AirIQ is one that I’ve wanted to get back to for sometime, as I haven’t published a formal review since November of 2024.

In my initial review earlier that year I awarded the company a handsome 3.75 stars. I tried to establish a position that day and the stock ran too quickly and I was left shareless by days end. Two quarters later I downgraded them to three stars, was thankful for not holding a position and the stock decreased by nearly 30% over the next three months.

That downward trend has reversed since their Q1 back in August of last year, going from $0.31 to $0.56 for an 81% gain and touched as high as 66 cents after these recent financials.

In my February earnings preview article last month, I categorized IQ as a Buy Zone with risk. After initially popping 20% from that article, the stock has retreated back to where it was trading then. My biggest question was whether their Q3 results were already somewhat priced in.

With that, let’s get into their Q3. Small numbers for this solid little $16M market cap so it should be a quickie.

Balance Sheet:

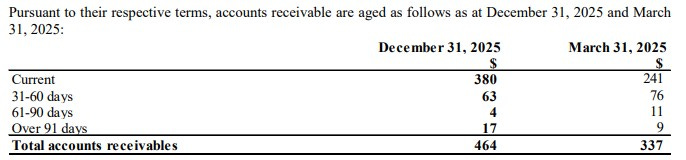

With deferred revenues removed from liabilities, IQ sports a solid current ratio of 3.5 that is made up of $1.4M in cash, $464k in A/R $470k in inventory and $125k in prepaids overtop of just $690k in current liabilities.

Not only do they have zero debt, they have zero long term liabilities outside of $35k in deferred revenue.

Super liquid, and cleaner than a spring breeze.

Cash Flow:

Operational cash flow was flat in the quarter, but is up 41% through three quarters to $929k vs $661k with minor movement within working capital changes.

AirIQ has utilized $2.5M via investments year to date including $850k on an acquisition of an unnamed private IOT company. They have also bought back $203k worth of stock YTD.

As a result of the NCIB, acquisition and investments, their cash position has depleted by 55% since the beginning of the year, but considering the continued health of their balance sheet, it appears these activities were excellent usage of capital.

Share Capital:

29M shares outstanding, approx 450k less than a year ago

2.24 options, all currently ITM. 800k expiring in one year under 19 cents but the rest do not expire for 6.5 years or more

611k shares repurchased under their NCIB this year, over 1.1M over the past two

41% insider ownership per Yahoo Finance

Minor insider buying last August

Income Statement:

Revenue improved in the quarter to $1.7M, a 31% increase over last year. Margins slipped by 110 basis points but still an exceptionally healthy 61.4% and that generated 29% more gross profit dollars.

AirIQ also generated additional operational leverage in the quarter with operating expense growth of only 7% on those additional top line wins.

Even after experiencing a $87k bogey in foreign exchange. I pared to a year ago, they were still able to grow their net income by nearly 4x to $103k.

On a YTD basis.

Top line growth of 10% to $4.66M

A slight uptick in margins by about 25 basis points to 60.7% generating 11% more gross profit

2% increase in operational costs

Total net income of $255k, 55% more than this stage last year

In total, their YTD performance gives them the Wolf Trifecta

Great performance and they have all the hallmarks of a very well run organization. Even more encouraging is their recurring revenue growth was 33% in the quarter and that only includes an estimated $75k from their new acquisition.

That acquisition was completed at the end of October and will add $450k in new recurring annual revenue and it comes with 50% EBITDA suggesting they paid as little as 2.6x EBITDA making it look like an absolute steal.

Since 94% of this quarter is made up of recurring revenue, it makes it that much easier to extrapolate these results. If we did so that would get them in the neighbourhood of $6.8M in revenue with $500k in net income.

So with a current $16M market cap, that doesn’t exactly scream cheap year generating a P/E of 32, but their EV/EBITDA and cash flow multiples in the 10 range do look a little more attractive.

If I’m holding 30-40 cent shares I’m probably grinning widely, but given the lack of liquidity there seems to be some risk taking it on near 60. The stock hasn’t traded over 100k shares in a day since last April, and the bid/ask spread can typically be quite large. Therefore if you’re thinking about buying/adding be careful and keep those things in mind.

The company is going to need their M&A pipeline to kick in I believe to take this to another level.

Even with these great results, they are still very small potatoes. But sexy, crispy ones with a lot of flavour.

Giving them their original 3.75 stars back.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

When i see ‘ trifecta ‘ i am almost immediately inclined to buy 😆