Before we dive into the review, the last few weeks have seen few bright spots the microcap space but Cematrix has certainly been one of them. Another occurred yesterday as iFabric 2026 Wolf Pick gained 39% yesterday increasing the return to 105% since the pick announcement.

Of 20 annual Wolf Picks, they become number 12 to AT LEAST double. Is a 60% double rate any good?

IFabric joins (multiples at peak)

Class of 2023:

Happy Belly Food Group 23x

Atlas Engineered Products 2x

KITS Eyecare 8x

Trubar 7x

2024:

Enterprise Group 3x

Kraken Robotics 15x

NTG Clarity 19x

Gatekeeper Systems 7x

2025:

ZoomD Technologies 3x

MTL Cannabis 4x

2026

PUDO Inc. 2x

List doesn’t include mid year pick DBox Tech 6x, nor the other three 2026 picks, just three months old that I still have high hopes for.

Back to regularly scheduled programming. Thanks for allowing the personal horn toot.

Cematrix has been on a one year heater now. If you were paying attention when I wrote my “What’s Wolf Watching” article back in March of last year, I identified a buy zone below to watch for after their previous annual earnings in the 15-17 cent area.

After a couple of brief dips into that buy zone, anyone acting upon that would be up 185% from the top of that buy zone with the stock closing at $0.47 yesterday.

The stock made a strong move leading into their 2025 annual earnings release, then dropped over the next three trading sessions last week, only to rise back up by 12% in yesterday’s action to close a new 52 week high.

Is there any rationale for the yo-yo price action within the financials, or is the stock poised to close that old gap from July of 2024 to fifty cents soon? Can they improve upon the 3.5 star rating from Q3?

Let’s dive in.

Balance Sheet:

Cematrix’s balance sheet just continues to get stronger with each review, improving on the current ratio of 3.8 one quarter ago to over 6.5 currently. That consists of $11.9M in cash, $11.7M of receivables, $1M worth of inventory and $450k in prepaid expenses over top of only $3.8M in current liabilities due across their 2026 fiscal year.

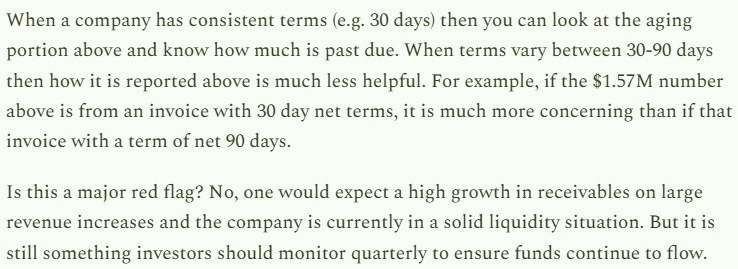

$2.3M of the company’s receivables are within holdbacks, and the aging for the remainder is below.

I certainly have seen cleaner aging statements. The company’s credit terms vary between 30-90 days, and there is no distinction in the above table of what is current and what is overdue. Over 90 days is 19% of trade receivables which is definitely higher than you would want to see it. Cematrix is already planning to book a $239k credit loss compared to $111k a year ago.

It is important to point out that their trade receivables did in fact improve by 28% in the quarter, but their over 90 days have increased by 15%.

This is not the first time I’ve discussed the company’s aging report. Here’s what I said after their Q3:

CEMX does have $1.27M of debt within a equipment finance loan and $945k of that is long term at a current rate of 7.7%. They also have an $8M credit facility available at prime + 1.25%.

Overall, quite a good start to the review despite the minor concern within their receivables that investors should monitor in upcoming financials.

Cash Flow:

Operational cash flow (OCF) achieved in 2025 totaled $3.8M, but that figure is off by over $1M or 22% from last year.

The variance in the YoY cash flows comes back to (you guessed it), receivables.

The good news for investors is their Q4 OCF of nearly $3M made up 77% of their annual totals, and in their earnings release stated most of their working capital issues post financials have been resolved.

Cematrix also utilized $600k in investing activities, mainly in equipment. They also added $165k of net debt, repurchased $419k of stock and incurred $337k of interest costs.

Overall, the company’s cash position improved by 16% during 2025.

Share Capital:

149.7M shares outstanding, about 700k less shares from a year ago

1.3M shares cancelled through buybacks in 2025. NCIB expires April 16

8.2M warrants, all currently out of the money at $0.58

5.6M options outstanding, at least 4.65M are ITM but none expire for nearly two years

2.9M RSU’s including 1.3M granted and 540k exercised in 2025. 360k additional RSU’s have been awarded post financials.

Fully diluted float including ITM awards is approximately 158.2M representing about 6% in future dilutionary measures

Minimal insider ownership of 3.5% with 4.5% owned by institutions

No insider activity on the open market since June of last year

Income Statement:

Total revenue for the year was $45.1M, and that is up 27.5% from the $35.4M they achieved in 2024. A pretty impressive end to the year after they began the fiscal year with a 21% decrease in their first quarter. Perhaps even more impressive is what they achieved within their gross margins. Those increased by 850 basis points from 26.6% to over 35%. Therefore, on 27.5% more revenue, they generated 68% more gross profit dollars from $9.4M to $15.8M.

Total operating expenses only increased by 12.5% showing excellent operational leverage on all those gross profit dollars. This is a true definition of a Wolf Trifecta showing double digit revenue growth, significant margin improvements and operational leverage.

Income after taxes soared to $4.1M as a result compared to $270k last year for a 15x improvement in profitability.

It’s really difficult to do any better than what Cematrix achieved in 2025.

Overall:

You have to take your hat off to the management team for a great year and totally deserving of the 185% share price appreciation since they delivered their 2024 results.

So what’s next?

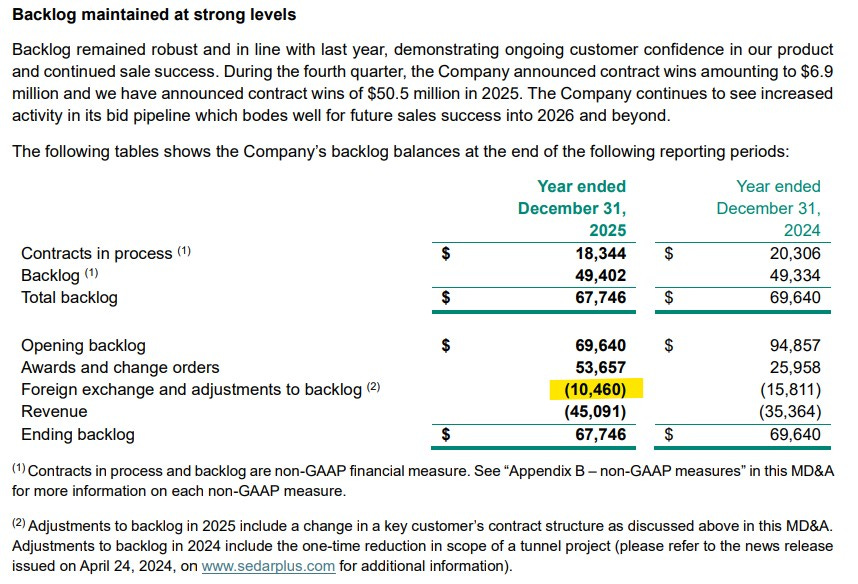

Backlog is a little worse than flat to where they stood a year ago, and unfortunately the company does not provide any forward looking guidance.

Astute investors would have picked up on a couple of items within the MD&A as it relates to their backlog numbers. The first is their contracts in progress is about 10% less than where it stood at this time in 2024. With Q1 being historically the softest quarter for Cematrix and their only poor quarter of 2025, does this suggest a soft upcoming quarter on soft comps? It’s hard to say for sure but what little evidence we have creates that potential.

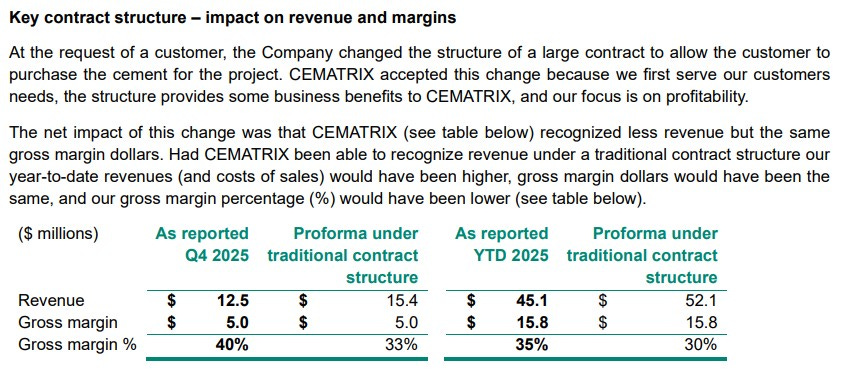

The other item was the adjustments to their backlog which was a contract adjustment to allow their customer to purchase their own cement. The negative is a reduction in revenues with the positive upside of higher overall margins.

Valuation wise the company sits at a $70M market cap with a 15.8 P/E and an EV/EBITDA of 8.2

It feels like it’s currently pretty close to being priced appropriately given the stagnant backlog, and lack of colour from management on guidance.

Given the company’s excellent balance sheet and cash position which only got better post financials, it will be interesting to watch what the company does which could include renewing their NCIB next month. They always look like a prime acquisition target too.

It feels like a solid hold and worthy of an upgrade to 3.75 stars. I would have given it four had the valuation scream a lot more room or some stronger bullish language within their 2026 outlook.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

thanks for the review ! I am curious about this one in the near future, no buy for me at the moment : RSU, no insider activity (only 3,5% insider ownership), lagging backlog w no clear management guidance does not make me feel comfortable.

Seems indeed priced at fair value.

Thanks for the review, Wolf. Appreciate seeing hope and optimism for a company, which seems rare these days.