It’s been a minute since I completed a FINS review of Haivision. Fifteen months in fact when I awarded them an average three star rating for their 2024 annuals. They “limped across the finish line” as I called it in Q4 last year and I also mentioned they didn’t do enough to interest me enough yet to become a shareholder.

Over the next year, that looked reasonably prophetic as the stock decreased by 32% over the next four months and then traded between $4 and $5 for the remainder of 2025.

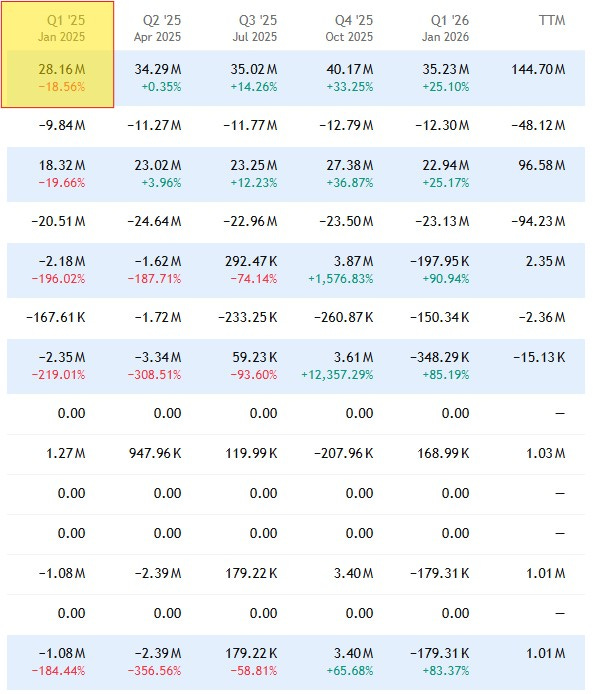

Things changed dramatically when they released their Q4 and 2025 annuals this time around. The stock ripped by as much as 83% over the next ten weeks leading into these Q1 earnings.

In my Feb WWW earnings preview, I told readers I was fading Haivision citing the difficulties of repeating that Q4 performance, at least to the expectations in the market. We are now a week removed from their recent results and the stock has taken a heavy hit, down over 20%.

Where do we see them going from here? Let’s review.

Balance Sheet:

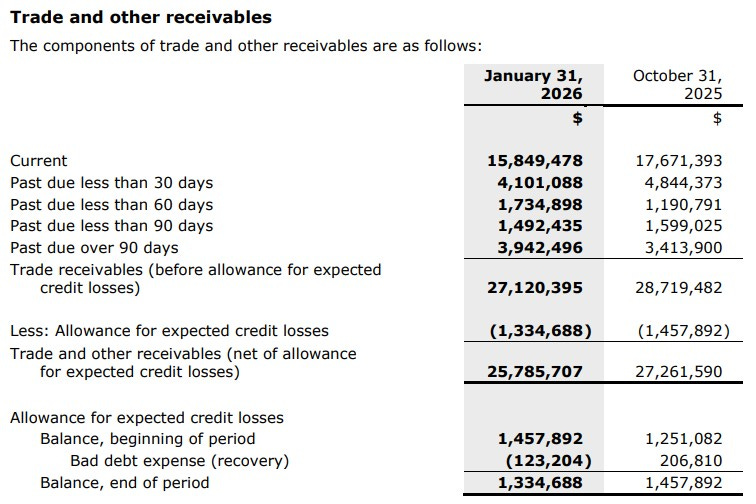

Haivision’s balance sheet looks quite strong. With deferred revenue removed they possess a current ratio of 2.7 consisting of $17M in cash, $25.8M of receivables, $11.9M worth of inventory and $6.4M in other short term assets against $22.7M in current liabilities.

The trend of two items I mentioned a year ago continue, one positive and one not so much. On the positive side they continue to get more efficient with their levels of inventory. Any time you can have 25% revenue growth while carrying 10% less inventory YoY is impressive.

On the other hand, it appears their credit manager has been asleep at the wheel with only 58% of their A/R containing customers paying their bills on time with 15% of them exceeding 90 days past due.

Haivision has $7.6M worth of debt, the majority of which is listed as current under their line of credit. That $5.5M balance is double the amount drawn from year end. It is a relatively small amount of the total available however as it is a $35M loan facility with an accordion feature of an additional $25M.

Despite the A/R concern there is more good that bad here.

Cash Flow:

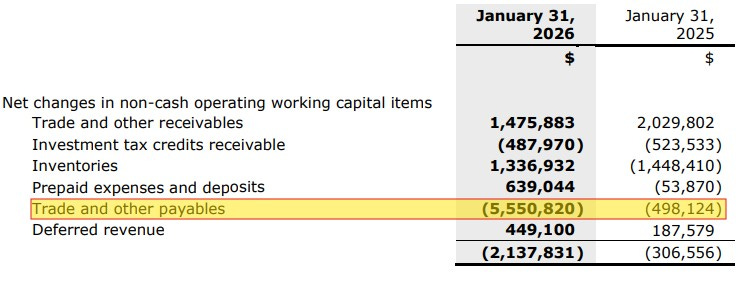

Haivision had $150k of operational cash burn (OCF) in the quarter, in large part due to working capital changes, and this is a $500k improvement from where they stood after their first quarter last year.

Trade payables were reduced by over 27% in Q1. When you pay your bills on time but many of your customers don’t it can result in working capital adjustments that negatively impact your OCF, as is the case here.

Prior to working capital adjustments, OCF improved by over $2.5M YoY, so as long as their A/R aging doesn’t get worse, I would expect their Q2 OCF to be much improved.

The company made small asset investments of $200k in the quarter, increased their LOC by $2.8M (curiously), set aside over $1M of withholding tax for RSU issuance and bought back over $500k in shares.

Overall the company’s cash position decreased moderately by 1.2%

Share Capital:

27.5M shares outstanding, approx 700k less than one year ago

2.6M options outstanding, with over 2.2M ITM

1.28M RSU, 260k DSU’s outstanding and 68k cash settled DSU’s awarded in teh quarter

104k shares bought back in the quarter. The company renewed their NCIB on Feb 3rd, but hasn’t repurchased any since

High insider ownership of 32% with 5% held by institutions (per YF) with no relevant insider activity on the open market worth mentioning

Income Statement:

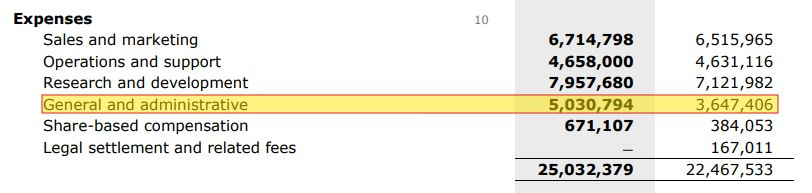

Very solid revenue gains of 25% to $35.2M on the back of a very strong quarter when they were up 33% in Q4. Gross margin remains strong at over 70%, but they were off in Q1 by 150 basis points to last year (72%), and that produced 22% more gross profit dollars.

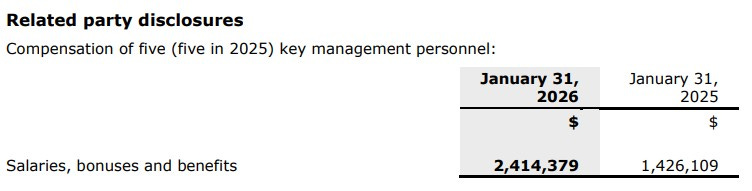

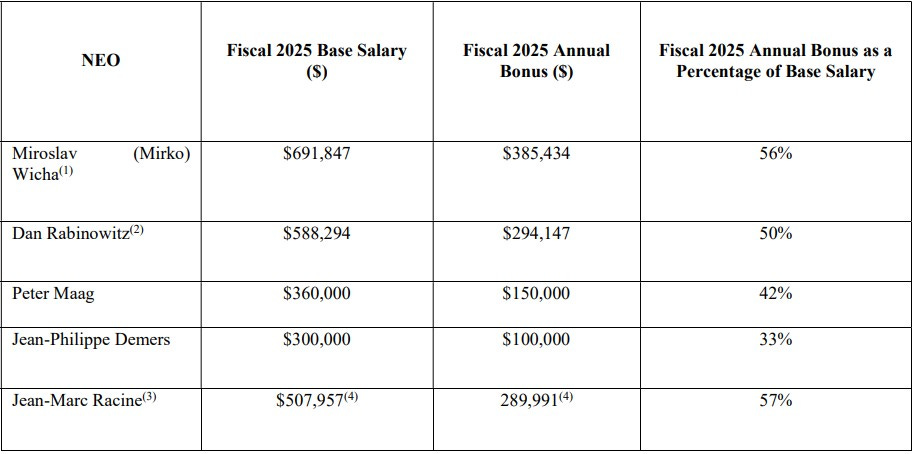

Overall Haivision generated some decent conversion within their cash burning operating expenses which grew at 11%, about half of the rate of their gross profit dollar increase. Ops and support were flat, Sales and Marketing increased modestly by 3%. R&D spending by 12%, but G&A expenses by 38%. The majority of that additional G&A spend went to five key management personnel

At the bottom, Haivision lost $180k on the net income line, but that did narrow from last year by over 83%.

Overall:

In a pure YoY comparison, I would have to say that there is more good than bad here. You may be asking why the stock is down by $2 or a little over 20% since these numbers were released then.

I believe the drop is from much higher expectations given what the company achieved in Q4, and these numbers, although improved YoY did not meet that same bar when compared QoQ. As I said off the top, the share price increased 83% off of Q4 earnings and that creates some pretty high expectations that I don’t believe Haivision lived up to here.

The company was up against a pretty big cupcake of a quarter. The $28.2M in revenue last year was the softest revenue quarter since Q4 of 2021. If you like profitable companies, HAI also delivered $3.4M worth of net income last quarter and experienced a small loss in Q1.

Investors also need to make their own determination on how they feel about the additional $1M in compensation to the five key leaders of the company, nearly 70% more YoY. The variance is the difference between a potential $800k gain in net income to the $200k actual loss. Based on their compensation from 2025, they weren’t exactly joining any food bank lines, while investors were mainly in the red for the past four years.

I think you’re getting the gist on my opinion. I’m going to need to see a lot more based on this $230M valuation which is at an EV/EBITDA multiple of 20 and not converting as much of that EBITDA to cash flow with a 25x CF multiple.

If you wish to explore Haivision further I’ve included their most recent investor deck and a recent interview from MS Microcaps hosted by Maj and Nicholas.

Had I reviewed their Q4 it would have been upgrade worthy. But I didn’t and their Q1 here was just enough to maintain a three star review.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Thanks for the review, Wolf. Some decent numbers, but that bonus is pretty disgusting. Staying away.