I didn’t have Biorem as a “must” review this week even though I held a position coming into their Q2 earnings which were released on Monday. I had twelve requests in the Wolf Den discord since earnings were announced. The people have therefore spoken and the Wolf always listens to the people (LOL, not really).

Last April, Biorem entered into rare territory achieving a four star Wolf review, and over the next eight months surged by 141% from $1.43 to a high of $3.45. Since then the company has not been able to maintain that momentum, both within their results and correspondingly their share price as well. As you well know, #FinsDontLie.

I’ve been exiting my position over the past little while, which was a painstaking process to say the least due to low liquidity and algo’s undercutting me on the ask. The stock popped as much as 17% on earnings and I used that liquidity opportunity to sell the news to complete my exit.

While I exited, I’m certainly not writing them off forever. I think there may be a day where the stock should be back on my radar. Let’s get into the review and I’ll touch on when exactly that might be.

Paid Subscriber Benefits:

First access to annual picks, upgrades and mid year “Seal of Approval” picks.

Monthly “What’s Wolf Watching” preview of upcoming earnings and potential market moves.

FinsDontLie Scholastic Series - exclusive educational posts

Access to The Wolf Den Discord community (daily insights, charts, chat & Q&A)

Balance Sheet:

One of Biorem’s historical strengths has been their balance sheet and that trend continues here. With unearned revenue removed they have a very impressive current ratio of 4.3 consisting of $7.7M in cash, $9.7M in receivables, $1.8M worth of inventory and $4.5M in other short term assets against only $5.5M in liabilities due over the next year.

Additional disclosures within the notes are on the weak side with no additional details surrounding their A/R (or much else for that matter).

Biorem has $2.15M worth of debt maturing in December of 2028 at an attractive 4%.

Cash Flow:

Operational cash flow is solid with $3.4M generated through the first half of the year, 47% more than the $2.28M generated at this stage last year. This is heavily influenced by working capital adjustments, particularly high A/R collections so while it is good, I wouldn’t expect it to trend as well going forward.

The company partially utilized that inflow by spending $340k on asset purchases and paid down $280k of debt.

Overall they improved their cash position by an impressive 47% from the start of 2025.

Share Capital:

16M shares outstanding in a historically well managed float - 2% dilution over the past year

An unheard of very retail friendly 5% SBC plan\

As of year end 3.3M options were outstanding. They don’t provide an updated table in these financials with their previously mentioned weak disclosures and I’m not interested in going to find it

Not a lot of skin in the game from insiders with under 2% ownership (per YF)

CEO purchased 15k shares during share price lows back in May/early June

Announced an NCIB in June but two months later have yet to buy back any shares

Income Statement:

After a very soft Q1 with only $4.7M in revenue and down 20% on the comparable quarter, BRM rebounded in Q2 with $9.4M in revenue, a 29% increase over Q2 of last year. Gross profit also came in much stronger than last year at 27% which was over a 400 basis point improvement resulting in 54% more GP dollars on 29% more revenue.

Operating expenses rose by a greater rate than their revenue with 31% more in total opex with a concerning 146% more spent in G&A, although this was partially offset by a 29% reduction in marketing spend.

Even while experiencing a 120% increase in additional tax burden (a $146k bogey to last year), they were still able to double their net earnings, $745k vs $340k.

On a YTD basis:

Revenue of $14.2M, up 7%

Gross profit rate of 25.8%, slightly off last year’s 26%

Better YTD conversion with opex only up 4%

Net earnings of $781k, up 15%

Overall:

You may be asking why I have been on the way out of Biorem, particularly when this quarter was much improved from their Q1.

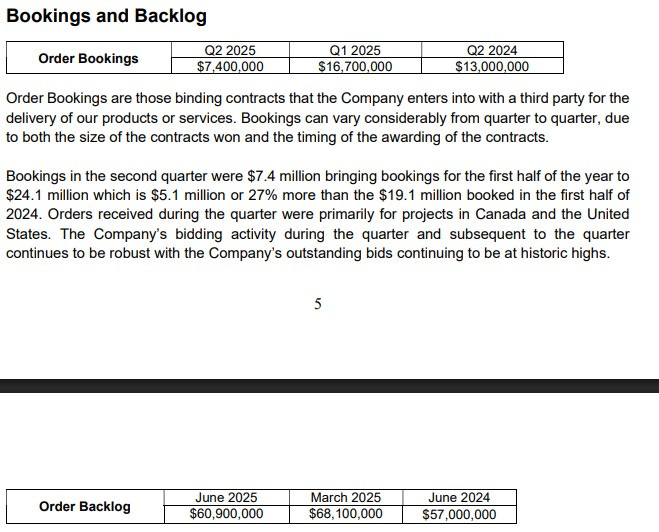

The biggest reason is the quarter they are coming up against when they report again in three months, along with the very overall lumpiness of their top line. They are coming up against their largest ever reported revenue quarter of nearly $15M in total revenue. Through the last six months they have only generated $14.2M so a repeat of last years Q3 looks like a very tough ask.

Their backlog numbers aren’t terrible, above last year but down from last quarter, so matching off their Q3 from last year isn’t an impossible task, it’s just one I’m not willing to continue to risk my investment dollars in.

They trade at seemingly reasonable metrics of 13 P/E, 6 EV/EBITDA and deliver solid ROIC numbers as well. But 70% of their TTM earnings came in Q3 of last year. So I’m going to wait until November to re-evaluate Biorem. If it’s a slight miss with an encouraging future and there is a resulting dip, I will take another hard look.

For now, I’m going to look at more encouraging plays. Maintaining the 3.25 review score.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.