What a massive change in sentiment since I did their Q1 review. From that 3.75 star review back in July, the stock ran from 47.5 cents to reach a high of $1.95 in early October, a staggering 311% increase or four bagger in less than three months. It did look for a while that it was peaking too fast, too soon and it is now down 35% from that high closing yesterday at $1.26, and also has dropped from it’s Q2 financials release from a couple of weeks ago.

Is this a dip opportunity or has the market finally have this one priced just about right?

Balance Sheet:

We begin with a current ratio of just 1.04 that consists of $658k in cash, $721k in receivables and $1.6M in prepaids against $2.88M in current liabilities. However, their is nearly $1.5M in share purchase warrants listed in here. I’ll discuss this more when we get to the income statement side, but with this removed their current ration and liquidity look better. The company holds no long term debt but does owe $590k in a related party loan (Omni-Lite) which is current.

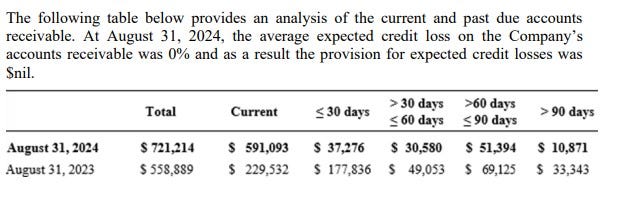

Aging of receivables was a bit of an issue during my last review. While the overall number is up which is understandable given their revenue performance, the aging has improved with 82% being current, much better than the 59% it was at last quarter.

Cash Flow:

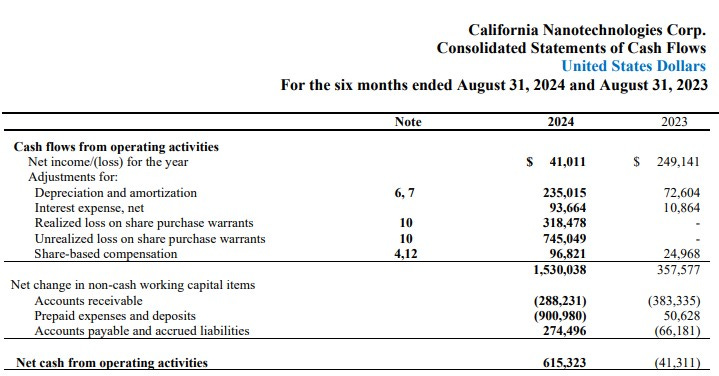

After burning nearly $300k in operational cash flow, they produced $900k of positive OCF bringing their YTD total to $615 in positive OCF compared to burning $41k through the midway point of their fiscal year. This also includes $1.2M of negative working capital changes due to their A/R (understandable) and $900k in prepaids (odd given their cash situation).

CNO paid down $400k of their related party loans, received $200k from warrants and have purchased $420k of assets so far this year. Overall their cash position has depleted by 22% during their first six months.

Share Capital:

42.9M shares outstanding, slightly higher than at their year end due to 1.1M warrants being exercised causing 2.6% dilution

2.8M warrants all well ITM at .25, expiring in October '25 and will bring in $900k to the treasury before then.

5.5M options, all ITM including the 83 cent options awarded this year

33% insider ownership and 39% institutional (per Yahoo Finance), but there has been no insider activity in the open market in some time not including Omni-Lite’s dumping of shares

Income Statement:

Strong top line with 122% growth in the quarter to $1.52M and 173% YTD with $3.27M. Amazing gross profit in the quarter at 82.4% and 73.5% through their first six months. Not getting a lot of conversion within their expenses which grew by 137% YTD, particularly in payroll which has grown by 154%, but even with that they nearly 4x’d their income from operations to $1.18M against $306k on a YTD basis.

Underneath that is where some investors are going to get concerned with a more than doubling of interest expense to $126k, and $1.06M of one time items relating to losses on warrants. It’s important to note however that these are non cash burning and really is a victim of their own share price success here.

Overall:

The one time items due to the warrants have killed a pretty good overall story here. The funny thing is now with the share price retreat, it will actually help their Q3 P&L if the share price is less than $1.58 by the end of November.

I do feel that the share price moved too hard, too fast. Their TTM revenue of $7.4M puts it at a near 8x revenue multiple and even with the non cash burning warrant hits removed, your looking at a P/E near 26, so not exactly cheap. Unless they can diversify their customer base they are also under continuous risk with 74% of their YTD business coming from two customers and and 73% of their Q2 business from a single customer.

While I don’t believe investors should punish the company for the one time items hitting their P&L, $1.95 back in October was absolutely ridiculous and I’m not sure the $1.20 it is currently trading at today is an attractive enough price for me to pull the trigger. Slight downgrade to 3.25 stars.

Have a request to review a stock you are interested in?

Paid subscribers have priority access to request financial reviews of stocks they have interest in. Request via subscriber chat, DM or email at thewolf@wolfofoakville.com

Chat with me and 3000+ other members daily in the TSA Discord.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

CNO repaid all the remaining debt of 600k this morning. Looks like a positive to me worth an upgrade!