There has been very little to cheer about in the market over the past couple of months, but this 2026 Wolf Pick has been one of the few exceptions. iFabric is up 99% since the pick in mid December and over the past twelve months has gained 141%

That doesn’t mean iFabric has been kind to all investors over the past month. Just last week, a few days after the company provided incredible Q1 guidance, multiple investors (jabroni’s) sent the stock up 27% at the opening bell to $4.50. While that share price did trigger the tenth Wolf Pick since 2023 to at least triple in value (out of 20), it turned out to be a grievous error in judgement fairly obvious to anyone at the time. With yesterday’s close at $2.99, those antsy buyers are down 34% in just 8 days.

Amusingly, in my March WWW article published on March 16th I told readers I was hesitant to call out a buy zone prior to their annual financials, but I felt great about their 2026 comps. Within an hour of hitting send on that article, iFabric dropped news and unexpectantly provided guidance for Q1 - one of the comps I was most excited for.

That guidance called for a potential tripling of revenue at the top end of guidance. In the press release announcing their financials this morning, they increased that guidance - the bottom end of which will at least 3.5x what they achieved in the comparable period.

While I covered my bull case in my 2026 Wolf Pick article, I haven’t performed a full financials review of iFabric since June of 2024. They received 3.25 stars at the time.

Being the eternal skeptic, when they first dropped news about their Q1 of 2026 and not mentioning a word about their Q4 of 2025, it left me wondering if there would be some potential issues. Given my cursory look this morning, that may indeed be the case.

How much should we care given their early 2026 optimistic outlook? Let’s don our best scrubs to dive in and find out.

Balance Sheet:

We are looking at a much different and mixed looking balance sheet than the 4.4 current ratio they ended 2024 with. That ratio is now down to 1.7 and consists of $3.8M in cash, $9.8M of receivables, over $20M worth of inventory and $2.9M in other short term assets against $22M in short term liabilities.

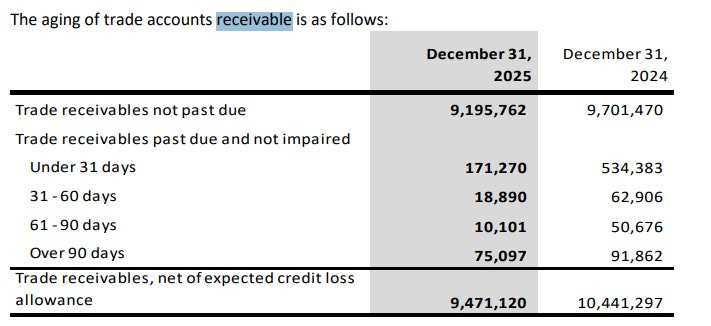

Their A/R aging report is up there with the cleanest I have ever seen with over 97% current.

Inventory values exploded in Q4 to over $20M from $8.5M just last quarter - an expected move to support the new programs for shipment in the following quarter. Their Q1 guidance supports this but this had impacts through the rest of the balance sheet also. Accounts payables increased by $8M and they tapped into their LOC to the tune of $6.66M to support the financing of their inventory wind up.

iFabric has a $3.6M mortgage that does not expire until 2055, but it is showing in current liabilities as the company had failed to meet one of the loan covenants. Normally this would be a yellow flag, but post financials the lender waived this so investors should expect this to return to long term liabilities when the company reports Q1.

Overall the balance sheet is pretty messy, but most of this should look much different in six weeks or so when we see their next set of financials.

Cash Flow:

For similar reasons we have additional messiness within the cash flow statement with the company burning $4.4M in cash in 2025 compared to generating $300k of positive operational cash flow a year ago.

$1.7M of this burn occurred in Q4. Some but not all can be attributed to working capital changes, but a good portion of the rationale was decreased profitability in the full year.

In 2025, iFabric also utilized $2.2M to purchase the remaining 25% of a subsidiary, increased their debt by $9.5M and purchased $340k worth of equipment.

Overall their cash position improved by 84%.

Again, not a great 2025 portion of the financial statements, making their Q1 of 2026 that much more important.

Share Capital:

30.3M shares outstanding. identical number from one year ago in a historically well managed float

1.9M options outstanding, all but 200k ITM

Zero warrants with all 2.9M outstanding last year, expiring unexercised.

66% insider ownership including 63% from President & CEO Hylton Karon although historically allergic to transactions on the open market

Income Statement:

Total revenues of $32.9M in fiscal 2025 a 20% increase over last year. Margins were atrocious coming in almost 1000 basis points less at 31.9% compared to 41.3% in the year prior and that resulted in bringing 7% less dollars to the gross profit line.

Expenses converted fairly well, growing by 12% on 20% more business but the gross margin is the big story here resulting in a decrease of of nearly $2M or 89% in operating income.

After taxes, iFabric experienced a net loss of $100k after delivering $1.6M in profit in 2024.

While margins also didn’t look great compared to last year after Q3, they took a much stronger turn for the worse in Q4, only coming in at 24.1% compared to over 40%, and to have that kind of margin erosion in your best revenue quarter killed the profitability of the entire fiscal year.

Overall:

Investors were aware of their margin difficulties for most of the year, mainly driven by the impact of US tariffs. Q4 had additional margin pressures from license exit costs. In their news release this morning, they had this to say:

Significant improvement is certainly what the market needed to hear, but it’s hard to imagine this gets them back into the 2024 range of 40% plus.

While these financials are certainly worse than I would have anticipated, I’m not sure they matter a whole lot. All eyes now move to mid May when the company will release a very important Q1. Let’s first look at their comps which consist of $7.1M in revenue, 38% margin and just better than flat profitability.

After initially issuing guidance of $20-$25M for Q1 just two weeks ago, they upgraded and tightened it to $25-$27M. The low end of that guidance is a 250% revenue increase, and would represent over three quarters of the revenue achieved in all of 2025.

Let’s attempt to make some assumptions on how the rest of the P&L could pan out. They achieved 38% margin a year ago and 32% in all of 2025 with expected improvements in ‘26. Let’s split that difference and use 35% which would deliver $8.75M in gross profit dollars.

Selling costs appear to be the biggest variable expense to revenue and typically are 9-10% of revenue which would put them at $2.5M. G&A expenses are likely where there is the most opportunity for operational leverage and were $1.6-$1.8M per quarter last year. If we assume that tops out at $2M with another $500k in other expenses that would drive $3.75M in net income and about $4.25M of EBITDA for Q1.

Beyond the first quarter is very tough to gauge and there is no doubt results will be lumpy given the nature of the business. The positive news flow kept going in Q1 with a 1000 store expansion of their scrubs program in Walmart, and the introduction of new programs into Costco. Their Intelligent fabrics division also announced new programs into bedding products and a partnership with Roots on a footwear initiative with Costco to generate up to $8M in year one.

All signs point to the medical scrubs market being the main driver of the company’s outlook in the next few years and the opportunity is extremely significant with a North American TAM of $25B expected to grow 6-7% over the next number of years. iFabric is just touching the surface in market share, but given their launches in two of the continent’s biggest retailers, they are poised to get their slice of the pie. Should they obtain an EPA “kill free” designation (99.9% of bacteria), potentially be the first ever granted, would be a big game changer.

There’s a lot to look forward to and further analyze. Had I just had these financials in front of me, it likely would have resulted in a downgrade. But given their outlook, I’ll stick with the 3.25 stars.

Note, the company will be participating in a webinar to address their earnings and future initiatives with Adelaide Capital on April 9th. You can register below.

Registration link: https://us02web.zoom.us/webinar/register/WN_MhizOHDfRvOql-kgIQr6rQ

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Huh, I thought their balance sheet would look much better than that, but I guess I'll be looking forward to their Q1 numbers.

Also, the line "given their launches in two of the continent’s biggest retailers, they are poised to get their slice of the pie" fills me with a lot of confidence.