This will be my first full coverage of Dirtt Environmental via requests from the Wolf Den discord, but it’s far from the first time I’ve talked about them.

The first was after sitting through their presentation in Las Vegas last spring. It showed some positive guidance and some flashy numbers. Unfortunately I found their presentation lacking something. No meat.

This was my summary of what I had to say in that April conference recap.

Then, in July I previewed their earnings, and had this to say:

The stock tumbled by 27% over the next month after dropping a “Dirtt Snake” on the market.

Over a one year period the stock is essentially flat. Today is a new day however, and time to look at them with a fresh set of eyes.

Naked Eyes if you will.

Let’s see if it’s time for DRT to rise from up the “dirt”

(All figured in USD unless otherwise specified)

Balance Sheet:

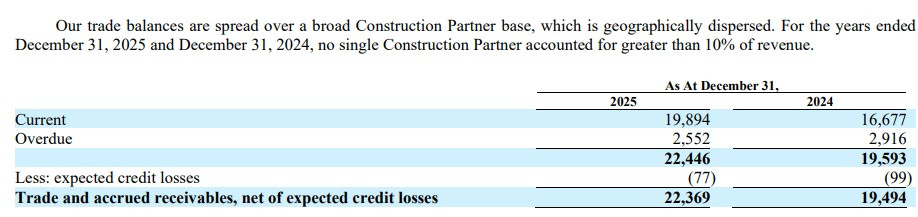

A barely satisfactory current ratio of 1.1 that consists of $20.6M in cash and restricted funds ($250k), $22.4M of receivables, $15.8M worth of inventory and $3.7M in other short term assets over top of $56.7M in liabilities due throughout their 2026 fiscal calendar.

No traditional aging report was provided but 89% current, along with very limited anticipated losses look more than acceptable. I’d still like to know how overdue the aged portion is however.

At year end, DRT had $23.2M worth of debt mainly in the form of convertible debentures. All were current as they expired at the end of January and August. Unsurprisingly since the January debentures converted at over 4x the current share price ($4.06), the principal of $12.1M was paid post financials.

That leaves $10.8M expiring at the end of August with a conversion of $3.64 (CAD) per share.

Post financials they received a $5.5M loan (CAD) from the BDC of an allowable $15M.

It’s a lot of bouncing balls after these financials so their Q1 in May it will be important to re-assess where they stand.

Cash Flow:

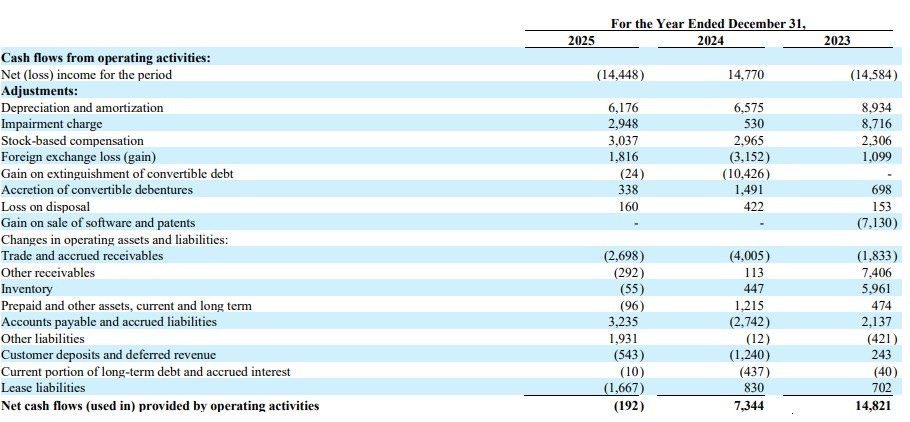

Let’s be generous and call their 2025 operational cash flow as neutral. The final results show operational burn of $192k for the entire fiscal year. By comparison it’s a very disturbing three year trend of $14.8M in OCF in 2023, achieving less than half of that total in 2024, and then moving to slightly negative this past year.

Not great news when their liquidity looked questionable at year end and they began tapping into their debt facility in February.

Dirtt also spend a net of $3.7M in asset spending during the year, and repurchased $4.4M shares. Overall their total cash position depleted by 30% during 2025.

Share Capital:

191.9M shares outstanding, which is 1.7M less shares outstanding than last year but 82% dilution over a two year period

Purchased 5.8M of shares under their NCIB

209k warrants expiring this year that are so far out of the money they aren’t worth discussion

8.2M RSU’s, 2.6M PSU’s and 3.5M DSU’s outstanding. 3.5M vested combined in 2025 and 3M additional were granted.

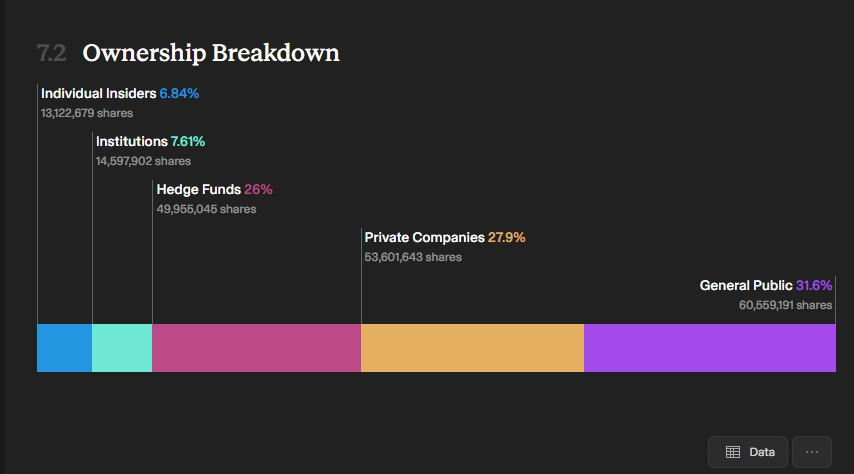

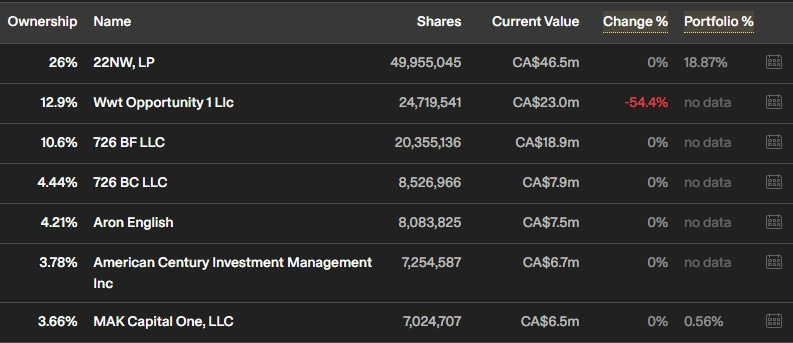

Ownership breakdown below with under 1/3rd held by retail (per SimplyWallSt)

Income Statement:

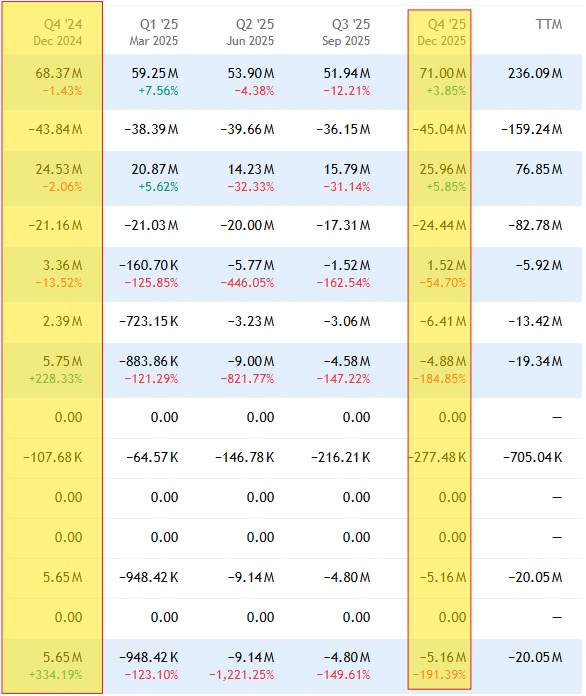

Revenue decreased by 3.1% during 2025 to $168.9M, down from $174.3M. That is after a 4.2% drop the previous year from $181.9M. That revenue decline came after an across the board 5% hike on all orders in the final three quarters of the year. The company’s three year revenue history is shown below:

The story isn’t better on the margin line which decreased by over 400 basis points to 32.8%, so on 3.1% less revenue, contributed 13.9% less gross profit dollars. To complete the reverse Wolf Trifecta, operating expenses increased by over $6.5M or 11% more than 2024. $3.8M of those additional expenses to the year prior did come from reorganizational costs. As you can see below, reverse Trifecta’s make for an unhappy Wolf.

All the above contributed to a $29M turnaround to the negative on the net income line, putting them as a similar loss as what they occurred in 2023 on 7.2% less business than they generated two years ago.

To be fair to DRT, tariffs on aluminum have been a significant impact to them. The bad news is there isn’t much light at the end of the tunnel regarding resolution.

Overall:

So after all of that, the stock is up over 10% since they dropped these financials and are up by 39% since their 52 week low experienced in September.

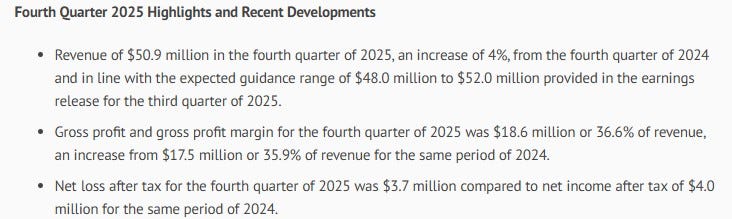

I’ll be honest, I don’t get it. Part of the reason may be that Q4 trended much better than the rest of the year on the revenue line and they also posted much stronger gross margin.

But those numbers still resulted in a near $11M (CAD) turnaround to the negative on the net income line, losing $5.2M (CAD).

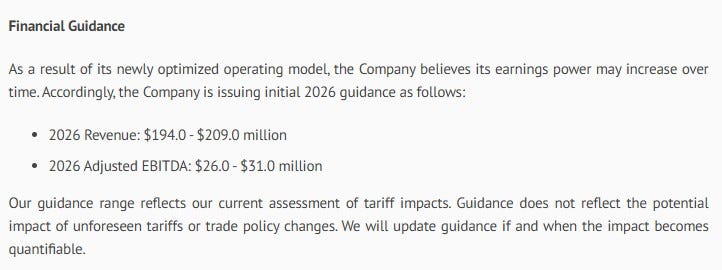

Another reason for investors to be encouraged is their 2026 guidance. The bottom end of that guidance represents a 15% increase over last year. While they give bottom line guidance, I don’t put any stock in AEBITDA numbers. In addition, the last time I heard them give 15% revenue guidance was back in April in Las Vegas, and they delivered -3.1%.

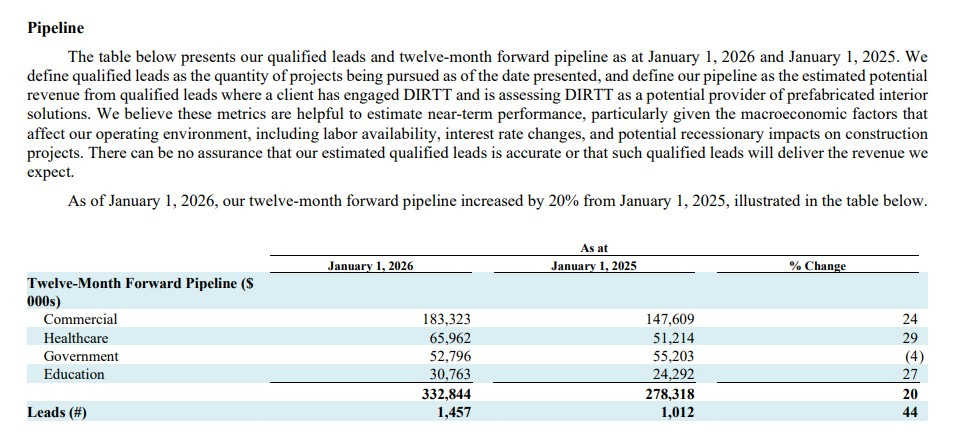

Pipeline? Sure the sales pipeline is up, but that is about as useful as a one legged man in an ass kicking contest. Poor sales people have too much of an easy time manipulating their sales pipeline. I’m not suggesting that is the quality of Dirtt’s sales team, but their two year track record isn’t great and I’ve seen this game before. It looks great in your CRM software though.

The company touts a strong balance sheet. It’s really not. I also highly question management’s decision to buy back as many shares as they did in 2025 given the mediocrity of their cash position. To top it off, they basically replaced shares repurchased with free shares to insiders via their SBC plan. Given their two year performance, that feels undeserving.

You made me promises (promises), promises

Knowing I'd believe

Promises (promises), promises

I knew you'd never keep

Now they’re back with more. I’m passing (again).

2.75 stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Thanks for the review, Wolf...and the YouTube video.

Thanks Wolf the details are fantastic. Keep it up and appreciate the frequency and quality of these reviews. Your are right 39% in 52 weeks is a decent return,