We are less than a month from my upgraded Q4 FINS review as the company is already out with their first quarter of 2026.

Back in February, I announced Biorem as my first mid-year pick of 2026 and it was certainly one of my higher conviction plays recently. I identified an important six week window between their Q4 and Q1 releases where their would be an opportunity for some rather significant share price appreciation. With this early FINS release, that window has shrunk to four.

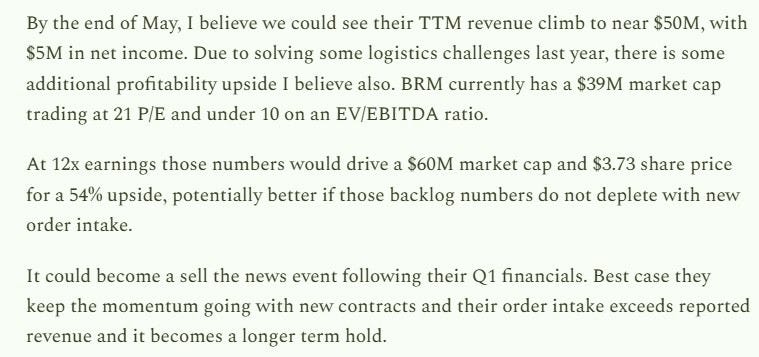

As of this morning, Biorem is up 38% from the February Seal of Approval pick, and just 17 cents shy of the $3.73 price target I set at the time.

What I had wondered back in February is if their Q1 financials would turn into a “sell the news” event. I felt that depended on if they could re-fill that backlog along with the anticipated revenue increases they would have over their first three quarters.

Their earnings headlines do indeed suggest a new record backlog, so does this now turn into a longer term hold? Let’s dive in.

(Free release scheduled for May 21st)

Balance Sheet:

Biorem has improved their current ratio over their last two quarters, now sitting at 3.3 with deferred’s removed. That is made up of $10M in cash, $9.3M of receivables, $2.9M of revenue to be billed, $2.4M worth of inventory and $4.3M in prepaid expenses. All of that overtop of just $8.7M of liability commitments due over the course of the next twelve months. Those commitments are easily covered by their cash balance alone, therefore showing very good liquidity.

BRM has $1.1 M in debt at an attractive 4% interest rate and an unused $3M line of credit.

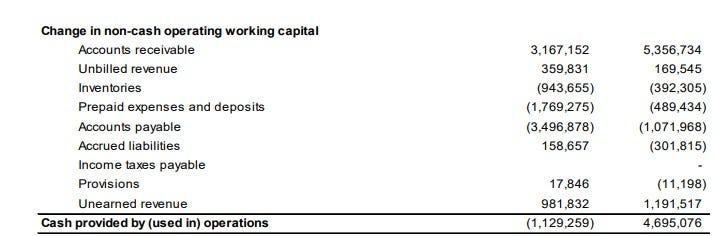

Cash Flow:

A slight hiccup here with $1.13M of operational cash burn during their first quarter, which compares to $4.7M of positive cash flow last year.

Given the large working capital swings I have zero concerns with the burn or variance to last year. They reduced their A/P by 43% in the quarter and had a significant 73% increase in their prepaids during their historical softest revenue quarter. I would anticipate this will reverse next quarter.

They made minor asset investments of $271k and paid down their debt by $147k in the quarter. Overall their cash depleted by 10% in their first three months but I would anticipate a rebound in Q2.

Share Capital:

A very tight float of just 16.1M shares outstanding, with virtually no dilution last year

3.3M options outstanding, all well ITM with 2.3M expiring in early 2027. Only 50k new options were granted in 2025

Announced an NCIB in June. Bought back a limited number of shares over a few week period in September. Not much of a commitment here - more like a game of just the tip to see how it feels.

Limited insider ownership of just 2%. Minor insider buying last May

Income Statement:

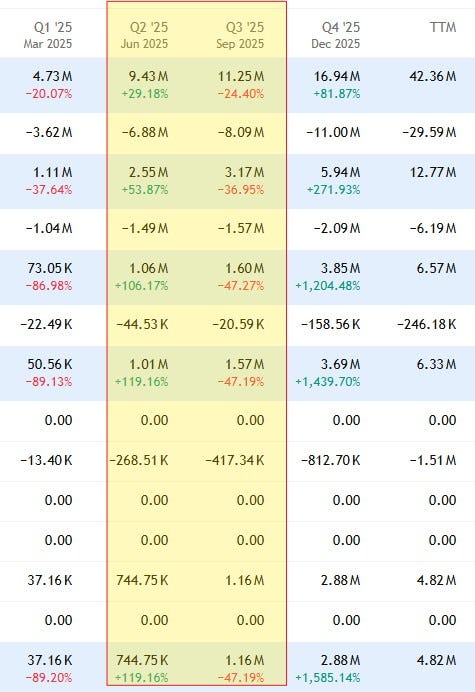

Revenues in Q1 came in at $6.8M, an impressive 44% jump over the same period last year, although well shy of their eye popping record Q4 of just under $17M. Gross margins were 300 basis lower at 20.4% vs 23.4% which generated 26% more gross profit dollars than last year.

Total operating expenses were just 6.7% higher on 44% more revenues, but with 34% more spending on Sales and Marketing. Overall some very good conversion which carries down to the Net Income line which delivered $201k of profitability which is more than 5x than last year.

Summary:

A pretty short review but Biorem has some relatively simple financials and they contain zero red flags or major concerns to highlight.

The biggest question to answer is what’s next and do they have additional upside from the 51% appreciation in share price since their low in mid January. First let’s look back on what I said back in February when I listed a price target of $3.73.

TTM revenue has fallen short of my $50M target, coming in at $44.4M, but the good news is I nailed their net income figure which came in at $4.94M. But given that the company had order intake of $18.7M increasing their backlog to a record $77M offsets that prediction miss from the top line IMO.

When I issued the mid year pick, the company had $71M of backlog which now sits at $77M. At the time, the CEO anticipated that 75% of that number ($53.3M) was expected to be achieved in the next four quarters. At the halfway point of that prediction they achieved $23.8M, leaving $29.5M to potentially be recognized over the next six months. Using the comps above (up against $21.7M in Q2 = Q3), that suggests the potential to beat the next two quarters by 36%.

Biorem has now produced 11 straight quarters of positive net income. That certainly helps to withstand some of the lumpiness of their revenue. When a company can produce profitability whether their revenue is as low as $4.7M, as we saw last year in Q1, or as high as $16.9M as we did in Q4, it really speaks to the operational excellence of the leadership team. My biggest question leading into this quarter was could their sales team refill that backlog. They did that and then some achieving another record of $77M and that is 1.5x of my anticipated Q3 TTM estimate. That supports the additional marketing spend this quarter as well.

For me they answered my biggest questions coming into these numbers. For me, it’s changed from a sell the news event in May to a longer term hold.

I’m also upgrading them for the second consecutive review to 4 stars.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.