What a great story D-Box has been over the last five quarters. In February of last year, I gave the company my Wolf Seal of Approval, my first in what would become a new way of announcing my mid-year Wolf Picks. The stock traded at $0.145 then and yesterday leading into these financials, the stock closed at $0.90 for a 521% return.

My conviction has only grown since then with multiple buy zones along the way, including in my recent May What’s Wolf Watching article. Within that piece I noted that DBO would be up against a very soft comp setting them up for a pretty good top and bottom line beat, also noting I would be a buyer at any dip into the 80-85 cent area. That opportunity arose last week touching the bottom of that buy zone at 80 cents and I and others within the Wolf Den Discord acted upon it.

You may have noticed many of my reviews of late have been a bit of a bummer with many of those covered missing expectations. Therefore I was very much looking forward to after hours yesterday. The highlights look excellent, supporting my thesis of a great quarter to close out the year on both ends of the P&L. Revenue was up 70% with net income up by 162%.

Let’s get into the weeds to ensure we do not come across any landmines. Grab yourself a comfy D-Box seat, and come along for a ride to see if we can determine where D-Box goes next.

* Free subscriber release on June 9th.

Balance Sheet:

DBO boasts a very clean and healthy balance sheet. They have a current ratio of over 4.1 consisting of $17.6M in cash, $8.4M in receivables, $6.2M worth of inventory and $1M in other short term assets. All of that is overtop of just $8M in short term liability commitments (deferred revenue removed).

They are very liquid with just their current cash position covering their next year’s financial commitments by a factor of more than 2x.

D-Box’s A/R appears healthy but I will note that they do not provide a traditional aging report. In note 17.2 they do add that three clients make up 43% of all money’s owed, and receivables over 90 days stood at 8%. About half of that amount ($324k) is booked as an allowance for doubtful accounts. The company has only written off $68k in the last two year.

They are also virtually debt free with a small Canada Economic Development loan at 4% with $323k remaining and will be extinguished by December of 2027.

This is about as solid of a start that one could hope for.

Cash Flow:

DBO generated $12M of operational cash flow during their fiscal 2026, 61% more than they generated a year ago. Q4, due to working capital adjustments came in at a similar $2M of OCF on a YoY basis.

Through the year they invested $1M in assets, paid down $900k of debt and had $100k flow into the treasury from exercised options.

Overall the company improved their cash position by 125% from the start of their fiscal year.

A short cash flow section is typically a good cash flow section. That is the case here.

Share Capital:

222.8M shares outstanding with just 0.3% dilution over the past year

NCIB to buy back up to 10% of shares announced a week before year end, with 173k re-purchased and cancelled. Approximately 580k bought back and scheduled to be cancelled since year end

13M all ITM options outstanding under the company’s 10% plan - none expire for another 2.5 years

425k SAR’s (Share Appreciation Rights) and 1.4M RSU’s

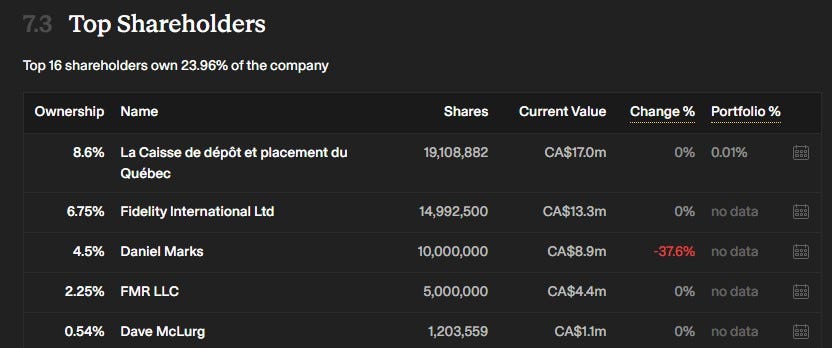

6% insider ownership with 16% owned by institutions. Top five per SimplyWallSt shown below

Mixture of insider buying and selling with the audit chair and largest insider, reducing his holdings by 38% over the past year

Income Statement:

Total revenues for 2026 totaled $57.6M, up 35% over last year. Gross margin improved on the year by 60 basis points to 52.8% and gross profit dollars improved by 36%.

Controllable operating expenses (forex losses removed) only grew by 8.3% while generating 35% more revenue showing exceptional operating leverage. This included a reduction in marketing spend by 11.7%. Admin and R&D costs rose by 21% and 20% respectively.

On the year, that awards them the Wolf Trifecta, for generating significant revenue wins, improving margin, and excellent expense control.

Wolf Trifecta’s add up to improvements in profitability. After also reducing financing expenses by 98% YoY, profit before income tax nearly tripled from $3.88M to $11.36M.

D-Box also had the luxury of carrying forward some tax losses in 2026, adding an additional $6.1M to the net income line and increasing their total profitability by over 350% YoY.

On a YoY comparison basis, Q4 revenues were the best performing quarter of 2026, rising to $14.65M, up 70%. That did however come at the expense of some gross margin with the rate eroding by nearly 600 basis points to 48.3%, and the only quarter of the year to slip under the 50% mark.

That was driven by revenue mix with much softer Sim revenue which carries higher margins. Theatrical revenue on the other hand was up by nearly 8x, but it also carries a lower rate. Despite this, gross profit dollars were still up by over 50% in Q4.

While not as strong as the total year, DBO still converted well on operating expenses with their three main buckets increasing by 31%, R&D spending rose by 12%, Sales & Marketing costs rose by 21%, and due to $500k of additional SBC costs, Admin expenses rose by 57%.

That all combined to drive $1.89M in net income vs $0.72M last year and increase of 162%. They fall shy of a Wolf Trifecta in the quarter, but more than made up for it during the rest of the year.

Summary:

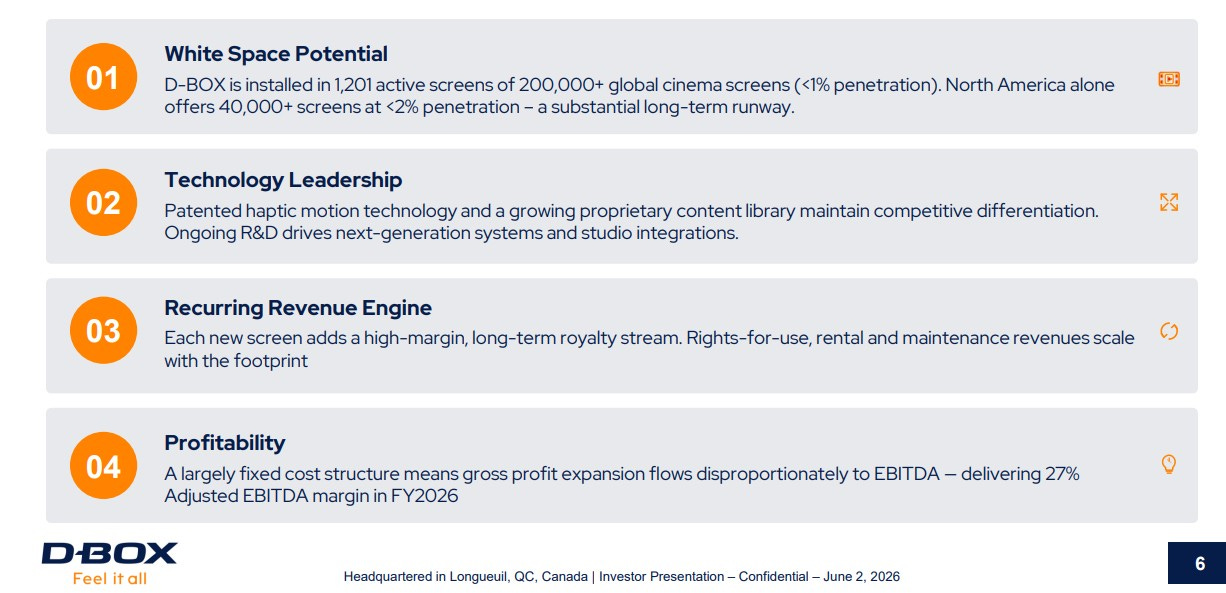

Overall this was a very transformational year or past five quarters for the company. They increased their net number of screens by 18% during the year while growing their royalty revenue by 36% and theatrical system sales by 133%.

Their sim racing and sim training businesses were both down by double digits and still make up 28% of total revenues. While this segment will be much lumpier than the others, it’s still large enough a factor to sway quarterly results.

But the future of DBO will rest with their theatrical business driving installs and the very important royalty revenue that generates going forward. With 66 net new screens added in Q4, that sets up their royalty revenues very well for next few quarters. They are also only present in less than 2% of North American screens and under 1% globally, giving them huge potential for the next number of years. Even on a comp basis, theatres are expecting solid growth over the next year with greater emphasis on premium experiences which sets D-Box up well.

So how do we price D-Box, particularly considering the $6M+ birdie in income taxes this year?

At $0.90, DBO sits at a $200M market cap with their valuation ratios as follows - an 11.5 P/E, 13x Adjusted EBITDA and 16.6x Cash flow. It’s unusual to see a P/E ratio lower than the others and that is due to the tax benefits experienced in 2026.

This past year won’t be the only time the company recognizes some deferred tax benefits as they have $6.4M and additional federal and provincial R&D expenditures to recognize for years to come.

Even with that I don’t think the 11.5 P/E is a great metric here. Without the tax benefits in ‘26 their P/E would stand at 17.6. That feels fair for what they are doing today, and then investors need to price in all of that white space potential. Can they get 2% global screen penetration in the next few years? That would be 4,000 screens and they have 1,200 today. That would be 3.5x their performance today. Feels doable.

Is DBO dollar bound today? I think they should be. Let’s see what transpires. Maintaining 4.5 stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.