I feel like I set this one up on a tee for everyone. Back in February I gave Biorem the Wolf Seal of Approval citing big opportunities for some upward share price moves early in 2026. Many within the Wolf Den discord took note.

Biorem reported their annuals yesterday morning and the market rewarded them with a 16% increase, now giving them a 21% increase from the bottom of my February buy zone.

Let’s dive into the numbers.

Balance Sheet:

With deferred revenue removed, Biorem has a solid 2.6 current ratio consisting of $11.5M in cash, $12M of receivables, $1.4M worth of inventory and $5.7M in other short term assets against just $11.9M in liability commitments over their 2026 fiscal year.

To be polite, Biorem’s aging report is messy. We don’t know their terms, but one would assume their past due receivables to be at least 24%, and have $660k in allowances for doubtful accounts already booked.

Biorem has $1.85M in debt at an attractive 4% interest rate. They also have an unutilized $3M LOC at prime + .75%

Cash Flow:

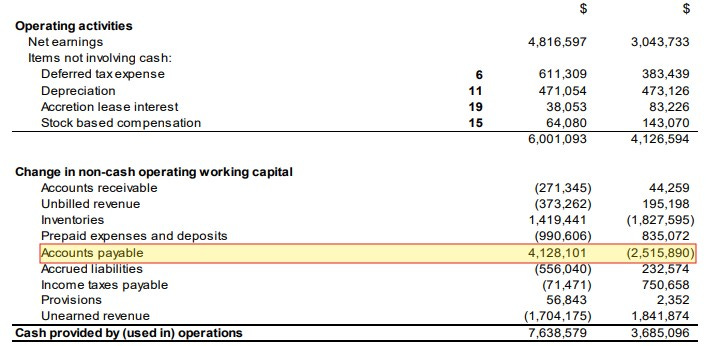

Significant cash flow improvements in 2026 with $7.6M of operational cash flow, more than double (107%) the $3.7M achieved in 2025.

While very impressive it also may be slightly inflated, Payables grew by nearly $4M in Q4 alone and those bills will be coming due. Inventory levels were also significantly depleted in the back half of the year, so re investment there will be expected. Do not be surprised to see a bit of a hiccup in their OCF when the company reports their Q1 in four to five weeks.

The company made minor investments in equipment of $367k during the year, paid down $570k worth of debt and bought back a small amount of stock for $100k.

Overall, their cash position grew by 120% during 2025.

Share Capital:

A very tight float of just 16.1M shares outstanding, with virtually no dilution last year

3.3M options outstanding, all well ITM with 2.3M expiring in early 2027. Only 50k new options were granted in 2025

Announced an NCIB in June. Bought back a limited number of shares over a few week period in September. Not much of a commitment here - more like a game of just the tip to see how it feels.

Limited insider ownership of just 2%. Minor insider buying last May

Income Statement:

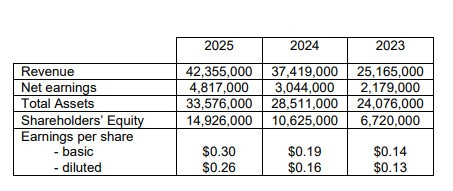

Revenue for the year came in 13% higher at $42.4M vs $37.4M last year. Gross margins were over 300 basis points higher at 30.1% vs 26.9% delivering an impressive 27% more gross profit dollars on 13% more sales.

Total expenses grew by less than 10%, all in G&A expenses showing very good conversion on their revenue and gross margin gains. That all combines for a Wolf Trifecta for their 2025 year.

Earnings from operations were up by 49%, and after a small savings in finance costs and 37% more in income taxes, net income came in at $4.8M, 58% more than the $3M they delivered in 2024.

Much of their 2025 success was delivered in their most recent fourth quarter. At the end of the third quarter, revenue and earnings were down to last year. Q4 revenues were 82% higher for a quarterly record of $16.9M. Gross margin more than doubled from 17.1% to over 35% with gross profit dollars increasing by a factor of 3.7x from $1.6M to $5.9M. At the bottom they delivered a very impressive $2.68M of net income compared to just $200k last year.

They certainly ended 2025 with a bang.

Conclusion:

After a mediocre at best first three quarters of the year, they really saved the year in Q4 with this record quarter on both the top and bottom lines.

If you were paying attention, much of this was telegraphed, hence why I awarded the company my first mid year pick of 2026 back in February. After having three pretty rough quarters of their last four, their order intake and backlog were increasing.

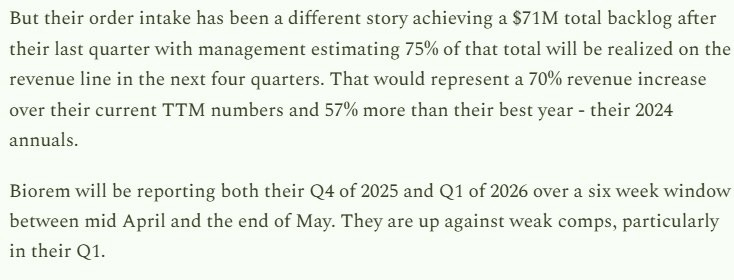

After Q3, the CEO reported $71M of backlog for which they anticipated 75% would be delivered over the next four quarters. That is $53.3M between Q4 of 2025 and Q3 of 2026. After delivering $16.9M in Q4, that leaves $25.4M over the next three quarters. That would represent a 43% revenue increase over the next nine months, while also setting up a very tough comp a year from now.

The downside with Biorem is quarterly results have been lumpier than a bad bowl of oatmeal, but they have delivered a 19% CAGR over their last three years of earnings when you smooth those results out. Their TTM by the end of Q4 looks like it will surpass $50M with improving margins, and they have a proven history of being great operators with excellent float management.

From a valuation perspective, after yesterday’s gains they sit just shy of a 10 P/E, and much more attractive from a cash flow perspective at 6x, and under 6 EV/EBITDA.

Now take into consideration their next three comp quarters starting with a rather dismal $4.7M when the company reports Q1 in four or five weeks. Given what the CEO said at the end of Q3 we should expect a beat over the next three quarters by 43%.

Backlog now sits at $65.3M. After their record Q4 that is down from $71M but 16% higher than they ended 2024 with. As usual the company commentary is cautiously optimistic with caveats on the current geopolitical climate.

Biorem is currently sitting about 50 cents shy of their ATH from last January. Are they a better looking company today than they were then? I would say yes which makes me feel that there is still some room to grow, particularly with these soft upcoming quarters.

If order intake in future quarters continues to be shy of their revenue, that could change resulting in future earnings becoming a sell the news event.

For now, I’m awarding them a half star upgrade to 3.75.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Thanks for the review, Wolf. I pulled out way too soon; didn't expect it to turn around so quickly.