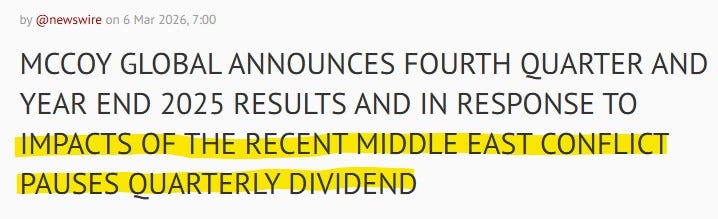

That sound you heard last night was the weeping from McCoy Global shareholders after the stock dropped by over 18% in yesterday’s trading. The company released their Q4 and annuals for 2025 pre-market. I was among those with teary eyes.

One year ago, after their 2024 annual earnings release, I selected McCoy Global as a mid year Seal of Approval pick at $2.39. Four months later the stock had appreciated by 85%. After yesterday’s ass whooping, those gains had eroded to only up 12%.

In my February WWW earnings preview article, I put MCB in a danger zone, suggesting it would be a bad time to pick up shares prior to their earnings release. While that turned out to be true, I had the reasons all wrong.

Let’s get into the financials. Does the thesis from last year still hold up?

(Note: will be available in full to free subscribers on Thursday March 12th)

Balance Sheet:

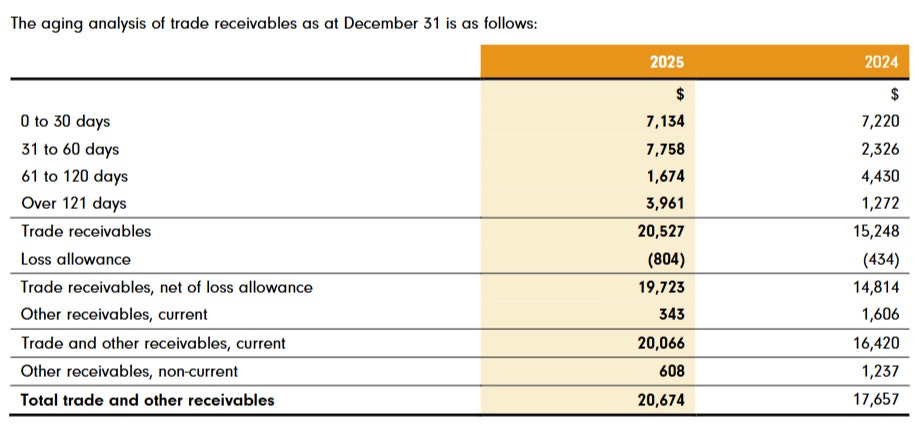

While McCoy has an overall solid balance sheet, their near term liquidity could look a lot better. They do sport an excellent current ratio of 3.1 consisting of $3M in cash, $20M in receivables, $43.7M worth of inventory and $1.6M in other short term assets against $22.1M in short term liabilities due within their 2026 fiscal year.

That current ratio is up from 2.6 a year ago but at the same time their liquidity has weakened due to their cash position of just $3M, and their inventory position going from 53% to 64% of current assets.

Their Cash and A/R does offset their one year cash commitments, but the receivables aren’t looking so hot with bills over 121 days approaching 20% (8% last year), and a near doubling of allowances for doubtful accounts.

The company does have a $5M credit facility available to them and if those receivables don’t come in ASAP, they could have to tap into it.

Cash Flow:

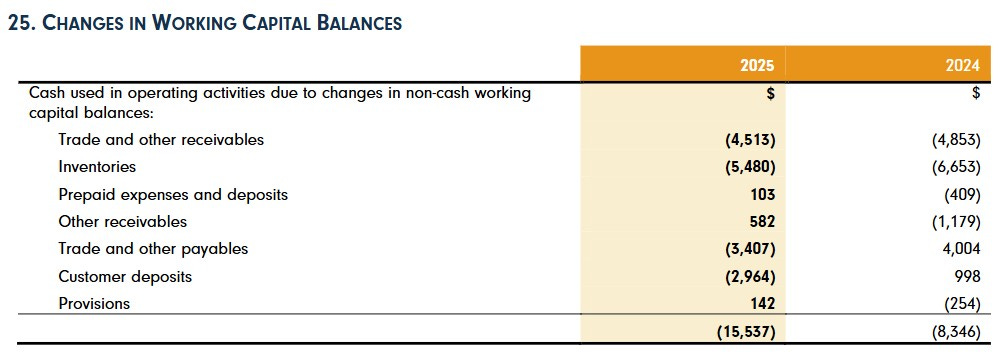

Due to significant working capital adjustments, operational cash flow looks like a dog’s breakfast, showing an overall cash burn of $1.7M during 2025 compared to generating $6.5M of positive cash flow a year ago.

This is what happens when you pay your bills on time but your customers don’t return the favour. Couple that with additional investments in inventory and the end result is operational cash burn.

During 2025, the company also invested $6.8M in capex, borrowed but repaid all of their $5.3M debt, repurchased $1.4M worth of stock and paid out over $2.5M worth of dividends.

All of that combines for an 82% reduction in their cash position from the start of the year.

Share Capital:

McCoy has managed their float extremely well - 26.8M shares outstanding which is less than the number from two years ago with their buybacks more than covering options and RSU’s

519k shares repurchased at an avg price of $2.67

2M options outstanding, a little more than half ITM but none expiring for three years

Approx 1M in DSU’s, DPSU’s, RSP’s and PSU’s

Overall SBC costs in 2025 were $783k, 55% less than 2024, $1.73M

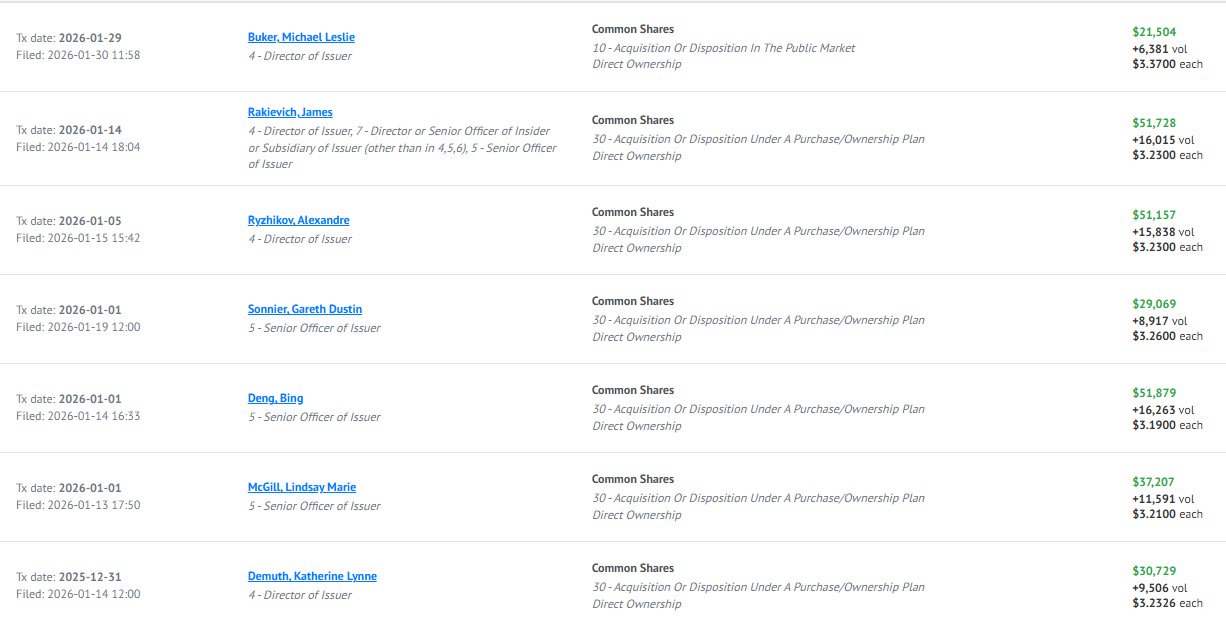

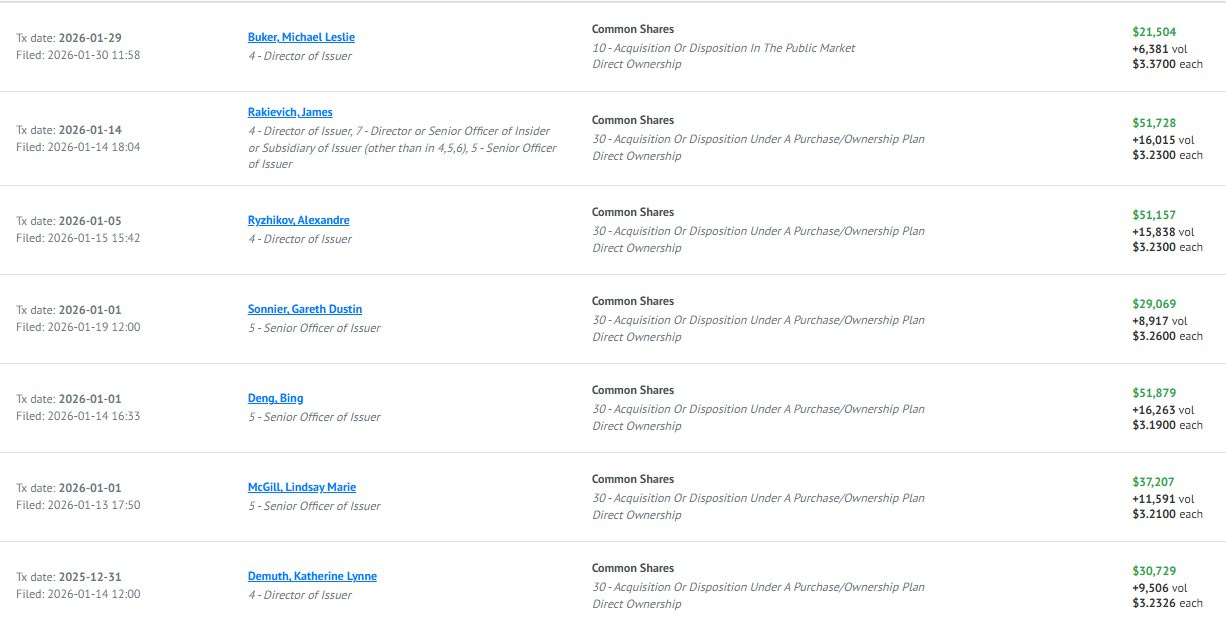

30% institutional and 5% insider ownership

7 different insiders were buying either in the open market or through their company purchase plan in the last three months. At an average price of about $3.25/share so they are down about 18% since.

Income Statement:

Revenue for the year came in 8% higher than 2024 to $83.8M vs $77.5M. Gross margin slipped by over 200 basis points to 33.5% resulting in only 1.6% more gross profit dollars on that growth.

Operating expenses were flat at $17.7M but total expenses grew by 4.2% due to increased finance charges and foreign exchange losses. Thanks to a $400k savings in taxes, they did squeak out 2% growth in net earnings, $9.02M vs $8.87M.

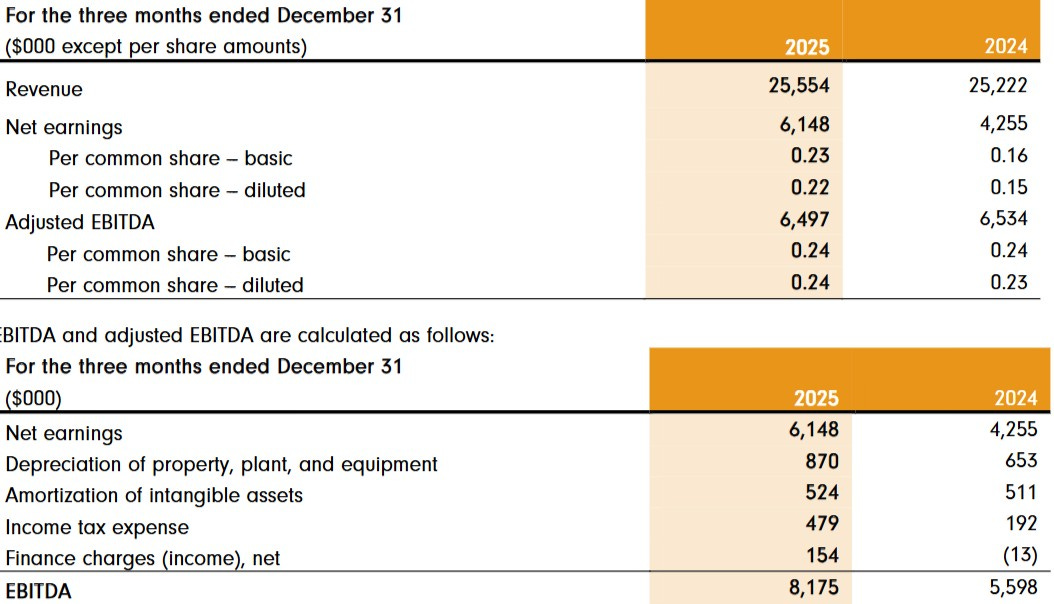

At the top of the review I mentioned the danger zone from my February WWW earnings preview article. In that I mentioned Q4 concerns as they were up against that big record quarter a year ago.

Not only did they offset their revenue from last year with a small 1% increase, but they grew net earnings by 44% and EBITDA by 46%.

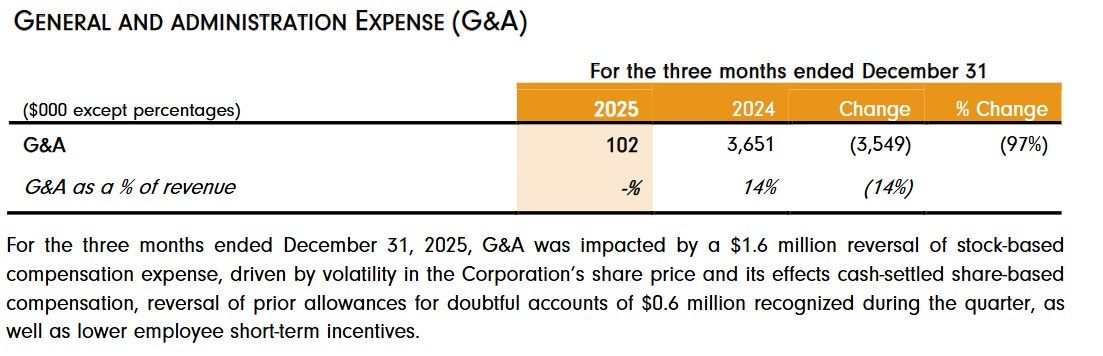

While the quarter overall was much more successful than I had anticipated, unfortunately much of that earnings improvements were non cash impacting including a $1.6M reversal within stock based compensation.

Overall:

If Q4 was better than I anticipated, why did the share price take such a beating yesterday?

Two main reasons as cited within their news release which accompanied their results yesterday. The current conflict in the Middle East and pausing their quarterly dividend.

Personally, the dividend issue is a very minor one for me. As a small cap investor, I’m not seeking companies with 3% dividend yield, at least not for that segment of my portfolio.

The conflict concerns are more troubling for the near term and those will only grow the longer this regional war lingers.

On the positive side, backlog is up from this time last year and their order intake in the quarter was up 42% from last year and their second best in the last two years.

The problem is more than two thirds of that increased backlog stems from the Middle East which likely pushes revenue and cash inflows back during the year. How long is anybody’s guess in these uncertain times and investors do not have much patience for uncertainty.

So back my original question, does the thesis still hold? I think both bulls and bears have a good case to be made.

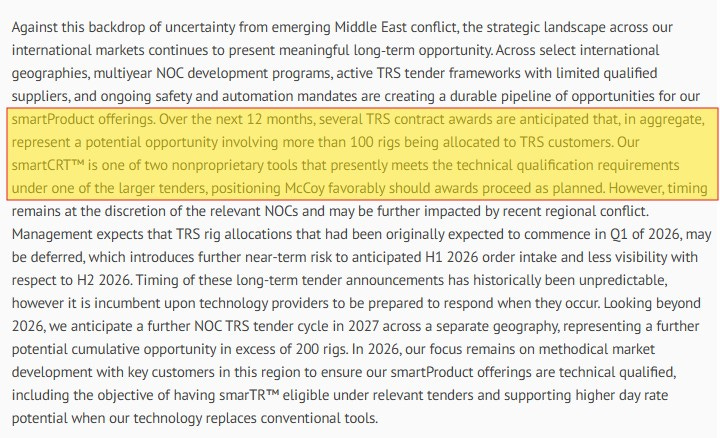

On the bullish side, the company has great products and their diverse product offerings within the sector give them a competitive advantage. That competitive advantage puts them in a prime position when bidding on new contracts, of which more than 100 could be awarded this year.

However, due to the same ME conflict, even those NEW tenders could be pushed back. But higher sustained oil futures could spur new investment in the sector increasing in other regions creating additional future opportunities.

From a long term TAM and competitive advantage perspective, I think the thesis continues to hold.

Where the thesis starts to come into question for me is the apparent cash mismanagement situation the company is currently in. Firstly, McCoy carries a very high amount of inventory relative to their revenue and that turnover ratio only worsened with inventory values growing at a higher rate than sales. To make matters worse, the company writes off an alarming amount of inventory each year.

But the biggest factor for their decision to halt their dividends is the management (or lack thereof) of their accounts receivables. Almost two thirds of their A/R is over 30 days aged. Getting paid from your customers should be more reliable than an invitation to sit on Trump’s Board of Peace. The Middle East sitch only amplifies the poor cash management of the past.

I added to my position yesterday on the dip. I’m starting to regret that decision. This could get cheaper, even with a current P/E of 8.

A second consecutive downgrade. Three stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.