This will be my first review of this tiny picocap trading at a $9.5M valuation. It’s not the first time I have done any research on them however. They did come up as a suggestion for a 2026 Wolf Pick, but they did not make the cut for reasons I cannot recall.

While the stock is up 30% over the past year it trades very choppy, down nearly 50% from their July highs. If one zooms out, Innovotech is trading at nearly the same valuations they did five years ago.

Innovotech Inc. is an established and scaling life sciences services and technology company specializing in contract research, analytical, and microbial testing within regulated healthcare markets.

The company announced their annual results on Tuesday evening reporting more than double 2024 revenues. The market responded positively on Wednesday sending the stock up 22%, but then were nailed to the cross by 10% on Thursday to end the short week leading into Easter weekend.

It feels like a company who struggled to hit $1M in sales five years ago that just doubled their revenue this year should be in a better share price position, and not down by 50% over the last nine months.

What’s missing? Let’s try to find out.

(Paywall will be removed on Saturday April 11th and be available to all readers)

Balance Sheet:

While the numbers are small, Innovotech has a very liquid and solid looking balance sheet. They sport a current ratio of 6.7 that consists of $1.6M in cash, $700k in receivables, and $500k in other short term assets against only $451k in liabilities due over the next twelve months (deferred removed).

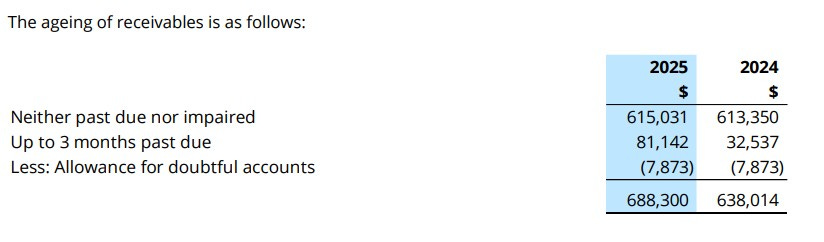

Receivables are solid, as evidenced by their aging (not ageing) report with 89% of money’s owed being current.

Longer term, they have $100k in contingent consideration from last years acquisition and $160k in convertible debentures.

We’re off to a very solid start.

Cash Flow:

Over the past two years, Innovotech has been just on the wrong side of cash flow neutral, experiencing $62k of cash burn in 2025, slightly better than the $82k suffered in 2025.

The company converted $550k worth of long term investments to cash, and purchased $470k worth of assets during the year. They raised nearly $800k to the treasury through options and warrants exercised, raised $200k through convertible debt and paid out $100k of contingent consideration.

Overall, they improved their cash position by over 120% during 2025, which makes the $200k in convertible debentures a curious decision, although it was done at a premium to market at $0.25.

Share Capital:

54.4M shares outstanding with 10% dilution occurring during the year, all through warrants (4.3M) and options (370k) exercised

1.9M options with 1.4M currently ITM with all of those expiring within one year

800k potential dilution from convertible debentures, 25 cents expiring in October of 2030.

38% insider ownership (per Yahoo Finance)

Plenty of insider activity with most on the share acquisition side including several warrant and option exercises above the current share price

Income Statement:

As I mentioned in the opening, Innovotech had a solid year on the top line with $4.53M in revenue, 107% better than their previous year. Margins also improved by 230 basis points to 52.9% which helped drive gross profit dollars 116% higher.

The company falls well short of achieving the elusive Wolf Trifecta however with 118% more in cash burning operating expenses. This significant increase in spending was experienced in all buckets - G&A costs rose by 102%, R&D by 89% and Marketing and business development increased by 5.5x from $66k to $364k.

All of that performance from revenue and margin lines were essentially wasted from an overall profitability perspective. In fact their net income decreased YoY from $214k down to just $88k on the year.

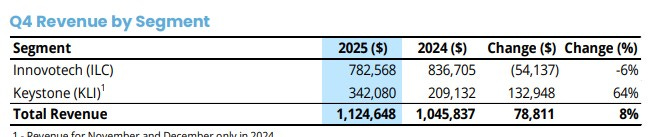

In Q4 alone, revenue was more comparable as their Keystone acquisition occurred in mid Q4 of 2024. Those revenue gains from Q1 - Q3 which surged by numbers between 150% and 270% screeched to a halt with just an 8% gain to close out the year including their organic business down by 6%.

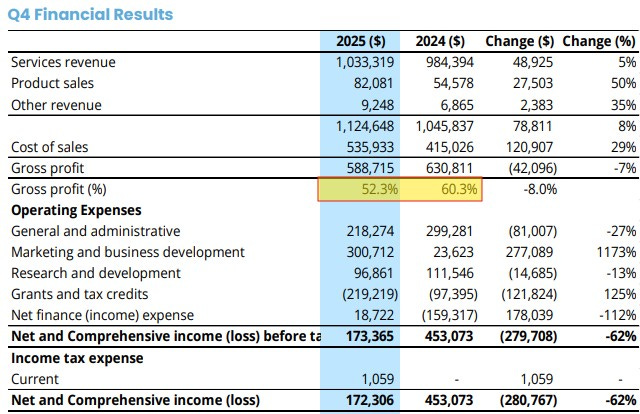

The rest of the Q4 is a bit of a mixed bag. While the total year had a great performance on margin, Q4 was 800 basis points lighter resulting in a 7% erosion of gross profit dollars. Then total expenses were up by 42% on only 8% more revenue and less gross profit. Even with a birdie on grant income, net income was down by 62% in the quarter. On the plus side, it was their most profitable quarter of the year.

Overall:

That income statement felt like a lot to absorb, particularly for a sub $10M market cap company.

Some companies do a better job than others with transparency in their financial statements and I have to say Innovotech is one of the better ones. They do an excellent job of breaking down their business by segment and geographic region. As you can see, while their organic business suffered in Q4, it was quite strong for the total year, up 59%.

If we look backward to the Keystone acquisition, it was done for a total of $517k ($300k cash + stock) with $300k in potential earn outs based on revenue and positive net income metrics. A portion of those earn outs were paid out in 2025 leading you to believe those goals were met. Considering that overall margins improved during the year and Keystone nearly generated $1.4M during their first year, it appears to be a very solid acquisition. Management is continually looking for other similar opportunities, and once you’ve seen one seemingly successful acquisition it should give you more confidence should they announce another.

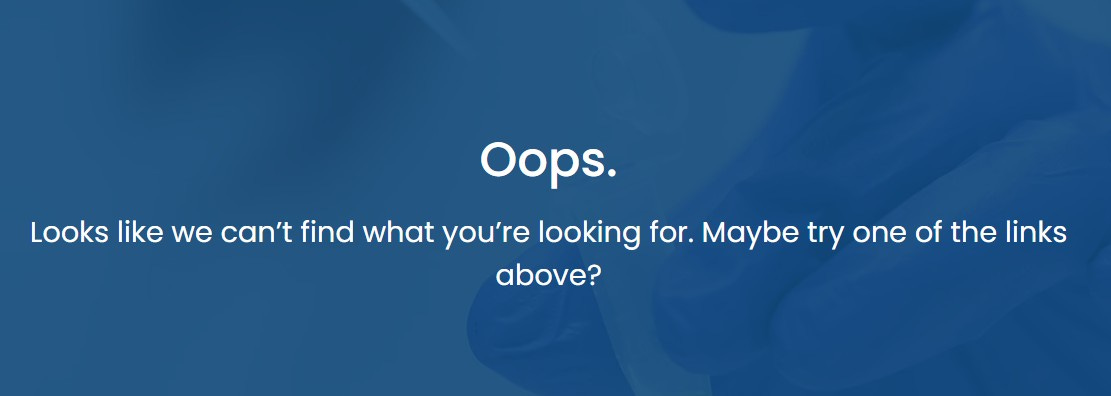

Where do they go next is the question, and that’s where additional due diligence begins. For me, let’s just say that didn’t go very well initially. From their investor relations website, I was asked to enter my name and email address in order to download their investor deck (Note to everyone else, don’t do this).

After entering my information, I clicked the link and received this:

Also, if you recall my introduction, I gave a brief overview of what the company actually does. I didn’t write that, instead it was a cut and paste from the latest press release. What you may notice is I had to correct a spelling mistake within it. This is boiler plate stuff folks, so my introduction to how they communicate with investors did not get off to a great start.

Thankfully, Smallcap Discoveries has done a series of interviews with the company dating back at least five years. I’ve attached the most recent for your viewing and researching pleasure.

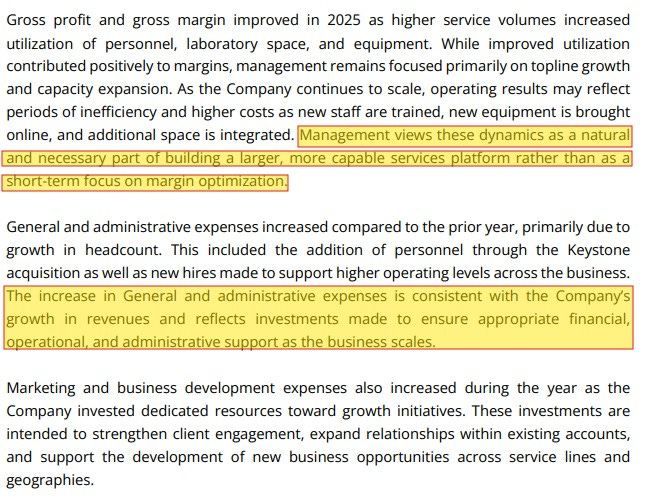

When you go through Innovotech P&L, it shows great organic and overall revenue growth, margin improvement but no operational leverage to take any of those gross profit gains down to the profitability lines. In fact, profitability became worse year over year. I therefore wanted to see some rationale within the MD&A that would speak to increases in headcount due to the acquisition and an indication that future synergies would ultimately gain some of that operational leverage not seen in 2025.

But I didn’t. Instead I surmised these margins improvements may not be sustainable as it is not a primary focus and expenses were just consistent with growth without any comforting statements that would lead me to believe that they would improve.

I won’t go as far as saying I think Innovotech is overvalued. In fact I’d say they look like a much better company than they did five years ago at the same share price. But there isn’t much within these financials to make me want to become an investor, nor did I feel ultimately inspired by the CEO within the attached interview - Paul Andreola asked him all the right questions to provide that opportunity.

Ultimately, it’s a very uninspiring three stars from me.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.