activity on the open market

Current float at approx 125.5M representing 20% dilution YoY and 61% over two years

Income Statement

Revenue in 2025 has been quite good, coming in just shy of $6M on a YTD basis representing a 50% increase over last year. Margins came in at 31%, a substantial 800 basis points above last years 23%, therefore gross profit dollars more than doubled against 2024 through three quarters.

Total expenses are also down, and significantly by 18% with savings across their two major spending buckets. G&A costs are down 18% with payroll down 19%.

Even with that Wolf Trifecta (double digit revenue, margin improvement and operational leverage achieved) they still lost $353k on the operating income line, and tack on $623k of finance costs (30% higher than LY) on a relatively small amount of debt results in a net income loss of $1.04M, a $300k improvement over 2024.

The third quarter itself had a 54% increase in revenue to $2.23M. Margins were up by 110 basis points to 28.5% and operational spending was 10% less. Nepra delivered $85k in net profit in Q3, but that is mainly due to a $424k gain in change in fair value of their warrants. Without this, they would have had a net loss of $340k compared to $560k last year. Now that the share price has appreciated so much this will turn into a much larger loss for warrants still outstanding.

Overall:

Using the updated share count, Nepra has an approximate market cap of around $46M. That feels outrageous for a company who has done $8.3M in TTM revenue with negative TTM EBITDA and treading water from an operational cash flow perspective.

That is all before taking into consideration the horrible state of their balance sheet, which to be kind is a mess with serious liquidity issues.

I went through their investor deck, and attached it below for your perusal. WTF kind of pose is the Chairman of the Board doing here? The guy sporting the tee shirt is Co-Founder, former CEO, and now Chief Visionary Officer, CTO and Master Baker.

To be honest all I had to see is this one slide to know I’d never invest in them. Chief Visionary Officer and Master Baker. You might as well just add Douche Canoe to the list of titles.

I’ll also attach a recent brief interview they did with Stock Box Media. They appear to have most of their content around mining shitco’s, which would explain why I’ve never heard of them.

I'll be honest, the P&L really doesn’t look so bad. Revenue growth is quite impressive, and they are doing so with improved margins. The problem is much of the impact in those margins is being eaten up by the way they are handling receivables. If you sell customers something at 31 points of margin, and then enter into a factoring scheme for advancement of those funds which come with a hefty VIG, you erase all and more of that margin improvement.

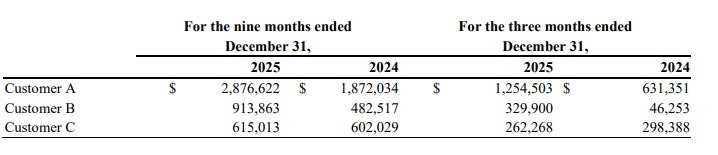

They also have customer concentration issues - 85% of their Q3 business came from three customers. When we go back to their A/R aging report, there is a strong statistical likelihood that one of their top three customers doesn’t like paying their bills on time - or maybe at all.

The market cap for what they are achieving is just highly overvalued in my opinion. This two week stretch of share price appreciation looks very unusual and I don’t trust it. This stock barely has a mention in social media and bulletin board circles and there were no worthy news items from April 1-10th. That April 10th NR cited preliminary revenue numbers showing a 15% revenue increase YoY. That is typically quite good, but also the worst revenue improvement they achieved in the last seven quarters.

Interestingly enough, the stock is down 20% today since I began this review. IDK but my pump/raise radar is off the charts with this one.

Two stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Douche canoe ... I had a good laugh :)

Never heard of this douche canoe before. Thanks for the introduction, Wolf!