The first MOAR was so popular, why not do another?

Wednesday and Thursday of last week had quite a few smallcaps that I usually cover release their financials. I made a last minute decision on Tuesday to drive six hours to see the Canadiens/Hurricanes game, only to see le Bleu-Blanc et Rouge suffer the type of abuse usually reserved for red-headed stepchildren (sorry gingers).

I absolutely “wolfed” down a giant smoked meat sandwich which was a near sexual experience, so I do apologize to any patrons who were within viewing distance of that display. We also brought home some bagels so the journey wasn’t a total loss.

I missed a lot during the 36 hour trek, so let’s catch up. Three of these four stocks declined on earnings, two of which I warned you about in May’s WWW - What’s Wolf Watching article.

ZoomD Technologies was listed as a Danger Zone stock in back to back WWW articles, dropping 37% on their Q4 earnings, 16% on their recent Q1 for a total of 49% since April 29th. The “momentum” has officially ceased continuing.

They were put in the second Danger Zone after their Q4 experienced a 51% drop in revenue with 93% less net income. In Q1 they faced the daunting task of tougher comps, and with the knowledge of little to no progress on their two largest customers, the writing was clearly on the wall for a disastrous quarter. Anyone telling you differently (some indeed were) simply was just not paying attention.

I did not think it was possible for the company to come up short of my lowly expectations, but that is indeed what occurred in Q1. Not only were they down year over year by 64%, but down sequentially by 9% too. They lost $640k on the bottom line which was their first net loss in the last nine quarters. After their Q3 of 2025, they had generated $24.7M of TTM net income and they have now lost $350k in their last six months.

The one positive to come of of the quarter despite everything, was they produced nearly $900k of operational cash flow. That is of course down 83% from the comparable period, but at least they are not burning cash.

The company may have softened the blow, or at least attempted to by announcing an NCIB for up to 10% of buybacks the day before they dropped these vomit inducing financials. Investors have been clamoring for this for sometime, and the $31M sitting in cash supports such a move. I’m on record as saying that an NCIB would not occur until positive news happened with their two largest customers. I guess now we wait to see how quickly they action it.

With these poor results largely known (again at least to knowledgeable investors), the biggest information to come from these results was going to be the commentary on the call. More specifically, WTF is happening with their two largest customers (Shien and insert your best guess for #2)?

I’m not sure the transcript provides a lot of encouragement, nor clarity. It sounds, at least to me, a strikingly similar message that investors heard during the last two quarters. The sequential decline QoQ further supports this.

Even without these top two customers coming back fully on board, customer concentration of their top five customers remains high. It was 85% at this time last year, but their top five (with last years top two removed) still remains at 66%. As much as we have heard about customer diversification and growth outside the top two, $6.3M of their $9.5M came from their new top five without Shien and last years #2. If you were thinking at these price levels that customer concentration was risk off, I’m not so sure it is. Who’s the new number 1 customer and how much of that 66% do they make up? What if they decide to implement changes to THEIR operating models and KPI’s? Or tweak their software? What then? I think these are fair questions to ask.

In the past two years ZoomD has done an incredible job gaining operational leverage, which I’ve discussed many times. In my five years of performing reviews, they may be the best I’ve seen. But that isn’t what the below portion of the conference call sounds like. This sounds like preparedness for future softness on the top line. Limited visibility is starting to sound like a breakdown in the relationship. We’re talking six plus months here. It feels like someone is getting dicked around. Is it ZOMD, or is it us retail investors?

Of course it’s not all doom and gloom for Zoom. They have over $30M in cash and a current ratio over 4.6. Even while having two disastrous top line quarters, they still remain operationally cash flow positive and are one of the most operationally prudent company’s on the Venture.

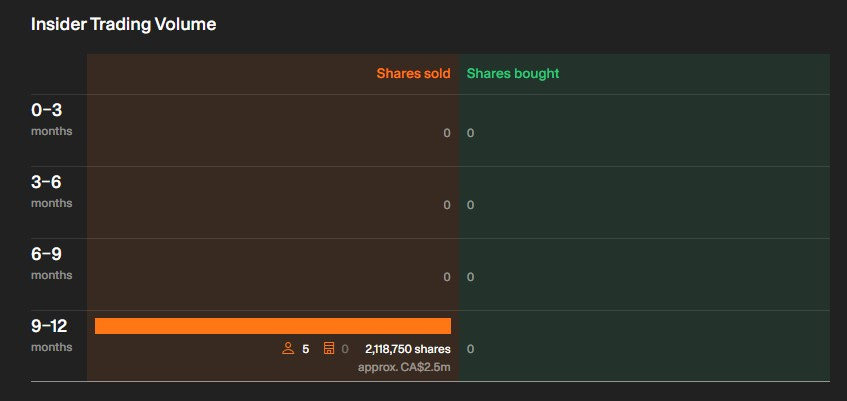

They have instituted a buy back program, so we will see how aggressive they are over the next couple of months. I’d much rather see insider buying which has not occurred in the entire slide from $2.75 to under 50 cents. I do know what they did last summer, and that is to take lots of profit off the table. If they ain’t buyin, I ain’t buyin.

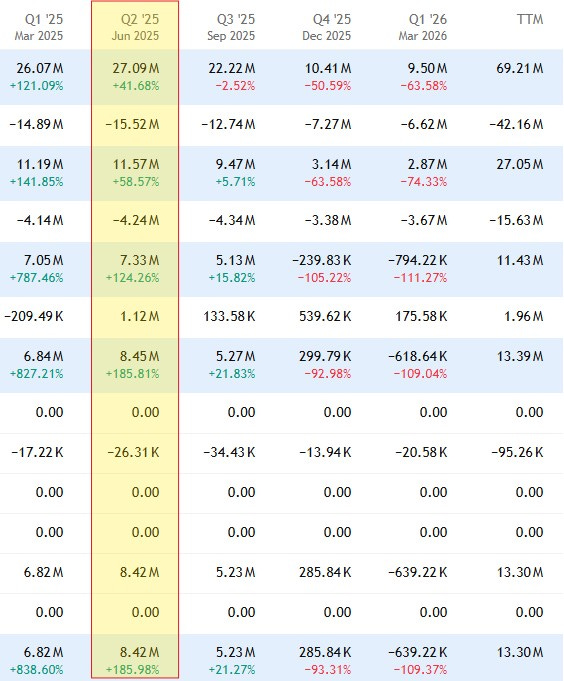

Stocks don’t trade on a strong balance sheet or high cash balance. They typically trade on meaningful progress. In the last six months, revenue is down 58% and went from $11M of net income to a $400k net loss. The bad news is the comps get even tougher in Q2 which we will see at the end of August. They are up against their highest revenue ($27.1M) and highest net income ($8.4M) quarter in their history.

I still see things getting worse here before they get better.

NTG Clarity is another stock that was put into back to back Danger Zone’s in my April and May WWW articles. They are down 28% from my April piece and are down 8% since last week’s earnings, decreasing by as much as 14% post Q1.

Unlike ZOMD, they are not hemorrhaging on the top line - in fact they were up 7.5% over the comparable quarter. But they were off by 11% sequentially, a seasonal impact we did not see at this time last year when they grew by 14%. Backlog also fell by $15M or 17% since the end of Q4.

NCI has a host of other issues, but in my view two major ones. The first is their investments in people during 2025 has not paid dividends, partially causing a 100 basis point reduction in gross margin, but more concerning is the 88% increase in G&A spend over the comparable quarter. A 7.5% increase in revenues while receiving lower margin with 88% more operational spending is a terrible combination. As a result, net income was down by more than 50%. But the pure comparable numbers are actually worse than that. They received a $1.6M birdie in income taxes compared to last year and a $260k birdie in forex. Prior to income taxes, net income was $134k vs $3.18M, plummeting by 96%. On an AEBITDA basis (a terrible metric to begin with) they came in at 4% vs their annual guidance of 13-16%.

The good news on that front is despite the above weakness the company did not back off their annual guidance. The company did face some holiday challenges and the current Middle East situation is not doing the company any favours. But let’s remember the annual guidance was pretty soft in most retail investors eyes and they have come out of the gate extremely slowly in Q1.

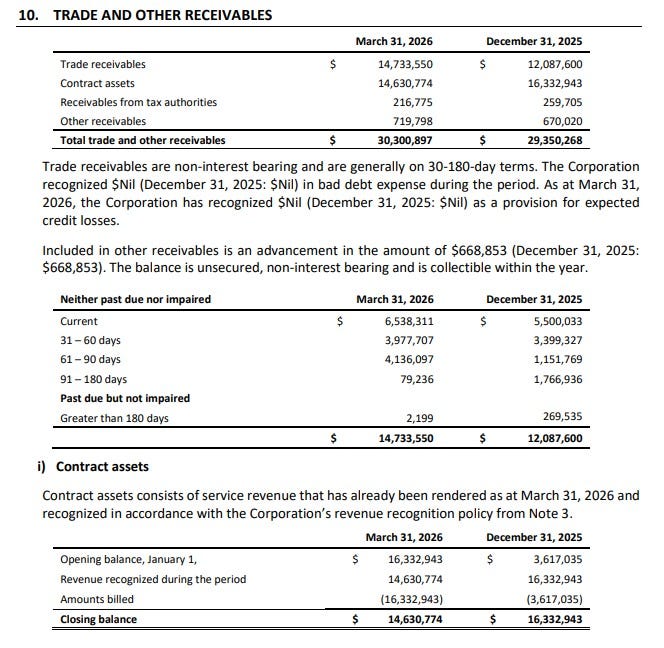

NTG’s biggest problem remains their cash generation, or lack thereof. They broke even from an operational cash flow standpoint in Q1, but still have burned $3.2M on a TTM basis.

While their current ratio is strong at over 3.1, their liquidity remains highly questionable with their A/R accounting for 78% of their current assets and current cash position not covering their one year liability commitments. If this were a one quarter glimpse, investors would be able to shrug it off. But it is far from that and in my view a systemic problem. Last month I said I felt their announced initiatives surrounding cash flow improvement were not enough and could in fact make things worse through delayed billings and offering extended terms and early payment discounts to top customers.

In Q1, early indications are I was accurate in that assessment as receivables grew by $1M and their aging report worsened.

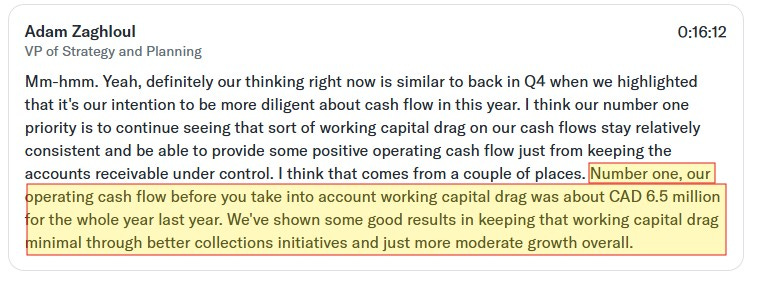

Perhaps the most troubling part of this is statements like below. Calling it “working capital drag” minimizes what their biggest problem is, and no, they have not shown good results as Adam claims.

In the past two years the company delivered $15M in net income and created zero operational cash flow generation. What they did do in the last two years is raise $14M of capital through dilutive measures during that time. Investors participating in the 2024 raise are down by 45%, and those who participated in 2025 are down 65%. When I see statements like I highlighted below it angers me, as it implies that Adam thinks his investors are stupid.

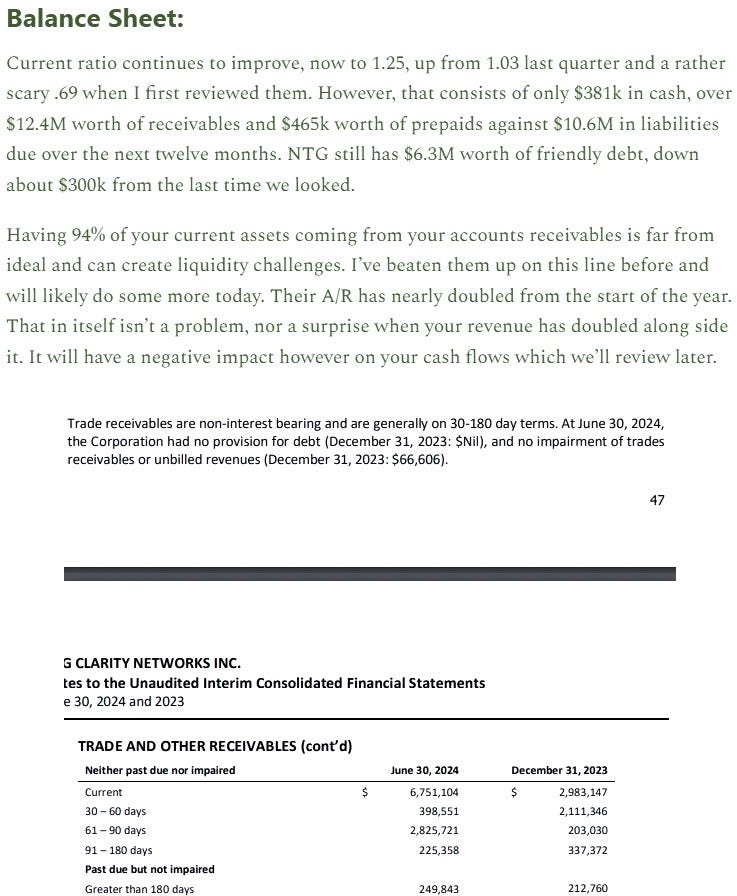

Harsh? Absolutely, but I don’t feel its without merit. A current or former Wolf Pick is always going to generate more scrutiny. Below is what I said about their balance sheet and receivables TWO YEARS ago and even then it wasn’t the first time I raised these concerns.

Are they a better company than two and a half years ago when they were a 2024 Wolf Pick? Yes. But there are many reasons why they are not as attractive a company as they were at the end of 2024 when they produced $10M of net income on $56M in revenue. TTM revenue may be up by over 50%, but net income has declined by 57%.

2026 growth is now expected to be in the single digits and they are spending nearly double on operating expenses. We are not yet seeing the improved gross margins we were told would happen with the expansion of things like NTG apps, and the all important profitability to cash conversion is one of the worst you will find on the Venture.

I’m more than ready to give them credit when any of that changes, but until they do, I’m just watching.

For further reading I’ve attached Atrium Research’s report update to the image below. Note the downward revisions in their estimates below the revenue line. I think their profitability estimates are still too high.

This one will not be nearly as long as the last two.

Kraken Robotics has tripled in value over the past year and they are a twelve bagger since their 2024 Wolf Pick selection at $0.61, achieving as high as 17x from their 52 week high of $10.74 in March.

The stock is down by 11% since they released their earnings last week however.

Kraken hasn’t traded on traditional fundamentals for a long time and I don’t expect that to change anytime soon. It has traded on a cyclically strong sector, some “goonery” and pump on the OTC side, and most recently an extremely large acquisition.

It’s a good thing for PNG that they do not trade on traditional multiples or fundamentals as their Q1 results were quite poor. Outside of a 35% revenue increase, margins decreased by nearly 600 basis points and operating costs rose by 64%. This caused them to go from $519k of net income last year to nearly a $4M loss this year, and they did so while burning $4.7M of cash vs generating $3.1M last year.

Therefore I’m not about to make an argument in favour of their current $2.3B market cap.

Their $615M acquisition of Covelya is expected to close sometime in June, therefore their Q2 will be about as meaningless as these latest financials. The more important financials will be in Q3 when they report amalgamated numbers, as well as updated guidance from the newly combined entity.

Until the end of Q3 expect to see continued volatility making it attractive to swing traders. I will continue to hold the 20-25% of my initial cheap shares.

Emerge bucked the trend, at least of the stocks covered in this article, as they leaped by 18% on the release of their earnings.

I bought some ECOM at the end of last summer, added on a dip and sold for a near 100% profit in December. I also retook a position within the Buy Zone listed above from my April WWW article that has yet to bear the same fruit the second time around.

No offense to Emerge, but while journeying back and forth to Montreal last week, they were lower on my priority list. So when I witnessed the 18% bounce on earnings I assumed they would be excellent. But upon further review, I have some questions.

In my Q3 review I cited balance sheet concerns with both their current and quick ratio’s. Those have worsened in the past two quarters with a current ratio of .84 (deferred’s removed) and increasing liquidity concerns with a quick ratio of just .48, as their cash plus receivables total less than half of their one year liability commitments. Even if the $1.2M in convertible debt goes to equity their cash plus A/R still falls about $4.4M short of their twelve month needs. Note this all takes place AFTER the company renegotiated their debt moving it from current to long term liabilities.

They can of course make that up with positive operational cash flow but they burned over $300k operationally during Q1. On the positive side that is half of their burn rate from last year but it does not put a dent in their near term liquidity needs.

On the P&L revenues improved to $5.9M, up 17% from the comparable period with gross margin slipping by nearly 400 basis points from 38.6% to 34.8%. Expenses converted modestly well with 4% additional spending with big savings in Marketing (30%) but offset by much higher SG&A which was up by 15%.

After experiencing 44% higher finance costs on their debt and a $330k bogey to LY in foreign exchange, Emerge suffered a $125k loss compared to a $400k gain.

Based on everything above, the bounce following their earnings I do find somewhat surprising.

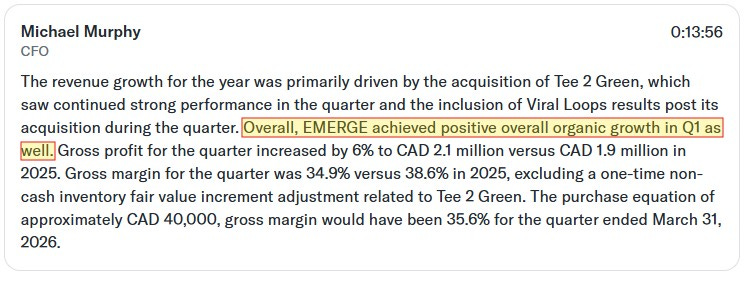

The new CFO stated in the call that organic growth was up.

But that doesn’t totally jive with their segmented breakdown which shows declines in both E-commerce segments. Perhaps this is to do with backing out the $405k in other revenue from last year which is non-comparable. Total revenue grew by $879k, and their retail revenue from T2G of $1.33M was not completed until Q2 of last year, therefore I’m showing their organic number shy by $46k YoY.

Next quarter both their E-commerce and retail revenue from T2G will be essentially apples to apples. They will have a new stream of revenue for almost a full quarter for Viral Loops. They did a little over $100k/month in 2025 so the numbers will be small, but are expected to be profitable, cash flow positive and present some potential synergies with taking some marketing costs out of their e-commerce business. The next two quarters are also very big for the golf industry so the organic growth of T2G in their first comparable quarter will be key to watch.

The balance sheet may be just as important to watch going back to their weak liquidity situation. Their $8.15M of payables are all due within the next twelve months in addition to minor debt and lease payments. Their current cash & A/R leaves over a $4M shortfall and $4M of operational cash flow in the next twelve months seems very unachievable. I fully suspect a raise is on the table. This comes after raising $2.6M (net) for the Viral Loops acquisition which had an initial outlay of $2.1M, with $200k additional next March.

Overall, I feel Emerge is priced pretty appropriately here at a $17M market cap being slightly unprofitable on the net income line with a 28 EV/EBITDA ratio and a very real risk of a near to medium term raise. Q2 does present a big opportunity with the Viral Loops synergies and organic growth potential of T2G. Probably a three star performance at best.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.