Back to back weekend reviews of stocks that I put into the “Danger Zone” in my Feb WWW article. Yesterday we looked at McCoy Global, today KITS Eyecare.

February WWW - "What's Wolf Watching

From Microsoft to microcaps, to say that earnings season has been sub-stellar of late would be an understatement.

KITS was in the group of my first year of Wolf Picks in January of 2023 when it traded at $2.58. I completed my exit sometime ago for a 500% gain only to see the stock continue to rise to $22.50 for a near 9x from that pick three years ago.

Even with the recent large pullback from the beginning of the year, the stock is still trading 66% higher over a one year time frame.

I had the following to say few weeks ago when previewing KITS’ earnings:

In the two days of trading since their earnings were released, the stock dropped by 15% and is down 21% from my article.

While I’m out of the company as a shareholder, I’m still an active customer with our household buying 5 pair of eye glasses over the past six months. But the stock has been trading at Tesla like multiples for sometime, and there isn’t the same cult mentality behind KITS. My latest review of KITS received 3.5 stars, but was downgraded earlier in the year from 3.75, mainly due to my perceived inflated valuation.

The stock sold off huge on Thursday and continued that trend on Friday finishing down another 2%. It bounced off $15 support to close at $15.50 and is currently still oversold with the RSI below 29. Does that mean it’s time to re-evaluate KITS and flip the Danger Zone into a Buy Zone?

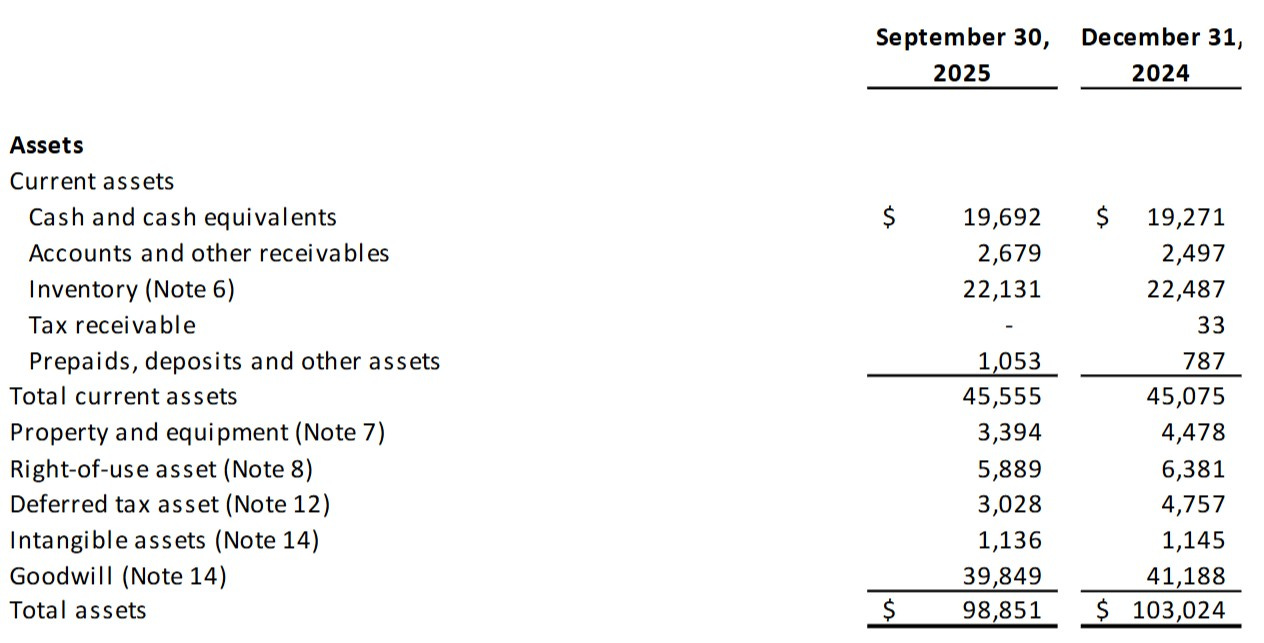

Balance Sheet:

KITS has maintained a relatively stable current ratio for a couple of years now. They ended 2025 with a current ratio of 1.6 (deferred revenue removed) which consisted of $29.8M in cash, $3.9M of investments, $2.4M of receivables, $23.7M worth of inventory and a million in prepaids over top of $38M in liabilities due within their 2026 fiscal year.

The company continues to manage their inventory very well experiencing a 20% increase in inventory turnover and their A/R is mainly derived from credit cards and supplier rebates.

KITS had a little over $10M of debt, but this was fully extinguished post financials. This leaves them with only $290k within a promissory note.

Cash Flow:

KITS produced $11.5M of operational cash flow in 2025, but that figure is down by 12% from the $13M generated in 2024.

They incurred about $3M in net debt, received $1.8M from the exercise of stock options and made investments of $5M.

Overall, their cash position increased by 51% during the 2025 fiscal year.

Wait a second, let’s rewind the tape for a second.

Didn’t I say in the assets section they had $3.8M of investments? But they utilized $5M of cash in investments earlier in the year.

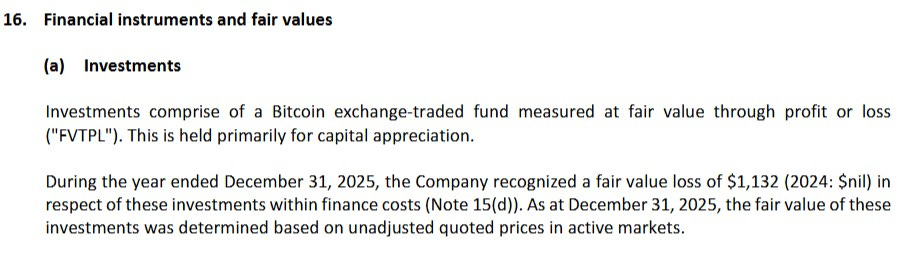

Let’s start the rewind at the end of Q4 where they had zero investments listed on the balance sheet.

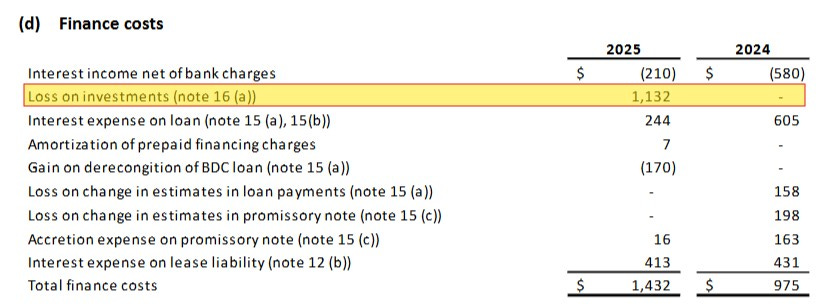

Then in their annual filings, they report Investments under current assets at a value of $3.86M. Within the financing section of the cash flow statement, it states they spent $4.99M on investments. So within the three month period of September 30th to the end of the year, they lost 22.6% or $1.13M on an investment. What did they invest in?

Bitcoin? Are you serious? Let’s move on for now, but I’ll have more to say about this later.

Share Capital:

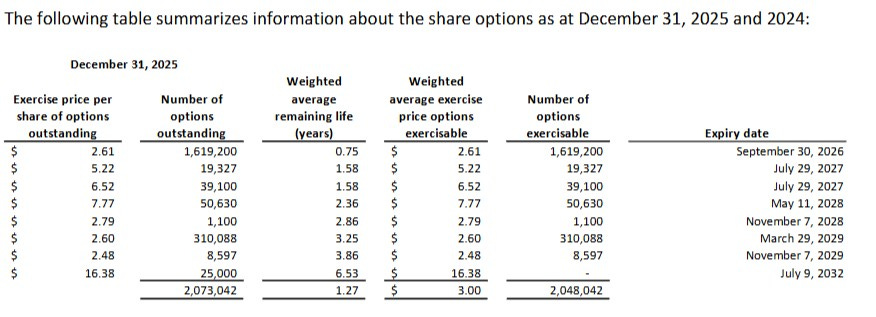

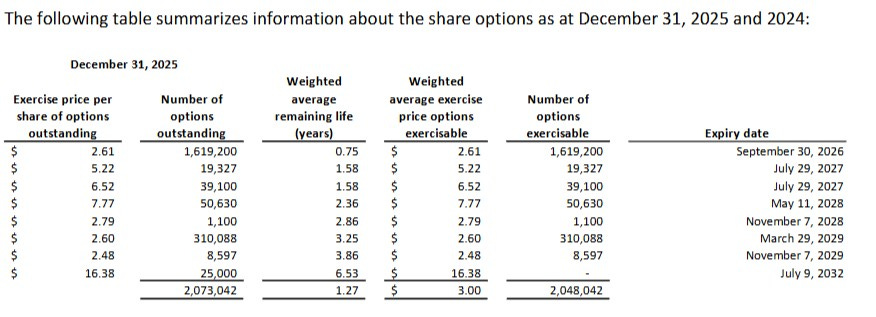

32.2M shares outstanding, 2.2% dilution during the year from RSR’s and options exercised

2.07M options outstanding with only 25k currently out of the money

1.6M options at $2.61 will expire at the end of September. When exercised, this will dilute the float by approximately 5%

108k of restricted share rights were awarded during 2025

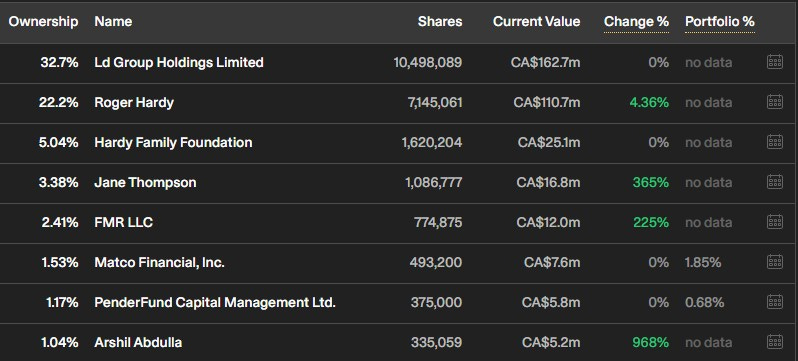

Very high insiders, private company and institutional ownership with about 25% held by retail

Moderate insider buying in the open market in the last six months

Income Statement:

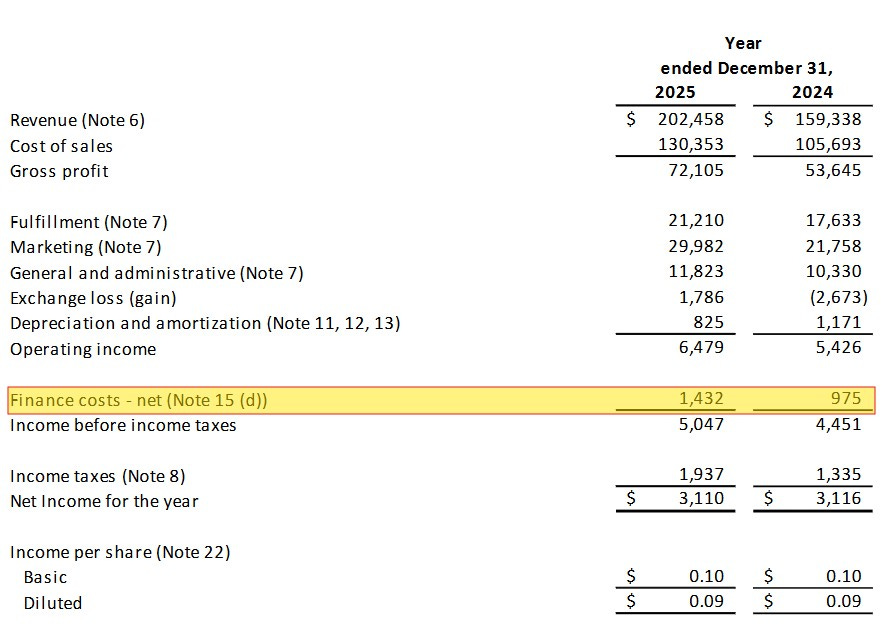

Incredible year on the top line for KITS exceeding $200M for the first time finishing with $202.5M, a 27% increase. After posting $92M in 2022 when they were first selected as an annual Wolf Pick, they have grown by 32%, 32% and now 27% in the past three years.

Gross margin grew by nearly 200 basis points from 33.7% to 35.6% and that helped to generate 34% more gross profit dollars.

Unfortunately, KITS generated near zero operating leverage in 2025 with their cash burning operating expenses rising by the same rate of revenue. Fulfillment costs rose by 20%, G&A by 15% and Marketing by a concerning 38%.

Unfortunately the company had a $4.5M bogey to last year in foreign exchange, suffering a $1.8M loss this year compared to a $2.7M gain a year ago.

After $500k in increased finance costs (more on this later) and $600k in additional income taxes, net income on the year was flat at $3.1M.

That has to feel awfully disappointing on $43M more in revenue and $18.5M more in gross profit dollars.

Overall:

Let’s start with the positives. Their revenue growth was outstanding yet again and surpassing $200M in annual revenue is a major milestone. To top it off they did it with nearly 200 basis points of additional margin.

The exchange loss this year had a significant impact on profitability, where last year the exchange gain made the company look more profitable than they really were accounting for 86% of their annual net income. If we normalized their net income without forex, it would be $4.9M of profitability vs $431k last year, growing it by over 11x.

Unfortunately, foreign exchange is a fact of life, but I will give the company credit for better improvement than the comparables would appear.

KITS also increased their “Active” customer base by over 16% eclipsing 1M, and have a very high repeat business within their contact lens category.

On the flip side, while the company has been able to obtain some leverage with their G&A and Fulfillment costs, the same can not be said for their marketing spend which rose from 13.6% of revenue in 2024 to 14.9% in 2025 and year over year grew by more than 1000 basis points of their growth in revenue. Much of this contributed to a 12% decline in operating cash flow on the year.

Now let’s get back to this Bitcoin investment, which I was not expecting to find within this review. This is the kind of thing that I would expect from shitco’s trading on the CSE (see LEEF Brands), not one of the best performers on the TSX over the past three years.

We do not know the exact ETF vehicle KITS invested in, but if we look at BTC’s chart we know the company lost 23% of their investment sometime within this highlighted window. BTC ended the year around $87,400 so by that we can assume KITS purchased $5M of this ETF around the time Bitcoin traded around $114k.

BTC currently trades just below $67k meaning the company has lost as much as 41% of their investment as of today - in approximately five months. If that value holds by the end of the month, that would suggest KITS would take another $900k or so hit to their profitability based on this investment alone. That would represent more than half of their profitability from Q1 of 2025.

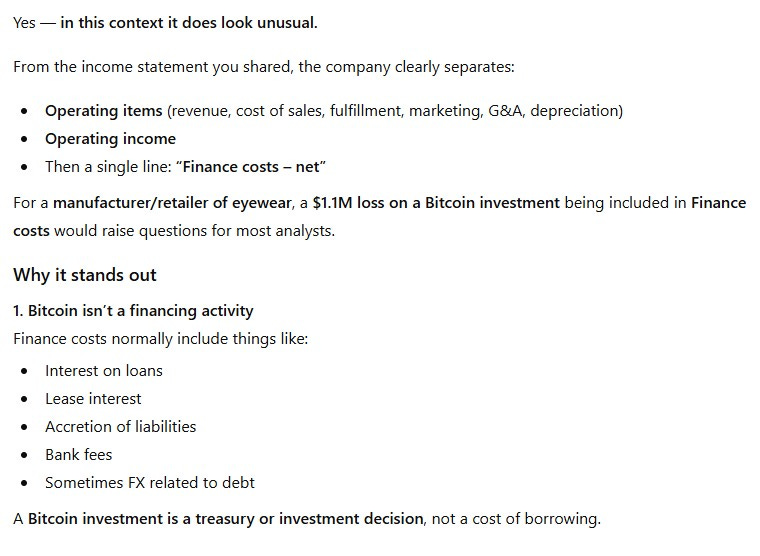

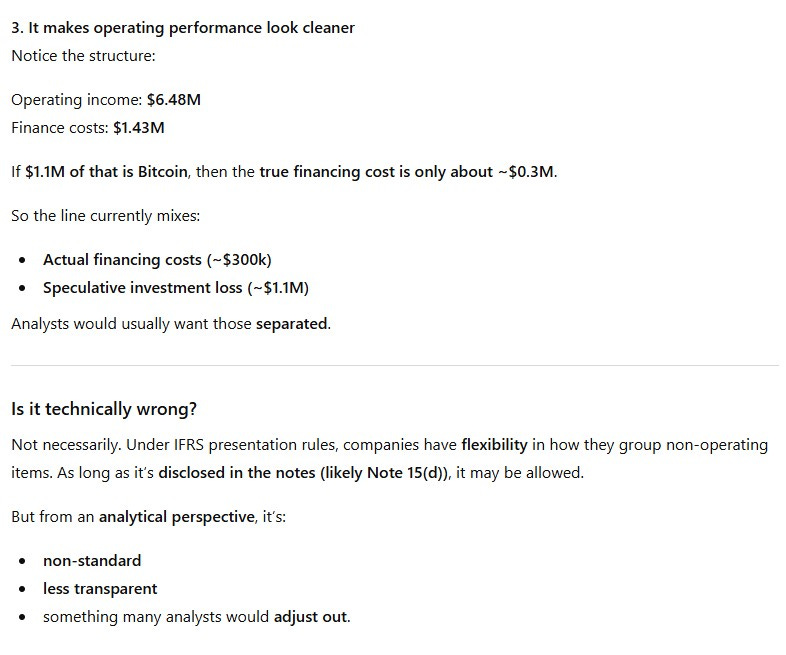

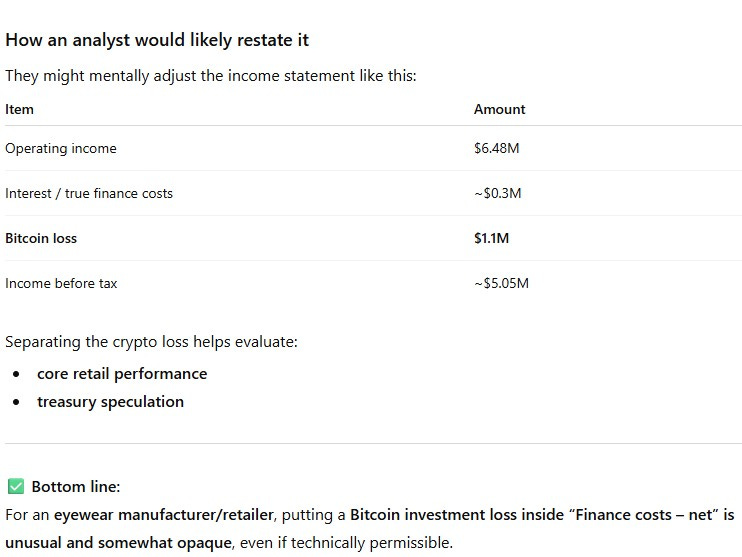

In my opinion, the optics get even worse, as this item is buried in a very unusual category within the P&L. It certainly gives me the impression that they stated it this way in an attempt to hide it from investors.

In an unusual move, I asked two AI agents their thoughts, and both Grok and ChatGPT gave similar responses. ChatGPT gave the best comprehensive answer in my view so here is what they said based on my query, “Would listing a loss of investments on the income statement within "Finance Costs" seem unusual to you?

Let’s leave it at that for now.

Now let’s review the valuation of $500M CAD. That drives some very expensive looking metrics of 175 P/E, 45 EV/EBITDA and 47x Cash Flow. Investors have been willing to pay this premium for KITS for sometime based on their tremendous growth history.

Personally, I’m willing to pay a metrics premium when I’m confident growth will continue at a solid pace AND I believe the company can improve their profitability margins. Their current EBITDA margin is around 5% and I would want to know how they can grow that into double digits.

If they doubled sales to $400M and delivered 10% EBITDA of $40M, a 12x multiple would put them at a market cap of $480M. They are at $500M already which still suggests to me that they are highly overvalued.

Coming into the review, I would have anticipated that I had valuation concerns. But now I also have management issues with their judgement and I’m not sure that I can trust their transparency. Responsible leaders of half a billion dollar company’s do not risk nearly half of their annual operating cash flow in highly speculative assets such as Bitcoin.

I did not listen to the earnings call but I did download the transcript. There was not one mention of Bitcoin, nor did any of the analysts covering the stock from Desjardins, Beacon Securities, Cannacord, Stifel or Roth Capital even touch on it. But they spent a lot of time asking about AI glasses, which to me feels like a strategic distraction. This is why you read the Wolf.

Three stars. Downgrading one quarter star on the results, and another quarter star for loss of faith in management.

(Written wearing a pair of KITS Adler frames)

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Christ, you've got to be smart to figure all this out and carry notes from previous years....thank goodness I found the wolf man.

I'm not invested and sold earlier for good profits, even so....what a Mick mack

Reckless abandonment for a management team to invest in bitcoin. What were they thinking, and after the trade unwound why did heads not roll!!! This trade is something I would do…😟