It’s been one year since my initial review of Kneat which received a rather encouraging three star review.

In 2024 they achieved 43% more revenue with a 750 basis point improvement in margin while only spending 15% more in opex, all contributing to a Wolf Trifecta. While those initial results had a brief positive impact on the stock, it did not last. Combine that with SaaS becoming a dirty word in the last four or five months and the result has been a 30% decline in share price with Kneat trading at levels not seen since the summer of 2024.

While I did deem them expensive at the time, I did some two year projections modelling their 2024 performance. How did that model live up to their actual 2025 performance, and how should we value Kneat today are questions I’ll attempt to address.

Balance Sheet:

Kneat maintains a solid current ratio of 1.8, but that is noticeably lower than the 2.3 they stood at a year ago. That consists of $48.7M in cash, $15.1M in receivables and $1.8M in prepaids against $36.1M in liabilities due over their 2026 fiscal year. Nearly $19M of those liabilities are in contract liabilities for which deferred revenue will be recognized against, so in actuality their liquidity position is much stronger.

No unusual findings within their accounts receivable, in fact 45% of their A/R are from R&D tax credits.

Kneat has $21.5M worth of debt, $7.5M of which is payable within 2026, and not at the most attractive rates at EURIBOR +7% & 2% which had an effective rate of around 13% last year.

Cash Flow:

Kneat generated $12.3M in operational cash flow in 2025 and that is 40% better than they achieved a year ago. They also made $6.6M of payments towards their debt (principal & interest), received $1.4M via stock options exercised and spent a net of $20.1M in intangible assets.

While their operational cash flow is impressive YoY, it is notable that the company generated $17.5M worth of OCF in their first quarter, and burned cash in each of their last three, including over $3M in Q4.

So, despite the significant improvements in OCF, their overall cash depleted by 17% during the year due to their intangible asset investments.

Share Capital:

95.7M shares outstanding, 2% dilution during 2025 via RSU’s and options exercised, but 22% dilution over two years from their two raises in 2024

648k options outstanding (0 granted in 2025). All currently ITM with more than half expiring in August at $3.45

1.69M RSU’s and 728k DSU’s (1.1M & 74k awarded respectfully)

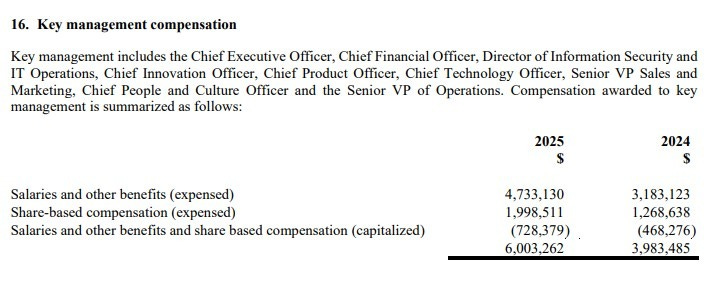

Over $5M in SBC costs during 2025

21% insider and 19% institutional ownership (per Yahoo Finance)

About $150k of shares were purchased by insiders in the open market in November. Most RSU’s in 2025 were exercised for cash

Income Statement:

Total revenues on the year came in at $63.3M. 29.3% more than they achieved in 2024. Gross margins improved once again after significant improvement in 2024, this year growing by 70 basis points to 75.8%

Unfortunately, total operating expenses grew by a larger rate than their rate of revenue and gross profit growth, by 32% and this was consistent across all three of their major spending buckets. R&D rose by 28%, Sales & Marketing by 33% and G&A up by 40%. This resulted in their operating loss growing by $2.5M or 42%.

After other expenses and foreign exchange net losses improved to $2.35M vs $7.73M.

In looking at Q4 alone, revenues grew by 24%, gross margins improved by 210 basis points to 77.6%, and total operating expenses were up by 26%, once again at a higher rate than revenue. This along with a foreign exchange bogey assisted to increase their net loss from $2.5M to $3.6M.

Overall:

At the end of my review last year I through out these “what if’s” if they mirrored their growth from 2024. Not only was their growth slower, but their expense growth significantly outpaced their revenue and gross profit gains.

2025 certainly seemed to take a step backwards from a valuation perspective in my opinion. If we remove the significant impact of forex gains from these results, their NNI loss in 2025 would have grown from $9.1M to $11.5M on nearly 30% more business. That’s also before considering that foreign exchange resulted in a loss in Q4 for the first time in a couple of years.

I have their current metrics somewhere in the neighbourhood of over 30x cash flow with an EV/EBITDA over 90, while continuing to produce negative ROE and ROIC.

The fact that they are only projecting break even free cash flow in 2026 doesn’t get me anymore excited about the prospects of Kneat, particularly in a SaaS sector that is about as popular as a red headed step child these days.

Same three stars as last year but I like them a lot less.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.