As I mentioned in my recent WWW article in regards to Covalon, what a difference a year makes.

My last full review of Covalon was over a year ago for their 2024 annual filings, one that received an upgrade to 3.5 stars. After that positive review came three straight poor quarterly results dropped to the market. As a result, the stock dropped like a bad habit - 38% over the past year and 60% from their highs above $4 just fifteen months ago. That’s quite the pecuniary impact to the wallet for longs.

In my Feb WWW article, I had predicted another big miss for these upcoming financials due to the very tough comps they would be up against. My initial look at their numbers released this morning confirmed those fears.

But I also suggested that they could be one to re-evaluate once these numbers were out, and see where the dust settles. So let’s do just that.

Paid Subscriber Benefits:

First access to annual picks, upgrades and mid year “Seal of Approval” picks.

Monthly “What’s Wolf Watching” preview of upcoming earnings and potential market moves.

FinsDontLie Scholastic Series - exclusive educational posts

Access to The Wolf Den Discord community (daily insights, charts, chat & Q&A)

Balance Sheet:

While Covalon’s YoY results have struggled over the past year, their balance sheet remains extremely strong with a current ratio of 5.7. That consists of $17.9M in cash, $2.2M in receivables, $6.8M worth of inventory and $860k in prepaids overtop of just $4.3M in liabilities due over the next year (deferred revenues removed).

Huge collection quarter within their A/R which will temporarily boost cash flows also.

Liquidity is phenomenal with their cash position alone covering their short term commitments by well over 4x. They are also debt free.

Cash Flow:

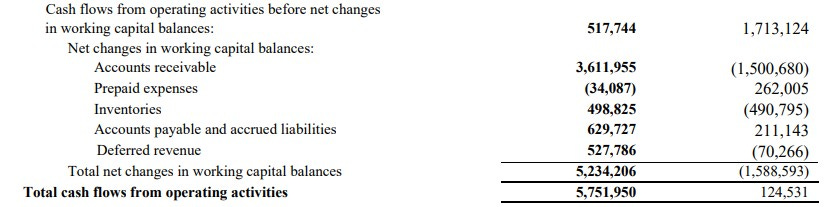

Massive operational cash flows in the quarter with over $5.75M generated in Q1, which is over 46x more than they generated in the comparable quarter.

BUT, investors really need to take this quarter with a grain of salt here as it was all heavily impacted by working capital adjustments.

Prior to working capital adjustments, cash flows were actually down 70%. Sometimes when your revenue is soft and you have an excellent collections quarter a company’s OCF can be exaggerated and I’m suggesting that is the case here.

Covalon utilized over $700k in asset purchases in the quarter and paid out over $4.1M in one time dividends. Despite those large cash outflows, their net cash position still increased by 3% in their first quarter.

Share Capital:

27.6M shares outstanding, under 1% dilution occurring in the past year from vesting DSU’s in a historically well managed float

200k warrants expiring in 2026 that are well out of the money at $4

1.4M options outstanding with only 800k ITM at $1.50

80k DSU’s

47% insider ownership (per Yahoo Finance) but no insider activity on the open market to speak of

Income Statement:

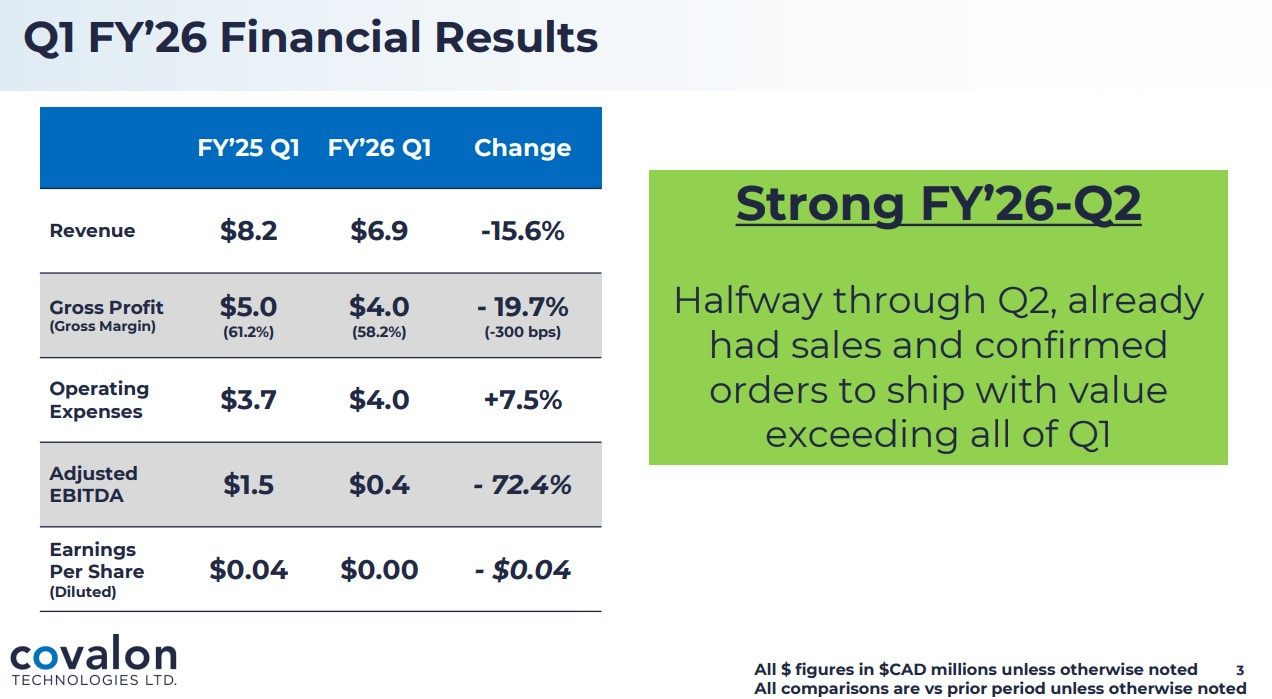

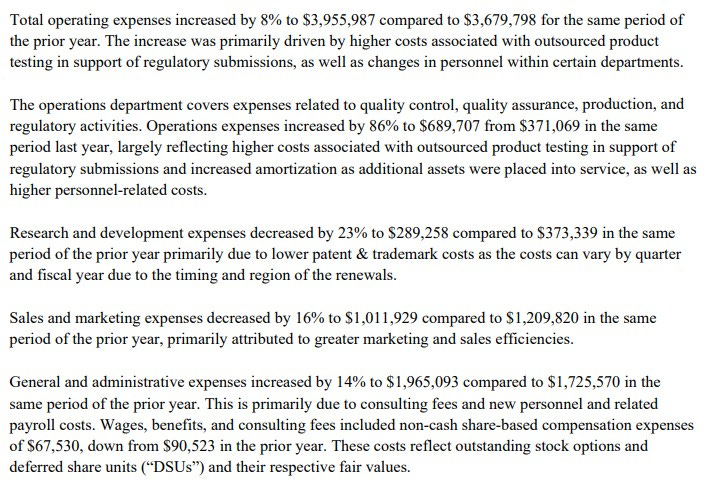

Here is where things get rough and we start with $6.9M in revenue, down 15.6% from Q1 of last year. Margins also suffered decreasing by 300 basis points from 61.2% down to 58.2%. That resulted in 20% less dollars delivered to the gross profit line.

To add insult to injury, and to complete the reverse Wolf Trifecta, total expenses rose by 7.5% with a 14% increase in G&A and an 86% increase in “operating” costs while R&D spending decreased by 22.5% and Sales and Marketing costs were 16% lower.

That all resulted in a 90% decrease in net income to $125k from $1.2M in the comparable quarter.

Overall:

Now that I’ve brought you those numbers, you may be surprised if I told you the stock is currently up 12% as we near the mid way point of the trading day on better than average volume.

These results have sent their P/E ratio from 21 yesterday to 51 today as their TTM net income was cut by more than half, coupled with today’s rise in share price.

Unfortunately I was unable to listen in to the conference call, but from their slides they are suggesting by the mid way point of Q2 they have already surpassed Q1’s revenue. That sets them up for a very good beat as they are up against just $7.6M and have already achieved $8.2M or more.

That does show some encouraging signs regarding the top line, but I’m not seeing much in relation to their margin, nor their opex. The commentary within their MD&A didn’t bring me a lot of comfort either.

On a 51 P/E based on their trailing twelve months, that requires a lot more revenue to justify the current market cap if better margins or more operational leverage isn’t found. On the other hand their market cap is less than 3x their current cash on hand. That does present a lot of flexibility to Covalon, so I would not be surprised if the right acquisition opportunity came around.

Bottom line is that dip I was hoping for has not occurred. That leaves me currently uninterested in today’s valuation. Maybe the conference call was just that good. Will stay on the watchlist.

3.25 stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.