The highly touted Q1 financials are finally upon us. In mid March they provided guidance on the quarter, estimating $20-$25M against just $7M in the comparable quarter. Two weeks later they upped it to $25-$27M.

That sent the stock soaring, resulting in the 10th Wolf Pick in the last three years to hit three bagger status. The stock had a significant pull back yesterday leading into these numbers, nearly by 12%. There wasn’t any detail provided below the revenue line so it’s likely some jittery investors took some profits in case the rest of the numbers didn’t live up to the high expectations.

Up against some time constraints today, so let’s dive right into the numbers.

Balance Sheet:

iFabric maintained a current ratio of 1.8 after Q1 consisting of just $1.8M in cash, $25.5M worth of receivables, $16.8M worth of inventory and $1.3M in other short term assets overtop of $25.3M in liabilities due over the next twelve months.

As you would expect with a nearly 300% revenue increase, A/R grew substantially and we will likely see a negative looking cash flow statement as a result. The company apparently only issues an aging report with their annual filings, but I can say when that was reviewed less than two months ago, it was one of the most impeccable ones I’ve reviewed.

Inventory values only depleted by 20% on all of that revenue and I expected that number to be greater. The company did however increase their scrubs program in Walmart to 1,000 additional stores later in the quarter, so that is likely related.

Liquidity therefore does not look very strong with their cash plus receivables just covering their one year financials commitments, with the A/R portion of that totaling 94%.

iFabric has $12.9M worth of debt, all classified as short term. A good portion of this debt was used to front the significant inventory ramp up in order to support their new programs in Walmart and Costco.

They also have a $3.6M bank loan which I made an incorrect statement on in my last review. I suggested the loan was listed as current due to a covenant of the loan being missed which was later resolved. While that was true the reasoning for the loan being listed that way was due to a “payable on demand” feature in the loan despite it being a long term mortgage. Thanks to the company reps for reaching out to me to clarify.

Cash Flow:

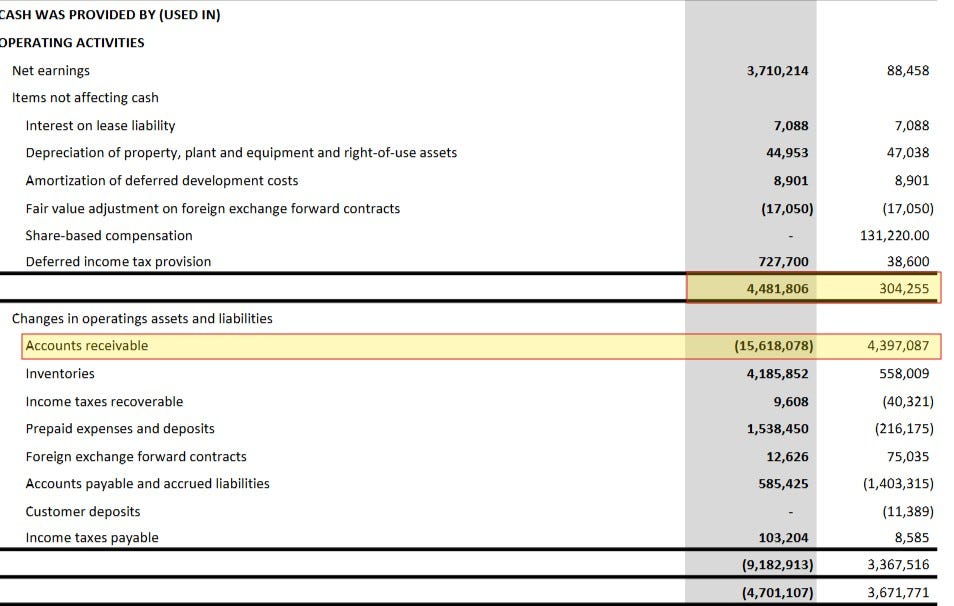

As expected, their Q1 operational cash flow does not look great showing $4.7M worth of operational cash burn compared with generating $3.4M in the comparable quarter.

This is all due to their accounts receivables growth of $15.6M within working capital adjustments. As you can see, prior to working capital changes, their OCF was $4.5M vs just $300k a year ago.

Had this been another scenario where the company was selling to unknown clients, it could be cause for some concern. Since the vast majority of their receivables are with highly reputable retailers, and given their A/R management has been excellent in the past, I feel this will reverse rather quickly with a large stream of cash in the next couple of quarters.

The company increased debt by $2.6M in the quarter to support their growth. Overall their cash depleted rather sharply in the quarter by 58%. Look for a big rebound here in Q2.

Share Capital:

30.3M shares outstanding. identical number from one year ago in a historically well managed float

1.9M options outstanding, all ITM

Zero warrants with all 2.9M outstanding last year, expiring unexercised.

66% insider ownership including 63% from President & CEO Hylton Karon although historically allergic to transactions on the open market

Income Statement:

These financials are the equivalent of an NBA player getting posterized. They slam dunked these financials on the market, while tea-bagging their competitions faces.

Clearly the statement I was looking to review most to ensure the company delivered underneath those record revenue numbers.

Those Q1 revenues came in at $27.5M, a half million more than the high end of their upped estimate of $27M at the end of March. That compares to just $7.1M last year for a 288% increase. Those revenues did come at the expense of some margin due to product mix and entering into big agreement with one of the world most cutthroat buying groups - Walmart. Their margin rate slipped by over 600 basis points to 32.5%. Gross profit dollars increased by 227%.

They gained a lot of operational leverage in the quarter which was what I wanted to see. G&A expense rose by 20%, while selling costs (highly commission based) rose by 135%.

Earnings from operations rose to $4.9M in the quarter against just $115k last year. Even after an expected much higher tax burden they still drove $3.7M to the net income line, 41x more than the $88k last year.

Summary:

That $3.7M in profitability in just their first quarter is higher than any YEAR in the company’s history, and the quarterly revenue figure is 84% of what they achieved all of last year, two huge reasons why the stock is up by 150% since my 2026 Wolf Pick and 275% up from a year ago.

While investors were counting on huge numbers from their intelligent fabrics division, it shouldn’t be overlooked that the Coconut Grove (or intimates) division also achieved massive numbers of a 212% increase.

I guess the big question now is what the company does now for an encore, and how the rest of the year will shape up.

I’ve attached Atrium Research’s initiation report to the image above. It is a very good basis to start your research for anyone new to iFabric, but I will say I think they did a terrible job on the numbers portion which I pointed out in the Wolf Den discord upon it’s release. They really missed the boat on the expense lines, particularly their G&A costs estimating $5M in Q1 which came in under $1.9M. The selling costs numbers for the balance of the year also look light. All of that translated to the bottom line beating their estimates by $3.1M on the Net income line. This actually could have translated into investors selling into the news for today IMO.

To extend your due diligence the company has also updated their investor deck for 2026. Attached below

To better understand how the rest of the year might shake out, the company will be hosting a webinar with Adelaide Capital on Thursday. You can register by clicking the link below.

Until we know whether the company will continue to provide guidance or if Q1 was a one time deal, it is really hard to peg a potential valuation. I think $70M in revenue with $8M in net income is achievable which would put them at a 14 forward P/E with tremendous growth potential. I reserve the right to adjust that thinking on Thursday.

Upgrading iFabric to 3.5 stars with the potential room for a lot more once their cash flow flips, and I am expecting it will.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.