We are back again for my tenth review of KITS. The first way back in November of 2022 with my initial coverage and I awarded them an initial 3.5 stars. Shortly after that I took a position at $2.50 and also chose the company as one of my 2023 Wolf Picks.

I was able to turn it into a four bagger, but I am completely out of my KITS position as of today, first selling off about 80% of my position on the day the insiders sold $13M of their positions in a block trade at $10.15. I was more than happy to take my profits in the $10.50’s, and then earlier this year closed the rest of my position.

Due to the valuation back in November still hovering just under $10 I also gave KITS a downgrade to 3.25 stars. The stock reached as low as $7.13 earlier this year before rebounded in January when the company issued preliminary numbers.

Noticeably absent in those preliminary numbers was any mention of anticipated profitability. We now have their full results, so let’s take a look at how their year ended.

Balance Sheet:

With deferred revenue removed from current liabilities KITS has a current ratio of 1.4 that consists of $19.3M in cash, $2.5M in receivables and inventory valued at $22.5M against liabilities due within the next twelve months of $31.9M.

Their balance sheet ratios have remained fairly constant throughout the year but the largest notable change is the $5.4M increase in inventory in just the latest quarter and 46% higher than where they ended their 2023 fiscal year, noticeable higher than their 32% revenue increase and weakening their turnover ratio. Could be timing differences given the $10M jump in payables but it is worth monitoring when they report Q1 next month.

KITS has $6.6M worth of debt across a BDC loan and promissory notes.

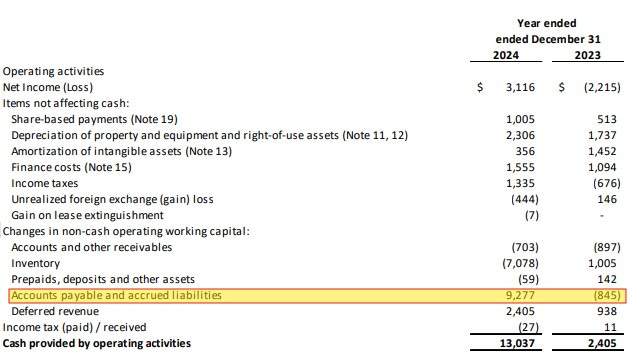

Cash Flow:

KITS delivered an impressive $13M in operational cash flow during 2024, well over 5x of the $2.4M generated in all of 2023. Accounts payables ballooned however within the working capital changes, so I suspect when their payables are caught up it will have some reversion in the next couple of quarters. Either way, it’s still an impressive jump YoY.

KITS also paid down $3.7M worth of debt, bought back a modest $213k worth of stock and utilized $3.15M in hard assets, mainly equipment.

Overall, KITS improved their cash position by 20% during 2024.

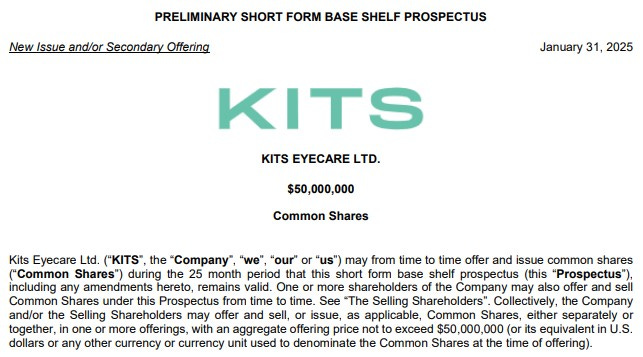

What I find very interesting given the above is the very quiet announcement of a $50M USD base shelf prospectus at the end of January. There has certainly been no news release accompanying this and their use of proceeds within the document couldn’t be more vague.

I think investors might like a little more detail on this BSP, since it would potentially dilute shareholders by about 25% based on today’s share price and market capitalization. I can’t believe nobody asked about this on the conference call, am I the only one who noticed?

Share Capital:

31.6M shares outstanding with only 122k worth of dilution (.4%) that includes 25k in shares repurchased.

2.65M options outstanding, all ITM. 420k were exercised post financials at $2.61

Minimal RSR’s outstanding with the company having a very responsible history of SBC

KITS has approximately two thirds ownership between insiders and institutions

While insiders have been purchasing under their purchase program, those are dwarfed by the $13M of insider sales during the Sept 2023 block trade

TBD dilutionary measures under the company’s outstanding Base Shelf Prospectus

Income Statement:

Yet another big beat on the top line with $159.3M in revenue, 32% up from 2023 and in Q4 and 42% up in Q4 coming in at $44.8M and that is up 7% QoQ. KITS made progress in Q4 in their gross margin with their GP 130 bps better than the comparable quarter, up to 36.3%, but on a full year basis, gross profit was a little worse than flat 36.7% vs 36.8%.

Total cash burning expenses rose by 24%, therefore there was some conversion on their 32% revenue growth with Fulfillment costs rising by 16%, marketing up by 29%, and G&A costs up by 28%.

Net income for the year came in at $3.1M, with almost all of that coming in Q4 which resulted in $2.7M of net income.

Overall:

Another very successful year overall for KITS but my valuation questions still remain. The $3.1M in net income profitability is a $5.3M turnaround from the $2.2M it lost last year but $3.6M of that variance was due to a birdie received in foreign exchange. Even if you give them full credit for the net income achieved that still equates to a P/E of 90 so when 84% of that E comes from foreign exchange gains, it would make it a tough ask for me to want to step in and take another swing at KITS right here.

With that said, I like their progress. I think they have a lot of good things going for them and I plan to still continue being a customer as I like their products and customer service. But as an investor I’m still in a wait and watch mode while it’s up here in the $9 range. If I lose out on future gains I can always look back at the 4x I made here and sleep very well at night. I also don’t like overhanging BSP’s which can be dilutionary time bombs.

I will upgrade them back to 3.5 stars due to their Q4 momentum and future guidance which will give them another QoQ increase in Q1 ($46-$48M).

Paid Subscriber Benefits:

FinsDontLie Scholastic Series - exclusive educational posts

First access to annual picks, upgrades and mid year picks.

Monthly “What’s Wolf Watching” preview of upcoming earnings and potential market moves.

Paid subscriber chat.

My entries & exits. Thoughts, charts and Q&A.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Congrats on the 4 bagger! Seems like a great company with solid financials, but price is a bit too high for me. I think this might be a good long-term investment, but not so much for short-term gains.