As you might imagine (or not), I receive many requests for reviews and deep dives - so much so that it is virtually impossible to get to them all. I do have a section within the Wolf Den discord that I try to give my two cents for requests that I won’t be able (or don't want) to review.

My initial reaction to this request wasn’t overly energizing or motivating, but when I looked at what they were doing and what the valuation was, I thought it might be worth a look. Investors on the other hand have not felt that way in the past year with the share price losing over 30% in value.

So that’s where we are. I might love it, I might hate it. I really have no idea where this may go, and sometimes these are the most fun.

Balance Sheet:

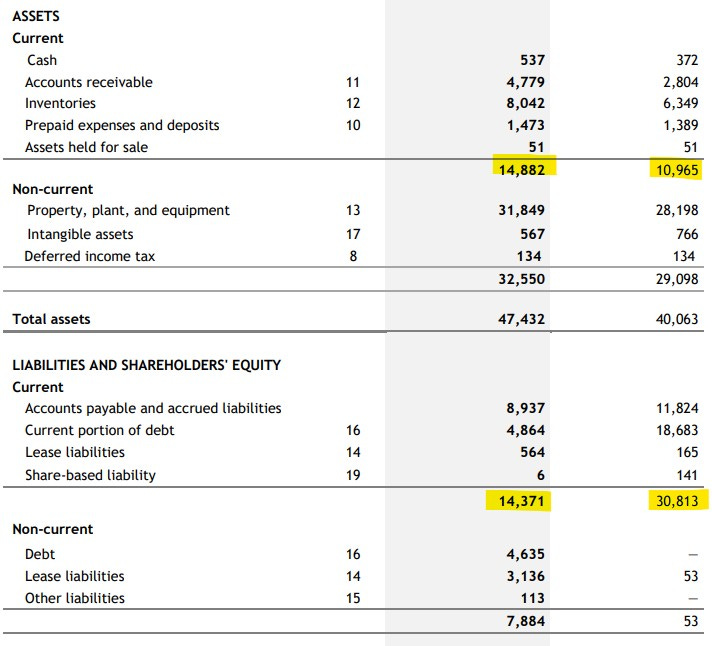

Big Rock doesn’t have a balance sheet that jumps off the page at you but when you look at the terrible shape it was in just a year ago it does give you an indication that they accomplished some things in 2025.

Their current ratio is just above 1 and consists of just $537k in cash, $4.8M in receivables, $8M worth of inventory and $1.5M in other current assets against $14.4M in liabilities due throughout 2026.

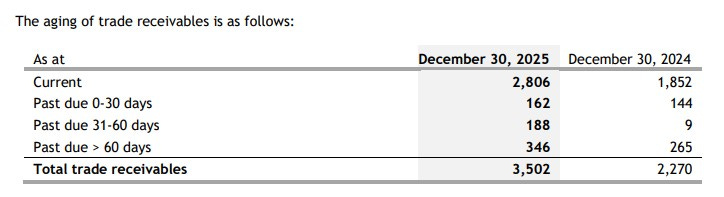

Receivables in terms of aging are ok at best, but not overly concerning.

The company holds $9.5M worth of debt with a little more than half due this year under two separate credit facilities. The majority of the long term debt, nearly $5M isn’t due until 2031.

Post financials the company modified one of their loans including the payment schedule but that announcement was short on details.

Far from a stellar looking balance sheet and not very liquid, but when compared to the .36 current ratio they started 2025 with, it’s certainly much improved which includes reducing their debt by nearly half.

That $9M was not settled via cash flow however. It was settled via a debt for shares transaction, done at $1 share and also with a related entity - VN Capital. Those 9M shares of course now worth 31% less.

Cash Flow:

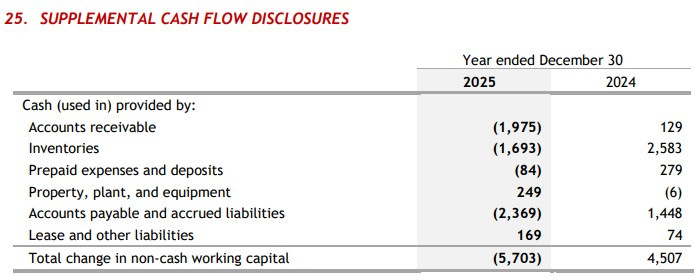

$4.15M of operational cash burn during 2025, and that is 180% worse than the $1.5M they burned in 2024.

This was heavily influenced by working capital changes due to paying down payables, and investments within inventory. It’s also worth noting that the last three quarters have been operationally cash flow positive. I’ll go as far to suggest that their OCF is better than it looks.

During the year they raised $7.4M (net) of capital through a private placement at $1/share and made $2.5M of asset investments.

Overall their cash position improved by 44% during the year, but once again just sits above the half million dollar mark.

Share Capital:

24.5M shares outstanding with extreme 3.5x dilution during 2025 due to the debt settlement and private placement

305k options, all well out of the money at $1.57 but not expiring for over four years

726k RSU’s with nearly 900k granted in 2025. Granting 900k RSU’s when the share count to begin the year was less than 7M appears excessive.

Approx 70% of the float is closely held via insiders or related parties - namely VN Capital Fund

No open market buys, but insiders participated for over $1M in their recent placement (currently down 31%)

Income Statement:

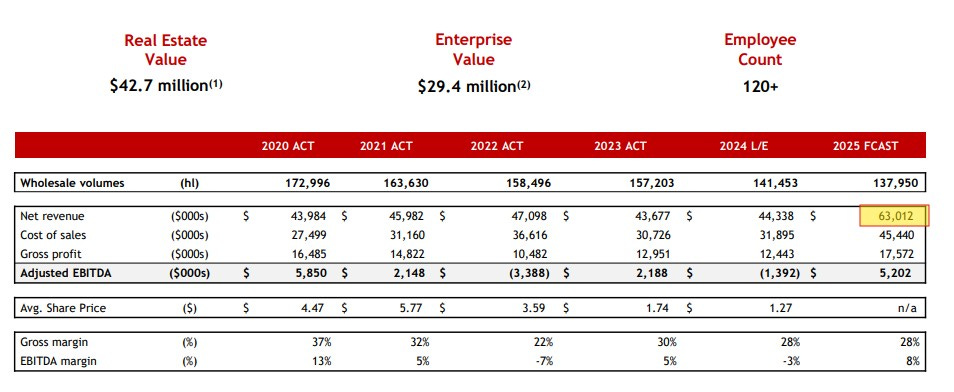

Big Rock achieved $49.1M in revenue during 2025, an impressive 15% improvement YoY. Perhaps more impressively is that they blew gross margins out of the water with a 950 basis point improvement from 25.1% last year to 34.6% this year. That resulted in delivering 59% more dollars to the gross profit line.

Expenses were also controlled very well spending 6% less in G&A costs while selling expenses only rose by 8% which feels like pretty good conversion, particularly when you include the margin impact.

Dare I say it, but those metrics are Wolf Trifecta worthy - Double digit revenues, margin improvement with operational leverage gains.

That just came $179k short of break even at the operating income line, but that compares to an operating loss of $6.1M a year ago.

Below operations, they also saved $1.7M through restructuring their debt so their net loss was reduced by over $12.5M from $13.5M to $939k.

In terms of quarterly revenues, they were $11.1M, up 23% over the prior year with margins of 30.1%, far exceeding the measly 10.5% in the comparable quarter. All of those annual losses however came in Q4, losing $1.06M. Since Q4 is seasonally weaker, revenues were also off to Q3 by 21%.

Overall:

I feel the company did a lot of things right in 2025 and these financials support that, yet the share price decreased by over 30%. They grew revenue by double digits, significantly improved their margins and did all of that at the same time as obtaining some decent operating leverage.

Does any of that make me want to invest in them? Not at all.

After going through the financials, my next step was to visit their investor relations page online. I’ll include their latest investor deck, but I must warn you, it’s from January of 2025 - fifteen months old.

Unfortunately, once you get into the deck, it appears much older as if it was created by someone who used PowerPoint for the very first time, powered by Windows 95.

The one thing that stood out the most was the slide which included their 2025 forecast which was over $63M in revenues. They fell 22% short of that coming in at $49.1M.

My favourite had to be the Key Leadership slide. Is this what they are supposed to look like while wearing beer goggles? Who thought this was a good idea?

Aside from the fact their investor deck gives me zero inspiration, and that it is fifteen months old makes me wonder if they want retail participation in the first place. It is very heavily insider controlled after all. I don’t like when a balance sheet lacks liquidity and the company chooses a significant amount of RSU or DSU share based compensation plan over option based ones.

The stock itself is very illiquid also, going several days without a single trade with their high volume day in the past year being 39,000 shares. I’ve probably never been less attracted to a set of Wolf Trifecta worthy financials. Perhaps the beer goggles aren’t working yet.

I’m giving them 2.5 stars, but note that it would have been 1 star or less had I reviewed their 2024 financials. The goggles just aren’t strong enough to rate them any higher. Pour me another pint.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Thanks for the review, Wolf. Despite the Trifecta, I'm staying away from any booze or cannabis related stocks.

Beer goggles lol....thanks wolf