KITS Eyecare $KITS.TO FINS Review

Q2 2024 (3.75 / 5)

After writing about numerous horrible tickers of late it’s always nice to come back to a winner.

Kits was a 2023 top annual pick of mine and recently hit 4x from that call, continuously putting out improved numbers quarter after quarter. I’m both a shareholder and a customer.

KITS helps customers see better with style, I help investors focus on what’s important within their financials rather than what their news release might say. Let’s dig in.

Balance Sheet:

Current ratio of 1.48 that consists of $19.3M in cash, $1.7M of receivables, $16.3M worth of inventory and $1.8M of prepaids against $26.4M of liabilities due within the next twelve months (deferred revenue removed). They have reduced their long term loan by 1/3rd since the start of the year, down to $3.1M and have $2.1M remaining of promissory notes. Solid and also notable that they continue to improve inventory turnover.

Cash Flow:

$7M worth of operational cash flow generated through the first half of the year, doubling up on the $3.5M they generated at the same time last year. This number does have a big assist from working capital changes due to a significant rise in their A/P of $4.8M, so while this doubling is indeed impressive, I don’t believe it will continue to trend this good for the rest of the year.

After paying down $1.9M in debt, and adding $540k in assets they were still able to improve their cash position by 25% since the beginning of the year.

Share Capital:

31.5M shares outstanding with very little history of dilution in a very well managed float

Over 80% owned by insiders and tutes

2.8M options outstanding and a handful of RSU's

Insiders buying semi regularly both in the open market and through their share purchase program

Income Statement:

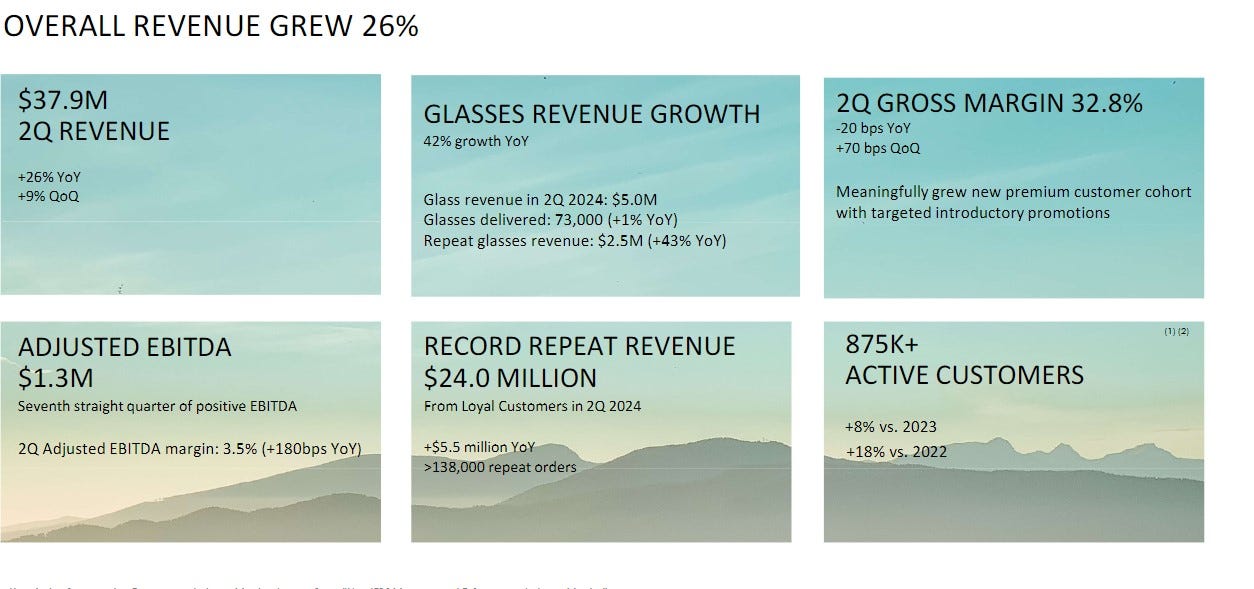

The revenue train keeps on rollin with $37.8M achieved in Q2, a 26% increase over the comparable quarter and now halfway through the year have achieved $72.6M, again a consistent 26% more than a year ago.

Gross profit for the quarter came in at 32.8%, slightly off by 20 basis points they achieved in Q2 last year. On a YTD basis, margins are at the same 32.8% rate, a similar 20 bps off last year.

A bit of a mixed bag on the expense lines. They have converted fairly well on Fulfillment and Marketing costs which YTD rose by 15.5% and 18.2% respectively, but G&A costs have risen by a greater rate than their revenue performance, 31%.

The profitable quarter on the income before income tax line of $400k comes after a just better than break even quarter in Q1 with YTD net income of $476k, a more than $3M improvement from their $2.7M loss experience through six months last year.

Overall:

Hard to be more impressed with the progress they have made since my initial review of them about two years ago. But they are no longer that undervalued, hidden gem of a stock trading at a $75M market cap anymore. They are a $300M market cap now. They are trending still at a reasonable 2x P/S ratio as they should eclipse $150M in 2024. The other ratios relating to profitability are certainly a little more suspect now. It also has to be noted that two thirds of their profitability improvement is related to foreign exchange differences - $2M. That’s pretty significant, and when the market we live in is one of “what have you done for me lately”, they are one mediocre quarter away caused by macro conditions away from a healthy price correction IMO.

They are delivering strong growth across segments and delivering consistent gross profit a pretty decent job on expenses, while reducing their rather negligible debt. They continue to grow their active customer base and in turn increases their repeat revenue. I also feel they have the goods to keep that revenue train going for some time too.

That valuation today though (as happy as my portfolio is) feels like it’s on a razor’s edge at these profitability metrics.

Invest safely, wear a rubber (I mean your glasses). Maintaining 3.75 stars.

Buy Wolf a coffee which goes towards website maintenance costs

Have an request to review a stock you are interested in? Visit the TSA discord to make your request in our dedicated channel or email us at thewolf@wolfofoakville.com

Chat with me and 2800+ other members daily in the TSA Discord.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings and I do so without compensation. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.