The cannabis/nutraceutical hybrid. The big swing that hasn’t swung. The nickel humper.

My first review of Glow Lifetech was exactly one year ago after their Q1 of 2025. Then, they were a year removed from a cease trade order for three months for failure to file their annual financials. They have come a long way in that two year span going from some dreadful float management and next to no revenue, to a little over $2M in 2025 via posting 200% revenue increases for five straight quarters. That streak came to an end in Q4 when they posted a measly 53% revenue increase (read that with sarcasm).

A year ago the stock traded at six cents. I awarded them an unimpressive two stars in my first look, in large part due to their warrant overhang. They had 170M shares outstanding with over 70M warrants, 60M of which were ITM at the time. Over this past year the stock is down 17% off that review and currently trading at, you guessed it, a nickel.

November of last year is when I first began talking about a potential swing opportunity, but calling them “dead money” until the March/April timeframe, and the stock has largely traded in the 4.5 - 5.5 cent range since.

I cited three potential catalysts in the April/May timeframe for a potential swing. I felt so good about it that I listed it as a bonus opportunity in my 2026 Wolf Pick article, and yes took an eventual position too. The first catalyst was the last large batch of ITM warrants (40M) from last year, and the last two would be their annual financials and then their Q1 of 2026.

Two of those catalysts have now come and gone. About three quarters of those warrants expired unexercised and while their April year end financials received nearly a full star upgrade to 2.75 stars, the share price has been anchored to that nickel area once again.

While Glow did have some much improved financials and less warrant overhang at the end of 2025, their QoQ financials were very soft for the first time, down 19% despite being better by 53% on a YoY basis. That gave the market some pause, and when you combine that with the fact that most of the sector has been stuck in a quagmire, the nickel hump continued.

Last night the last of those three potential catalysts I’ve been discussing for sometime were released to the market. Are these financials the catalyst to complete that swing, or is it a three strikes and you’re out scenario here?

Balance Sheet:

Some small overall numbers here as one would expect from a $9.6M market cap, but impressive nonetheless with a current ratio of 2.7.

At quarter end they had $1.6M in cash, $570k in A/R, $470k worth of inventory, $150k of prepaids and $160k in loan receivables overtop of just $1.1M in current liabilities. That’s also their total liabilities as the company holds zero debt or long term financial commitments.

It’s both a healthy and liquid balance sheet as just their cash position alone is over 1.5x this years current needs.

Unfortunately the company discloses no aging report to gauge the health of their receivables. The loan receivable mentioned refers to a loan agreement with a subsidiary of one of their largest shareholders (Swiss PharmaCan). The loan is satisfied through royalty payments for MyCell™ products. In addition to the $160k listed in short term assets, an additional $380k sits in long term assets.

Solid start and an improvement YoY from my initial review.

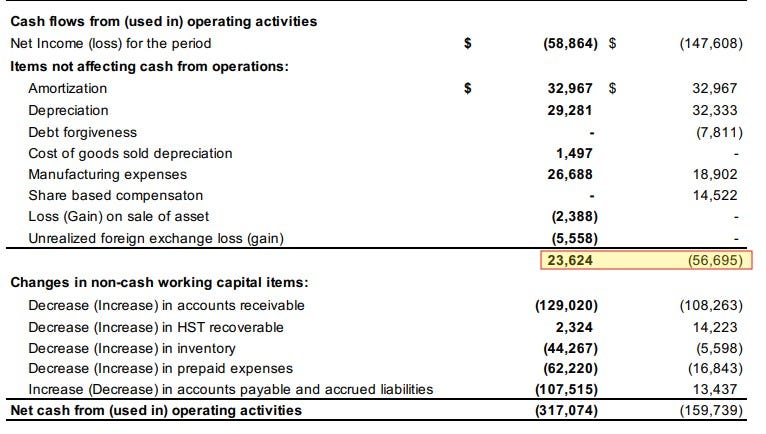

Cash Flow:

Glow was operationally cash flow neutral in 2025 with just $15k of OCF burn in their recent fiscal year. Here in Q1 of ‘26 they experienced operational burn of $317k, approximately double the burn from the comparable quarter.

That burn however is due to working capital adjustments all going the wrong way, increases in A/R and inventory investments, and paying down payables and increasing prepaids.

Prior to working capital adjustments they performed better by $80k. I’m still willing to call them operationally cash flow neutral, as this is more than likely going to balance out in a quarter or two. With that said, I’d still like to see that aging report.

Share Capital:

192.2M shares outstanding, representing 13% dilution over the past year and 6% in just Q1 due to the near 11M warrants recently exercised

11.3M options outstanding with over 5M expiring unexercised in Q1, unsurprising at 30 cents. 4.5M sit on the bubble at five cents but do not expire until Sept 2029

8.9M warrants expiring this week at seven cents, most likely expiring unexercised unless something crazy happens this week

Insider ownership listed at 28% per the company investor deck

Modest insider buying in the open market but both insiders and their top shareholder (UK based Nova Capital) have been exercising warrants at the current share price)

Income Statement:

Glow Lifetech set a new quarterly revenue record with $643k in Q1, 35% better than a year ago. Gross margins declined by 230 basis points from 66.5% to 64.2%, but still a very healthy margin in this sector and that resulted in 30% more gross profit on those 35% more sales.

Glow achieved some very healthy operational leverage in the quarter with total expenses rising by only 4%, well under the rate of revenue and GP improvements.

That all translates to cutting their operational losses by more than half. After a few minor birdies to last year below the operational income line, their total net loss was $59k, a 60% improvement over a year ago.

Summary:

Some solid improvement, and a much improved company from when I looked at them first one year ago. Revenue is moving in the right direction again after a hiccup last quarter, they have very sexy margins, run operationally lean and their cap table is cleaned up and more attractive than it has ever been.

The CEO also bats above his weight relative to the company’s market cap. For more on him, here is a recent interview from last week hosted by Smallcap Discoveries Paul Andreola.

But did Glow Lifetech do enough in this quarter (my last of three spring catalysts) to move the stock away from a nickel and give them a re-rate above their current $9.6M market cap?

I hate to say it as someone who has been holding a swing position for the last few months, but I don’t think so.

If you have been following Glow for sometime, you are aware of this chart that they have been using quarterly for sometime. It shows the number of distribution points (sku’s x locations) along side their quarterly revenue totals. The comparison of their distribution points vs their revenue may be starting to show some stagnation. That previous Q3 revenue record still looms large as this recent quarter only exceeded it by 2% with over 1000 more “distribution points”.

(The full investor deck is attached to the image below)

While Glow isn’t your typical cannabis play as they expand into nutraceutical verticals, the best comps we have are in the Canadian cannabis sector. When you look at those comparables, I think it is hard to make the case that Glow should be valued significantly higher than the multiples it trades at today.

Glow trades around 4.5x revenue, but on a TTM basis has yet to turn a profit on the Net Income or EBITDA lines. Looking at three other sector plays I’ve covered heavily in the past (LOVE/ROMJ/XLY), none trade higher than a 1.5x P/S ratio.

Auxly Cannabis (XLY), who’s management team I couldn’t trust as far as I could throw them are one of those that trade at 1.5x revenue. They also put over 20% of each revenue dollar on the net income line and trade at under a 7 P/E ratio. If they have traded flat over the last eleven months, it’s hard to make the case for significant share appreciation here.

So despite an upgrade to three stars to these financials, when it comes to my three spring catalysts for a great swing opportunity - I’m ringing them up on a called strike three. Get that nickel some KY jelly for some additional humping.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

my new term for all cannabis companies canibust :)