Well it took about three years worth of reviews for someone to finally tell me that I have been using the wrong corporate logo for this 2025 Wolf Pick. Awkward.

Minutes ago ADF Group release their first quarter of 2026, and the highlights look quite impressive.

Four months after my 2025 Wolf Pick came Trump’s “Liberation Day” tariffs sending the stock market reeling and to a much larger extent Canadian companies dealing with aluminum and steel. Due to some excellent managerial decisions a year ago and their deft acquisition of LAR group last September, the company has clawed all the way back and then some with the share price appreciating by over 52% since they released their Q1 a year ago.

A year ago tomorrow I ended a tough review with this.

Guess what, they’re back.

I did not have a chance to review their annuals presented in mid April, my last coming in December after their Q3 which received 3.25 stars. The highlights in the news release suggest upgrade potential. Let’s do the work to find out.

Balance Sheet:

We begin with a solid current ratio of 2.2 that consists of $62.1M in cash, $80.5M in receivables, $18.6M worth of inventory and $81M in other short term assets overtop of $93.2M in liabilities due over the next twelve months. Liquidity is pretty good as well with a quick ratio of 1.5 that includes their cash + A/R against their one year commitments.

I’ve mentioned my disappointment in only disclosing an aging report on an annual basis, but the good news is their A/R is down from the last time we looked at it in December while revenue has increased significantly.

DRX has $37.5M of debt as of these statement, about $1M less than our last review. Post financials the company added $12.5M worth of debt through the Liberal government’s Strategic Response Fund. 50% of which comes in the form of a grant and the other half interest free over eight years beginning in 2029. You don’t turn down this type of opportunity. Free money Homey.

Cash Flow:

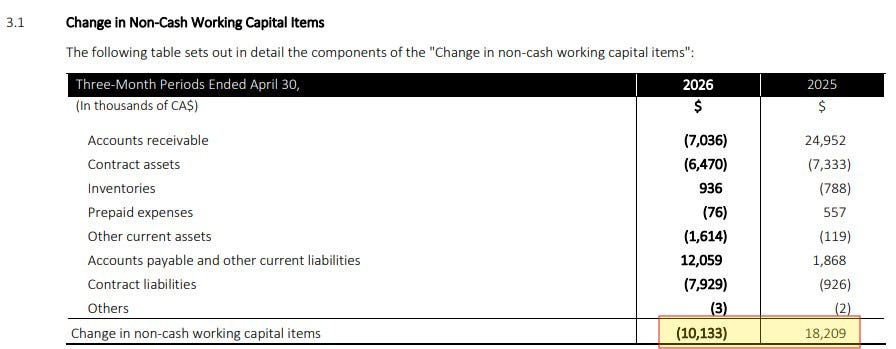

ADF Group had $10.1M of operational cash flow in the quarter, which on the surface may look like a huge miss compared to the $25.3M they generated in the comparable quarter. I’m here to tell you it’s not, as there is a $28M reversal in working capital changes from last year. Prior to working capital adjustments, cash flow from operations totaled $20.2M vs $7.1M.

The company made $8.9M worth of investments in the quarter and paid down nearly $1.8M of debt including interest payments. Overall, they maintained a very similar cash position as they began their fiscal year worth.

Share Capital:

28.6M shares outstanding made up of 16.5M subordinate and 12.1M multiple voting shares

1.05M subordinate shares repurchased last year. NCIB not renewed from December.

450k shares issued in Sept as part of the LAR acquisition

51% ownership between insiders, institutions and private companies

Income Statement:

Revenues exploded out of the gate with $99.3M compared to just $55.5M, an increase of 78%. Not only is that exciting from a YoY perspective, but it is also their best top line performance of the last eight quarters, and at a time when they are facing significant tariff headwinds. Equally impressive was their margin which rose by 220 basis points from 22% to 24.2%, nearly doubling their gross margin dollars which increased by 97%.

They did not however have great conversion within their operational expenses as Selling and Admin expenses rose by 125%, higher than the rate of both their revenue and GP gains. They also came in at 7.7% of revenue vs 6.1%. Acquisition costs related to LAR and SBC costs were the cause. Therefore they miss out on a Wolf Trifecta in Q1.

But even after paying 49% additional income taxes in the quarter, they were still able to deliver $12M of net income, 37% more than a year ago. This was also achieved while experiencing a $2.6M bogey to last year in foreign exchange gains.

Summary:

A pretty fantastic quarter out of the gate, but you have to feel that management sandbagged here as their commentary in April after their somewhat disappointing Q4 didn’t sound this bullish. Post “Liberation Day” the company has become much more conservative on their conference calls, and quite frankly who the hell can blame them. I don’t think Trump knows what he is going to do on a day to day basis, so how can they?

I don’t expect the company’s tone to change much in today’s call so I won’t be waiting for it to complete the review.

What the company did say last time which has changed should be the impact of capex in their fiscal 2027. That is due to the $12.5M in funding from the feds, which essential comes in the form of a half grant, and half interest free loan for which payments will occur in 2029-2037. We are still about one year away from that capex to pay dividends with the completion expected late Q1 of their fiscal 2028 (May/June of 2027).

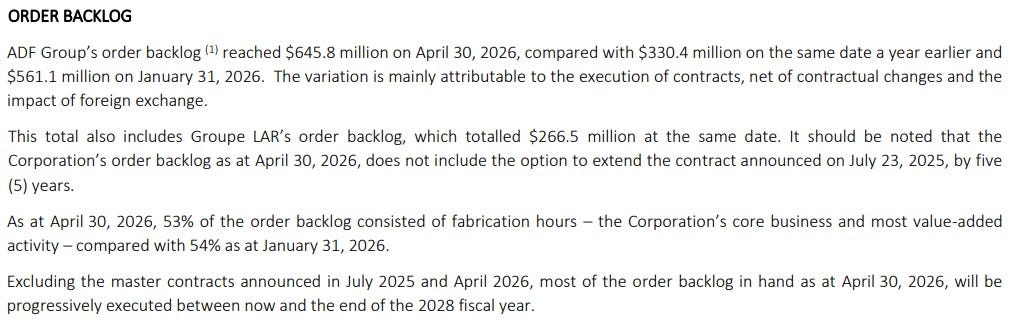

While I expect their quarterly revenue numbers to be lumpy, their short-mid term outlook is very positive as evidenced by their backlog. That number is up by 95% from one year ago and 15% better than announced after their Q4. That does not include a $200M potential extension with their energy sector customer in Quebec. With the government’s aggressive infrastructure plans, the company is also positioned very well to take advantage of those opportunities.

Better yet, that backlog is 74% Canadian. In Q1 of last year, Canadian revenues only amounted to 13% of their business (30% this quarter). This really shows the value of the LAR acquisition and managements ability to diversify and manage the business under very challenging conditions.

With TTM revenue now at $303M and Net Income at $30M, the company now trades at sub 1.0 P/S, a 9.9 P/E and about 5.5 EV/EBITDA ratio. This easily looks to have a 50% upside over the next twelve months.

Upgrade to 3.75 stars and likely poised for another shortly. They are back in a big way.

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from companies I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.