BLM released their first quarter of the new fiscal year on Wednesday evening. Revenues increased by 45%, yet the stock was down by as much as 15% over the next two trading sessions. I had this to say in my monthly WWW earnings preview article almost two weeks ago. (The first paragraph is in reference to their 2025 full year earnings)

The share price is up over the past year by 33% however, but 30% off of their high from last May.

I haven’t fully reviewed BLM since this time last year when they were awarded three out of five stars. Now that the dust has settled, let’s take a look to see if they are worthy of more than just a watchlist candidate.

Balance Sheet:

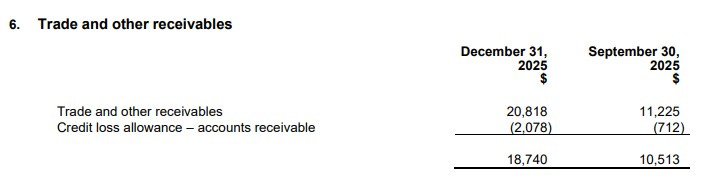

BluMetric ended Q1 with a current ratio of 1.45. The ratio is acceptable but it does bring their liquidity into question being comprised of just $1.8M in cash, $18.7M worth of receivables, and $13.6M in other short term assets including $600k in “due from related parties”. Those come overtop of $23.4M in short term liability commitments including $15.3M in trade payables.

The company’s accounts receivables account for 55% of their current assets and are are up by 78% or $8.2M in the past three months. Almost all of that increase is related to the A/R on the books from the acquisition of DS consultants completed a few weeks prior to quarter end. The company does not provide an aging report for their receivables, but what we can gleam from the financial notes is to expect credit losses amounting to $2.08M. This also stems from the DS Consultant acquisition, and without additional disclosures it does make me question the quality of these remaining receivables.

BluMetric has no traditional long term debt but does have $6M in contingent considerations relating back to the acquisition, for which $3.16M is current. BLM also has a $4M credit facility available to them and I would not be surprised if they needed to tap into that in the short term.

Cash Flow:

Not a great start to the year with $1.8M of operational cash burn compared to generating $838k of positive cash flow a year ago.

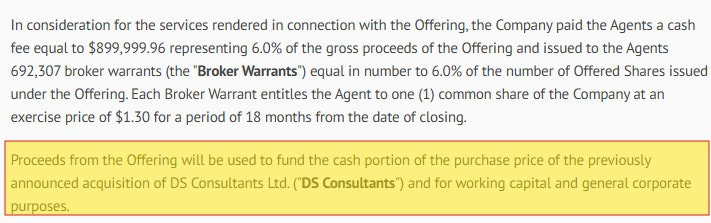

They also spent $10.5M of cash on the DS acquisition which was funded by the $12.5M raise at the same time.

Overall, their cash position depleted by 16% during the quarter.

Share Capital:

54.5M shares outstanding, 48% dilution during the past year and 71% over the past five quarters. 16.8M additional shares are directly related to the DS Consultants acquisition

950k warrants outstanding. 262k well ITM at 80 cents which expire this June.

4.55M options, the vast majority ITM but none expiring for 3.5 years or more

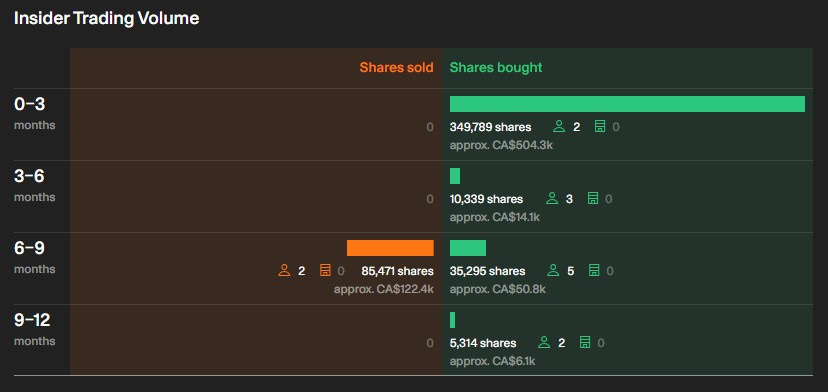

10.5% insider ownership (Per SimplyWallSt) with rather significant open market buying activity of late from insiders

Of the $15M (gross) raised in early December, only $12,484,000 made it’s way into the treasury. A typical 6% in commissions went to the broker along with an equal amount of warrants but somehow $1.26M went to key management for services provided. Ex-fucking-scuseme?

Income Statement:

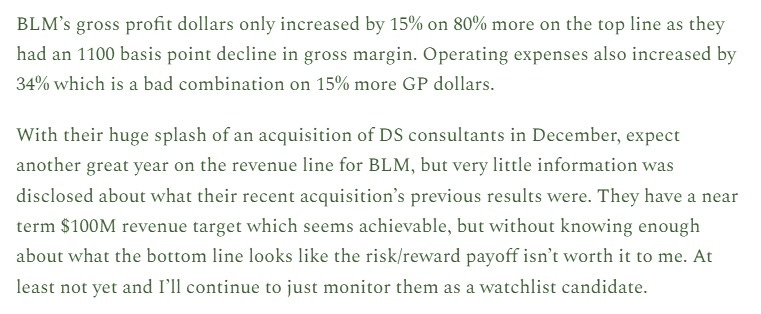

It’s hard to imagine the year starting off stronger on the revenue line with $20.3M representing a 45% increase over the comparable period. Gross margin continues the terrible trend downwards however, losing over 500 basis points at 27.9% comparted to 33% last year. So on 45% top line growth, that margin erosion shrinks that growth to just 22.5% more gross profit dollars.

BLM only has one major operating expense bucket, lumping all of their opex under SG&A expenses. Those costs rose by 56% in Q1, a significantly higher rate than both their revenue and the 22.5% gross profit dollars realized. That doesn’t even include acquisition costs for the DS Consultants purchase, as those $333k costs are shown below the operating income line.

BluMetric realized $700k in income tax recovery in Q1 which limited their net loss to just $67k vs net income of $378k last year. Losses prior to income taxes compared to last year therefore look considerably worse, a $773k loss compared to a $693k profit.

Overall:

The revenue performance is quite commendable, achieving by far a record quarter on the top line. Given that their big new acquisition only accounted for approximately $1.5M of that total, perhaps even more so.

But that is BLM’s only redeeming quality in these and their 2025 financials. After margins depleted by 1100 basis points in in 2025, they dropped by over 500 more to start the year in Q1. To top it off operating costs continue to balloon at a greater rate than dollars delivered to the gross profit line.

After four straight profitable quarters from Q4 of 2023 through Q3 of 2024, the company has posted losses in six of the past seven.

Prior to the DS acquisition, the stock traded at $1.35 and carried a market cap of $50.6M. The stock currently trades at $1.22 (down 10%), but due to the dilutionary measures the market cap has grown by 32% to $66.6M. For that you get a company trading at a 66 EV/EBITDA with negative cash flow and ROIC on a TTM basis.

What I said above confirms my biggest worries I referred to in my earnings preview earlier this month. What I wasn’t counting on was insiders pocketing $1.26M of the $15M raised in their recent financing. If you paid a company 6% commissions or $900k, what justification for services rendered for key management could there be? This was not mentioned in the news release when the financing closed. I did not check the prospectus but I think those participating in the raise would have liked to know that fact.

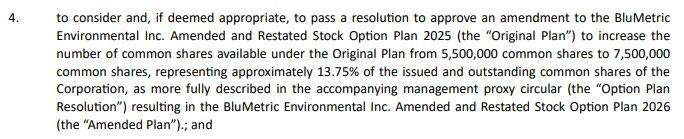

On Friday the company also released their information circular for their upcoming annual shareholder meeting on March 31. Within the items to be voted on is an amendment to their 2026 stock option plan, increasing the amount of options available under the plan.

While I don’t like anything larger than 10% SBC plans, 13.5% is far from the most egregious I’ve seen covering microcaps. But when this is coupled with the $1.26M mentioned earlier, it sends a pretty distinct message to retail shareholders in this writers opinion. Retail does have an advantage of holding over 85% of the shares, but sadly most retail investors in microcaps aren’t smarter than the average zoo chimp, so I fully expect this amendment will pass.

100M in revenue in 2026? Who gives a shit? BLM goes from the watchlist, to the ignore pile. We witnessed what a loss in faith of management in Simply Solventless can do last night. While this may not be in the same category yet, this has too much stank on it.

Downgrade to 2.5 stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Zoo chimps damn.....lol

Thanks for the review wolf, proffesionell as always

Thanks Wold I am impressed with the quality and as important the frequent reviews,, Impressive, Your honest is important and so is your style. Keep it up