First look at this $90M market cap that was receiving a lot of chatter around this time last year in microcap circles as they were doing the convention circuit. The company went 9x in the six month stretch of January to June last year, but then lost 48% of their value over the last three months.

ALUULA is a next-generation composite materials company manufacturing the world’s lightest, strongest, and fully recyclable composite fabric, embedded as the premium ingredient inside the world’s leading performance brands.

Their Q1 financials are about a month old now and the share price has stabilized over the past six weeks. Is this a good time to take another look at Aluula or do the financials suggest there is more downside ahead. Let’s find out.

This article will be re-released without a paywall on May 1st.

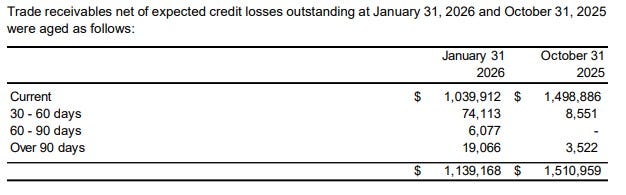

Aluula’s current ratio is (was) decent at 1.70 consisting of $2M in cash, $1.2M in receivables, $2.8M worth of inventory and $370k in other short term assets against $3.8M in liability commitments due over the next twelve months.

I always like to give a positive shoutout when a person is managing their A/R as well as this with 91% of their receivables listed as current.

The company has (had) $1.4M worth of debt, $400k with WD Canada, interest free with payments ending in March 2029, and a $1M related party loan through a numbered company at 12 points. The loan has been amended twice, most recently at the start of the year. Twelve points doesn’t sound like a great deal between friends.

While the current ratio is decent, the quick ratio is (was) a little lacking as their cash + A/R doesn’t (didn’t) offset their one year liability commitments.

Post financials they took advantage of all of that share appreciation and raised a whopping $14.1M through a LIFE offering at $3.30/share with a half warrant exercisable at $4.29 over two years. Those PP investors are currently down 12.1% however.

Aluula plans to utilize about $6.6M of that raised capital on expanding their manufacturing capacity.

That significantly changes the look of their balance sheet and liquidity. They also paid off that related party loan, and considering the twelve points, a wise decision.

Cash Flow:

Aluula burned just shy of $100k through their first quarter of ‘26, but that is a 36% improvement over the comparable quarter. They have not had a positive OCF quarter in their last six. Inventory levels rose by 37% in Q1 and that investment seems to be the biggest culprit contributing to their Q1 burn.

The company utilized $82k in asset purchases and added $164k of debt in the quarter which has now been fully extinguished.

That $2M in cash at the end of the quarter quickly increased to over $14M after commissions on the raise and debt payments.

Given their relatively small burn rate and $8M in additional general working capital available, they seem well positioned moving forward.

Share Capital:

As of Jan 31, 26.3M shares outstanding with 5% dilution in the past year.

Post financials the raise added 4.3M, bringing the total to 30.9M outstanding and dilution rate to 22% over the past five quarters.

Goofy structured warrants. Stated amount of warrants outstanding is 26.25M outstanding which almost made me stop doing the review all together. The actual potential dilution on these should actually be 26.25/20 which is 1.3M. Some of these were exercised post financials

2.5M options, all ITM with the exception of 295k granted in the quarter at $3.30 under the company’s 10% rolling option plan

Insider ownership of approximately 34% per investor deck

Minor slaps on the open market in the past twelve months by insiders

Income Statement:

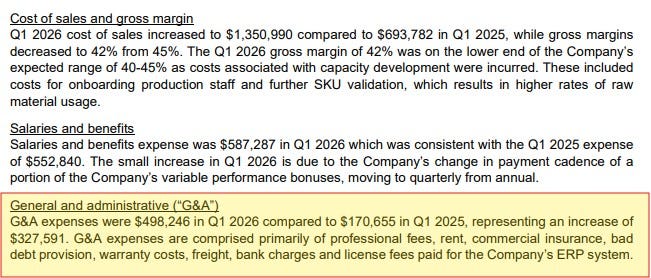

Very strong revenue headlines achieving $2.33M on the top line which is 85% more than they achieved last quarter. Margins did slip by 300 basis points in the quarter to 42%, and as a result delivered 73% more gross profit dollars.

Expenses jumped by 51% mainly via G&A expenses which exploded by 193%. That resulted in a slightly larger operational loss of $260k vs $251k. Not much worth noting below that so their net loss was also slightly up at $384k in the quarter vs $374k.

The margin decline is related to onboarding of staff, and the rationale for their G&A costs (highlighted below) is definitely on the weak side, as there is nothing to assure me that these near tripling of G&A costs are just a one time pain point.

Overall:

On the surface it looks like a disappointment, having 85% more revenue turn into a slightly higher loss at the bottom of the P&L. I certainly would have liked to see a more detailed explanation within the MD&A on where the misses were to be able to forecast their spending moving forward.

On the other hand they went from a pre-revenue company in 2022, achieving $4M in 2023 with a now TTM number approaching $9M. Some growing pains and not all numbers making sense are to be somewhat expected.

They have a long list of partnerships with key brands in the sports and outdoors segment, and I would think this is a company that should be on people’s radar’s, even if you missed out on shares in the 50 cent range one year ago.

There is no better deep dive (very bullish case) than the following piece by Domum Capital. It’s six months old now but I suggest you start here if you are interested in learning more about them.

The biggest question for me is the valuation sitting around $90M. That is about 10x TTM revenues for a non profitable company on the EBITDA or Net Income lines with six straight quarters of operational cash burn and a negative ROIC of -13%.

Their float management history is also questionable. They went from 150M shares in 2022, which ballooned to over 500M shares a little more than a year ago. They did a 1:20 reverse split in February 2025 and have experienced 23% dilution since.

They are definitely going to need to show me a little more to get interested at these levels. Now that their treasury is near full, let’s see how they manage that better looking balance sheet. The fact that their first move post financing closing was to hire an investor relations company makes me wonder.

Three star financials, less a quarter star for the 10x revenue valuation. 2.75 for those who can’t math.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.