How time flies! It’s been over two years since my review of Grey Wolf, and you’d think it would have been a more regular occurrence given their ticker.

I first reviewed WOLF back in Jan of 2024 and gave them an encouraging 3.5 stars. The market liked it too sending the stock up 33% within a few trading sessions. A quarter later in April I downgraded them and by August they had lost 40% of their value.

As a result of that downgrade they went into my ignore pile. The Wolf ignoring WOLF has turned out to be a bad idea as the company is up 170% since those August 2024 lows and 74% over the past twelve months.

Looking at their 2025 overall numbers that appears to make sense with a 33% revenue increase and 135% growth in net income. Their $56M valuation has them trading at a 32 P/E, 10.5 EV/EBITDA, 13.5x cash flow but a rather unimpressive 3.3% return on invested capital.

Grey Wolf released their financials after close on Thursday and Friday the stock traded a little better than flat, up a penny or .61% to close at a buck sixty five.

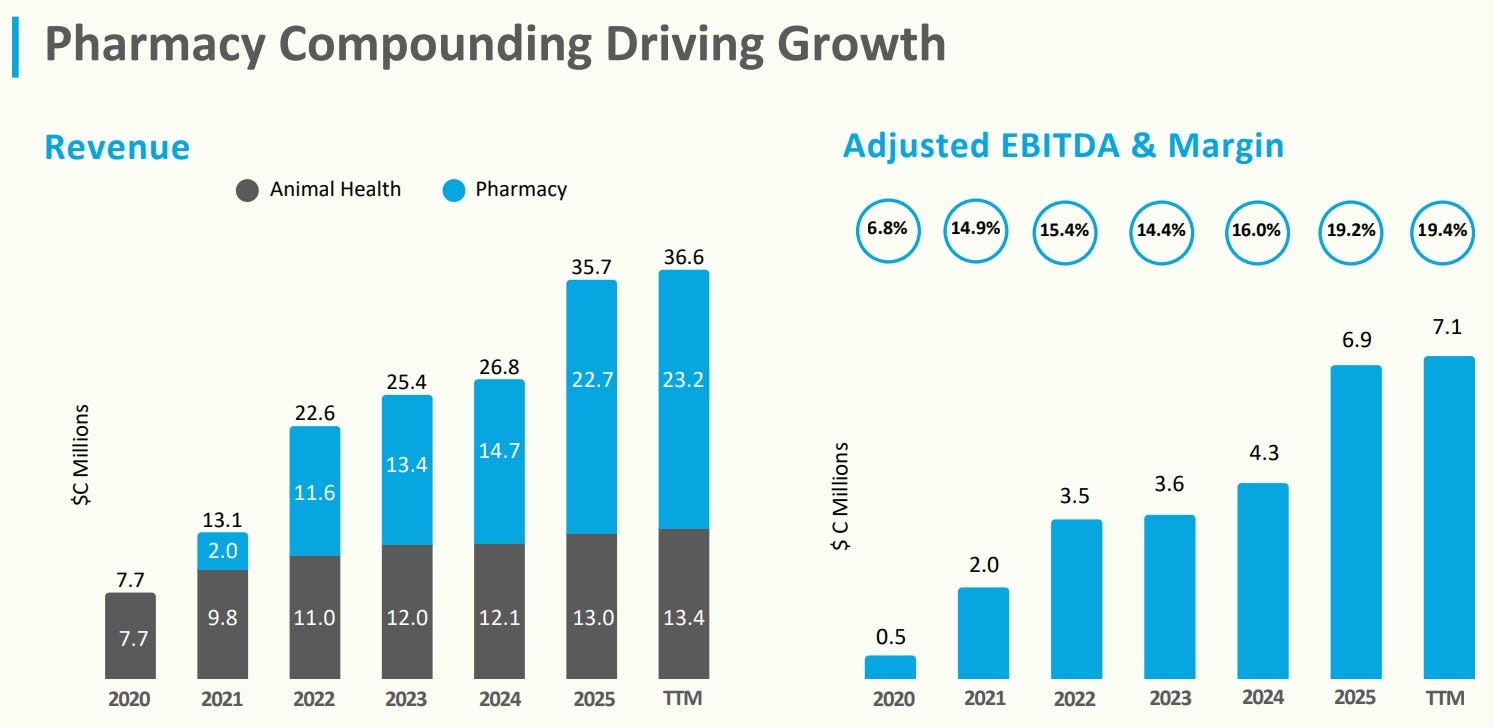

In addition to operating two pharmacies, a 25k sq ft facility in Manitoba and another in Ontario set to expand in 2027 from 10k to 28k square feet, the company also sells, markets and distributes products to veterinary clinics across the country. I’ve linked the entire presentation to the image below to learn more about them. As you can see both of their segments deliver very healthy margins and both had Q1 growth with the pharmacy business up by 5.6% and Animal Health revenue by 13.8%.

Grey Wolf Animal Health has a proposed name change in the works to become Grey Wolf Health as it better recognizes their pharmacy services to both animals and humans.

Let’s dive into their financials and other information to see if there is anything to howl about.

(Free version will be delivered to free subscribers on May 29th)

Balance Sheet:

Grey Wolf possesses a very solid current ratio of over 2.6 that consists of $8.8M in cash, $2M of receivables, $5.3M worth of inventory and $550k in prepaids overtop of just $6.3M of liabilities due over their next twelve months.

Their cash position covers all of those liabilities showing excellent short term liquidity. The company does not provide any detail on their receivables including an aging report but it is down from the end of the year and I couldn’t find any history of large write downs.

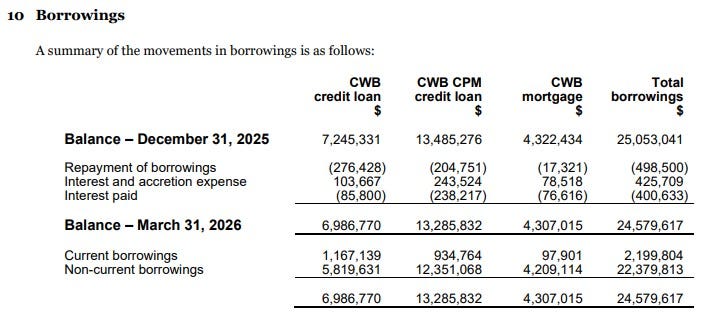

Grey Wolf does have some debt, $24.6M in fact which is a bit of an eye opener given that figure is about 44% of their total market cap.

Unfortunately you have to go back to their annual financials to obtain the details on the above loans. From left to right the first loan is what remains on a $11.5M loan at an attractive 4%. Next is what remains on a $14.3M loan which occurred in November of 2024 to partially fund the CPM acquisition. This loan carries a rate of 7.09% and ends in 2030. The last is a $4.4M five year mortgage used for the land and buildings of the CPM acquisition and carries the same 7.09% rate.

In addition, the company has a $750k untapped line of credit with RBC, and $4.5M in deferred tax liabilities.

Cash Flow:

Grey Wolf achieved $1.53M of operational cash flow in their first quarter of 2026, 45% more than what they achieved in the comparable quarter, notable with very minimal working capital adjustment assistance.

They utilized $127k in the quarter on hard assets, received $249k from option exercises and paid half million worth of debt payments.

Overall, they improved their cash position in the first three months of the year by 14% or $1.1M.

Encouraging so far.

Share Capital:

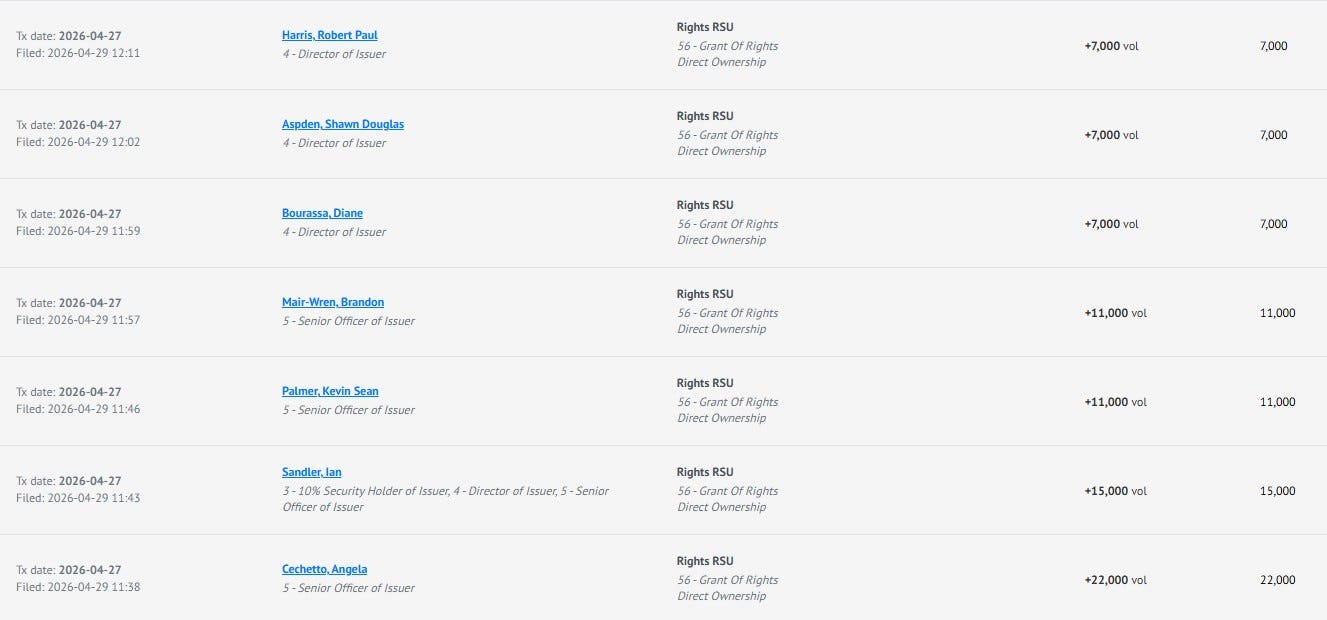

34.5M shares with under 1% dilution in the past year from options being exercised

192k broker warrants expiring in three weeks. They just sit out of the money by two cents at $1.67

2M options outstanding. 1.57M are ITM with none expiring within the next year

Insider and Employee ownership of 24% (per investor deck). Bloom Burton & Co is the largest shareholder owning 10.5%.

Small open market buying by four different insiders last June, but totaling just 58k shares

It’s notable that the company adopted a RSU plan for the first time in May of 2025 (a 10% SBC plan) but gave out their first RSUs last month - a rather negligible amount.

Income Statement:

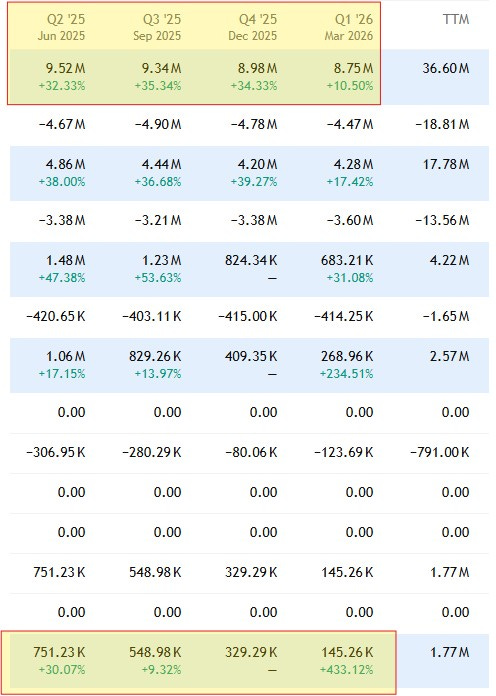

Revenue grew in Q1 to $8.75M, a 10.5% increase over the comparable period. Gross margin improved by 150 basis points to 54.1% which drove higher gross profit dollars by 13.5%.

Total operating expenses grew by 11% at a slightly higher rate than revenue with their two main cash burning buckets, Sales and Marketing and G&A growing by 25% and 13% respectively. That will leave them one segment shy of achieving a Wolf Trifecta in Q1.

Operations Income grew by 31% to $683k or a ratio of 7.8%. Below that line is where their debt becomes a factor as the $438k in interest expense in Q1 makes up 64% of their operating income. After paying 133% more taxes YoY, their net income was $145k, 1.7% of revenue, but over 5x what they achieved in Q1 of last year.

Summary:

I think the 170% increase in valuation over the past twenty or so months has been deserved. But how much upside remains is the big question.

Their pharmacy segment has been the driver of their growth story going over 10x since 2021 on a TTM basis, and 58% since 2024 while the Animal Health segment grew by 11%. Their new Ontario facility will nearly triple that facilities footprint next year which should support further growth.

The company is very quiet in the press release department, only putting out five news releases in the last nine months - three of them earnings calls, therefore it is challenging to be up to speed on what the company is up to.

One of their press releases was in regards to their participation at Smallcap Discoveries last year. I’ve included the presentation below, and maybe that will assist it getting more than the sub 200 views it has currently.

Animal Health and pharmaceutical compounding do not seem like seasonal types of businesses, but it’s notable that WOLF’s revenue and profitability have declined for three straight quarters. They will be up against much more challenging numbers in the quarters ahead without the benefit of their big acquisition they had at the end of 2024 which drove 30%+ growth for four earnings straight.

Their next two quarters represent nearly 75% of their profitability comps, so with a 32 P/E, it feels like a risky time to give Wolf a swing here. They will also be facing some increased costs without the benefit of revenue due to the new buildout of their Ontario facility.

There is some small regret for putting them on my ignore list, perhaps too abruptly a couple of years ago. But these comparables do not make me want to make up for lost time with a position here just yet.

Very watchlist worthy. 3.25 stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.